|

|

|

|

|||||

|

|

|

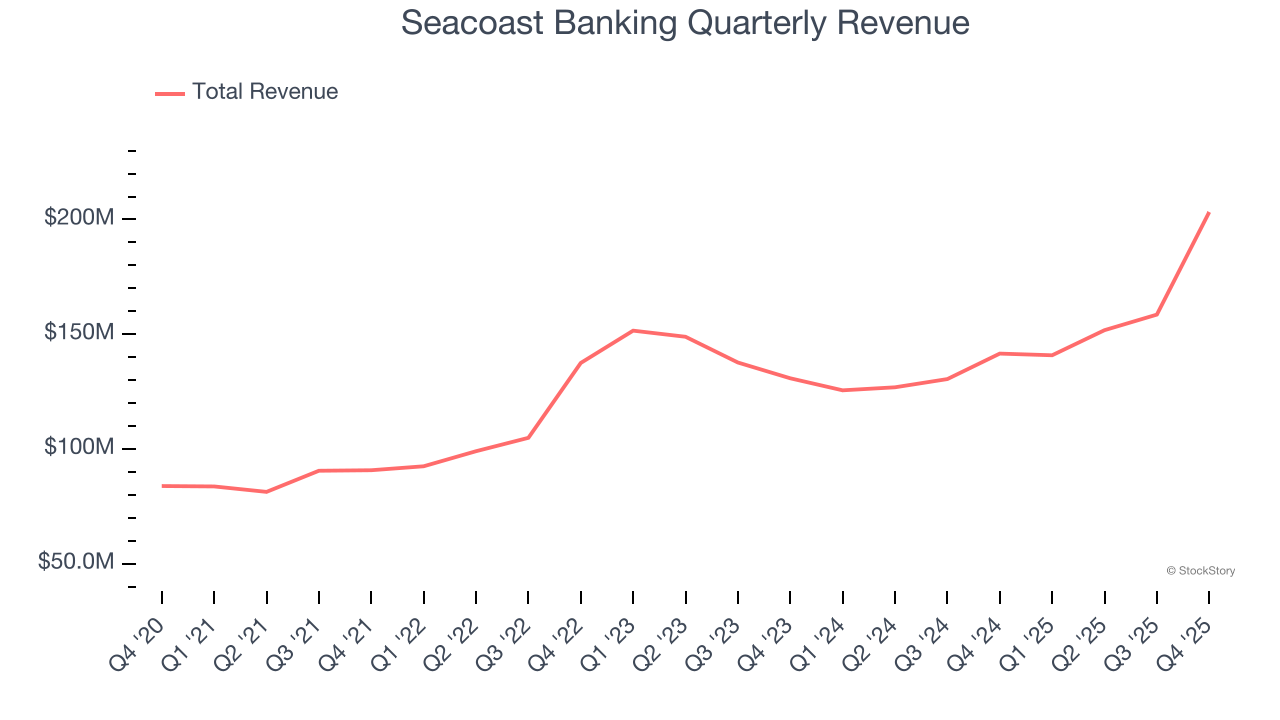

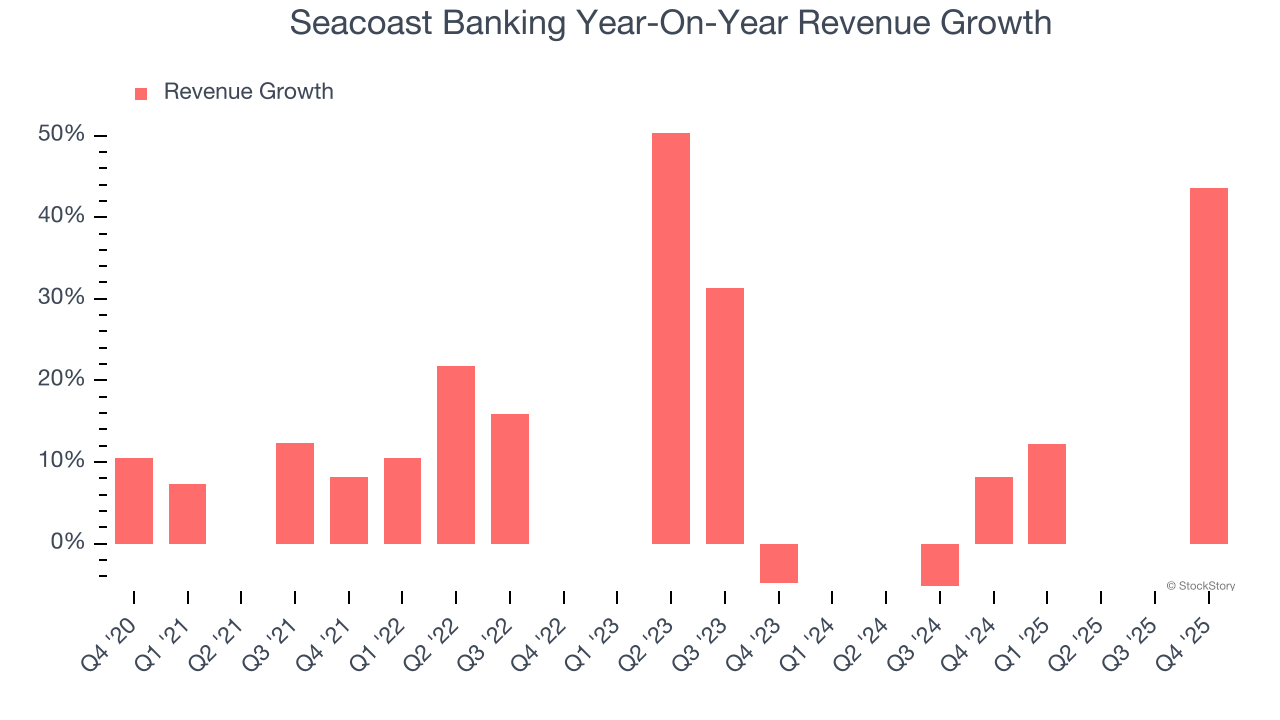

Florida regional bank Seacoast Banking (NASDAQ:SBCF) announced better-than-expected revenue in Q4 CY2025, with sales up 43.6% year on year to $203.3 million. Its non-GAAP profit of $0.44 per share was 11.7% below analysts’ consensus estimates.

Is now the time to buy Seacoast Banking? Find out by accessing our full research report, it’s free.

Charles M. Shaffer, Seacoast's Chairman and CEO, said, “Seacoast delivered another quarter of strong financial performance, highlighted by robust loan growth and continued expansion in pre‑tax pre‑provision earnings. These results underscore the strength, resilience, and momentum of our franchise, which continues to outperform across our markets. We are thrilled to have completed our acquisition of Villages Bancorporation, Inc., a transaction that brings us top‑tier market share and a high‑quality, low‑cost deposit base in the rapidly growing The Villages® community. This acquisition further strengthened our competitive position and enhances our capacity for sustained growth and industry‑leading performance.”

Founded during the Florida land boom of 1926 and surviving the Great Depression, Seacoast Banking Corporation of Florida (NASDAQ:SBCF) is a financial holding company that provides commercial and retail banking, wealth management, and mortgage services throughout Florida.

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Over the last five years, Seacoast Banking grew its revenue at an impressive 15.1% compounded annual growth rate. Its growth beat the average banking company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Seacoast Banking’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 7.2% over the last two years was well below its five-year trend.

This quarter, Seacoast Banking reported magnificent year-on-year revenue growth of 43.6%, and its $203.3 million of revenue beat Wall Street’s estimates by 1%.

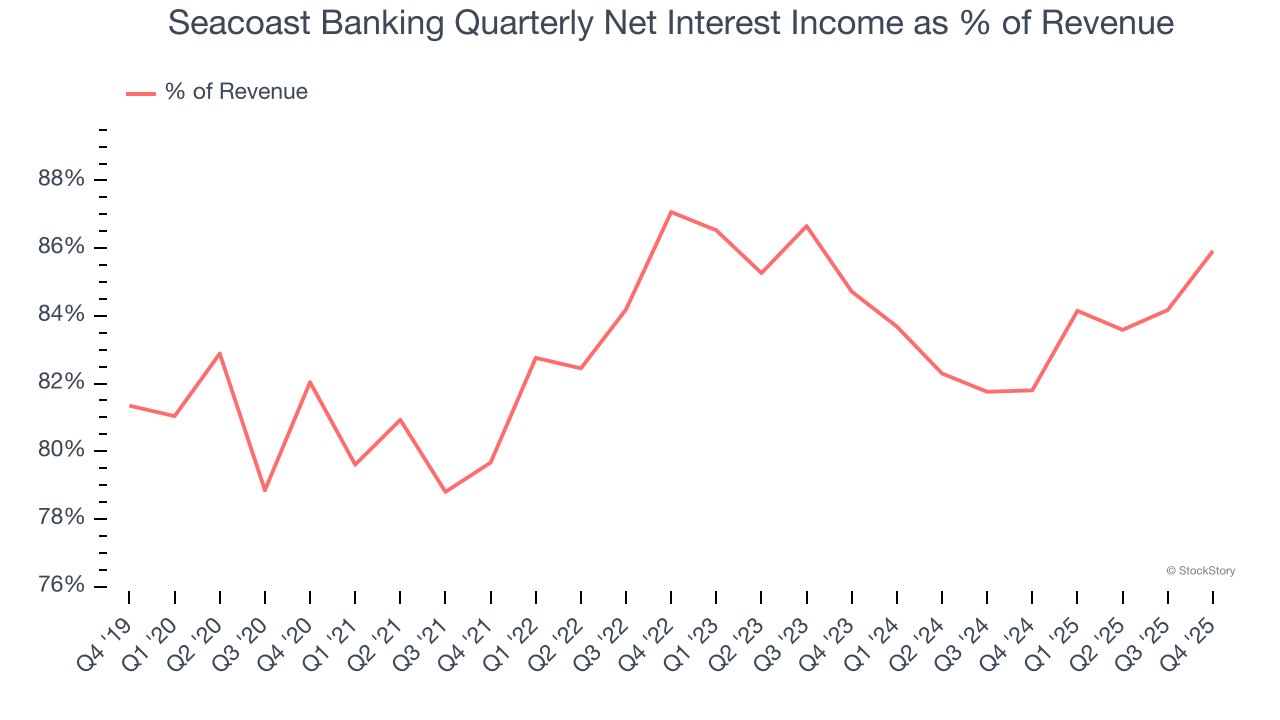

Net interest income made up 83.3% of the company’s total revenue during the last five years, meaning Seacoast Banking barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

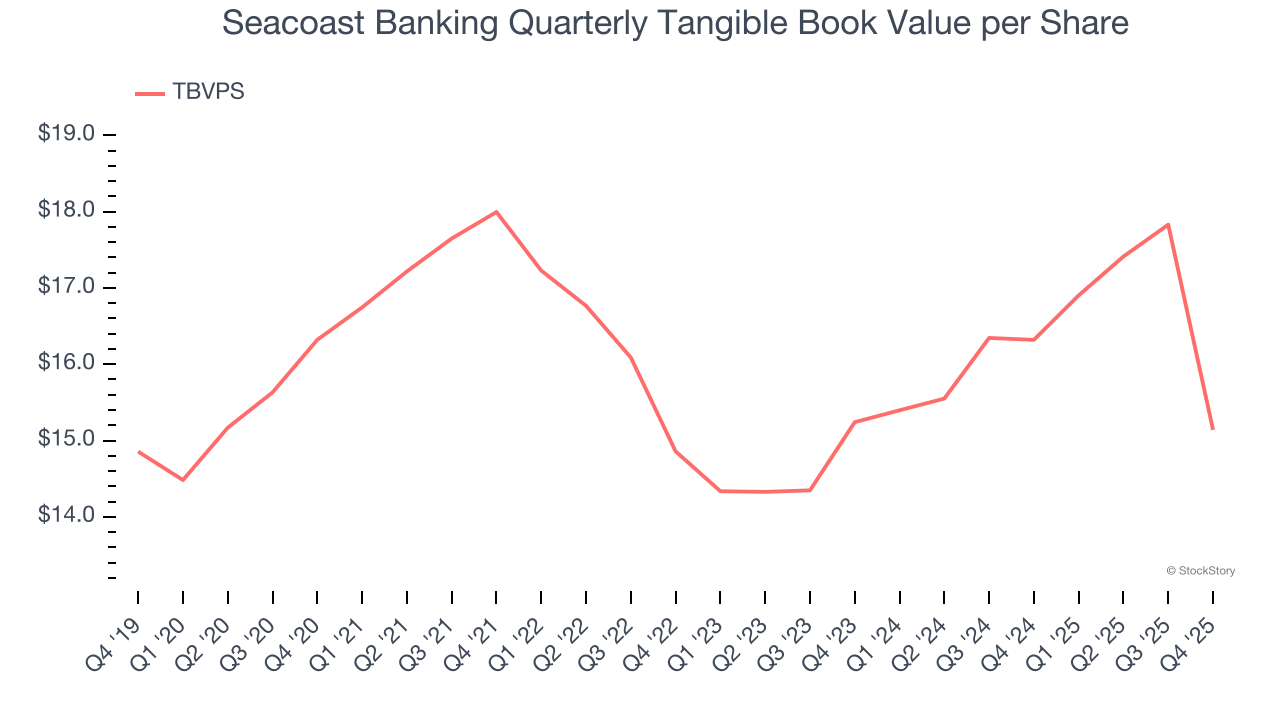

Banks operate as balance sheet businesses, with profits generated through borrowing and lending activities. Valuations reflect this reality, emphasizing balance sheet strength and long-term book value compounding ability.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

Seacoast Banking’s TBVPS declined at a 1.5% annual clip over the last five years. TBVPS has stabilized recently as it was flat over the last two years at about $15.14 per share.

Over the next 12 months, Consensus estimates call for Seacoast Banking’s TBVPS to grow by 19.1% to $18.04, top-notch growth rate.

It was good to see Seacoast Banking narrowly top analysts’ revenue expectations this quarter. On the other hand, its tangible book value per share missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $34.14 immediately following the results.

So should you invest in Seacoast Banking right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 | |

| Jul-06 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-27 | |

| Apr-23 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite