|

|

|

|

|||||

|

|

|

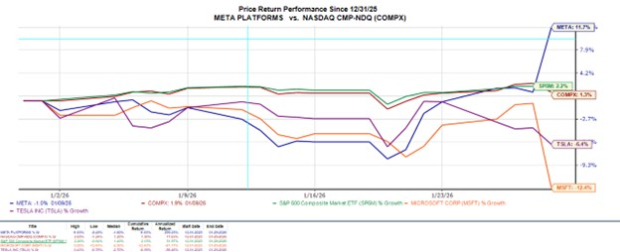

With quarterly results from the Mag 7 starting to roll in after market hours on Wednesday, Meta Platforms META took the spotlight.

Overshadowing reports from Microsoft MSFT and Tesla TSLA, Meta stood out with stronger revenue growth and a bigger earnings beat while offering better-than-expected guidance as well.

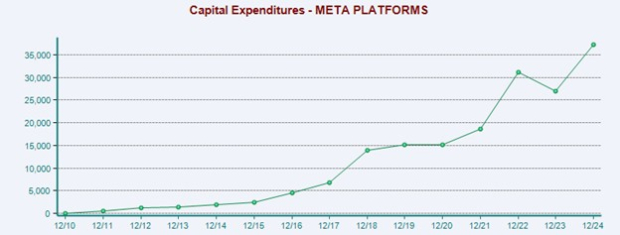

Although the social media leader announced a significant increase in its capital expenditures (CapEx), investors reacted positively as AI boosted Meta’s Q4 performance by improving ad targeting, driving higher engagement, and strengthening advertiser demand.

Robust growth in its family of social media apps (Facebook, Instagram, WhatsApp), higher ad impressions, and improved ad pricing all contributed to a standout quarter with Meta stock spiking as much as +10% in Thursday’s trading session.

Posting Q4 sales of $59.89 billion, Meta’s top line stretched nealry 24% from $48.38 billion in the prior year quarter and impressively topped estimates of $58.59 billion by 2%. On the bottom line, Meta’s Q4 EPS of $8.88 was up 11% from $8.02 per share a year ago and beat expectations of $8.21 by 8%.

With AI being a primary contributor to Meta’s growth, the tech giant plans to boost its CapEx significantly in order to scale its AI infrastructure — including data centers, compute, and its “Meta Superintelligence Labs” — to support next-generation AI models and long-term platform growth.

Meta expects its CapEx to be between $115-$135 billion in 2026, up from the $72.22 billion the company spent last year and a more than 200% increase from $37.26 billion in 2024.

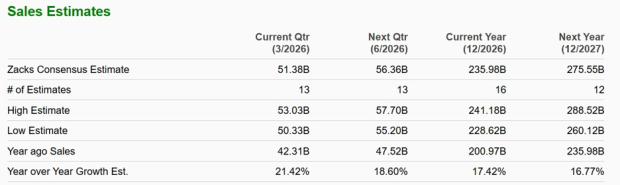

Optimistically, Meta provided positive revenue guidance for Q1 2026, expecting quarterly sales in the range of $53.5-$56.5 billion and nicely above Wall Street’s expectations of $51.38 billion or 21% growth (Current Qtr below).

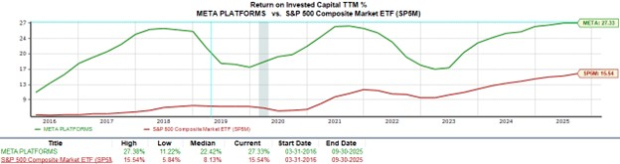

Making Meta’s elevated CapEx less daunting is its intriguing return on invested capital (ROIC) of 27%, showing a keen ability to turn invested capital into profits.

As one of the clearest indicators of long-term shareholder value, the often admirable ROIC percentage is 20% or better, with the benchmark S&P 500’s average currently at 15%.

What may be most intriguing to investors is that Meta is making the argument for being one of the most attractively priced high-growth tech stocks when considering P/E valuation.

Although Meta's stock has a lofty price tag of over $700, its 22X forward earnings multiple offers a discount to the benchmark and is the cheapest P/E valuation among the Mag 7, with the rest of these big tech peers at 30X or more, and Tesla having the high of 196X.

Following a strong Q4 report, Meta stock currently lands a Zacks Rank #3 (Hold). However, a buy rating could be on the way considering that the tech giant’s favorable guidance, valuation, and ROIC could offset any CapEx concerns.

Keeping this in mind, EPS revisions for FY26 and FY27 could begin to rise in the coming weeks. This would certainly serve as a further catalyst for more upside in Meta stock, especially with double-digit top and bottom line growth already being anticipated for the foreseeable future.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 34 min | |

| 6 hours | |

| 10 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 13 hours | |

| 19 hours | |

| 20 hours | |

| Jul-18 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite