|

|

|

|

|||||

|

|

|

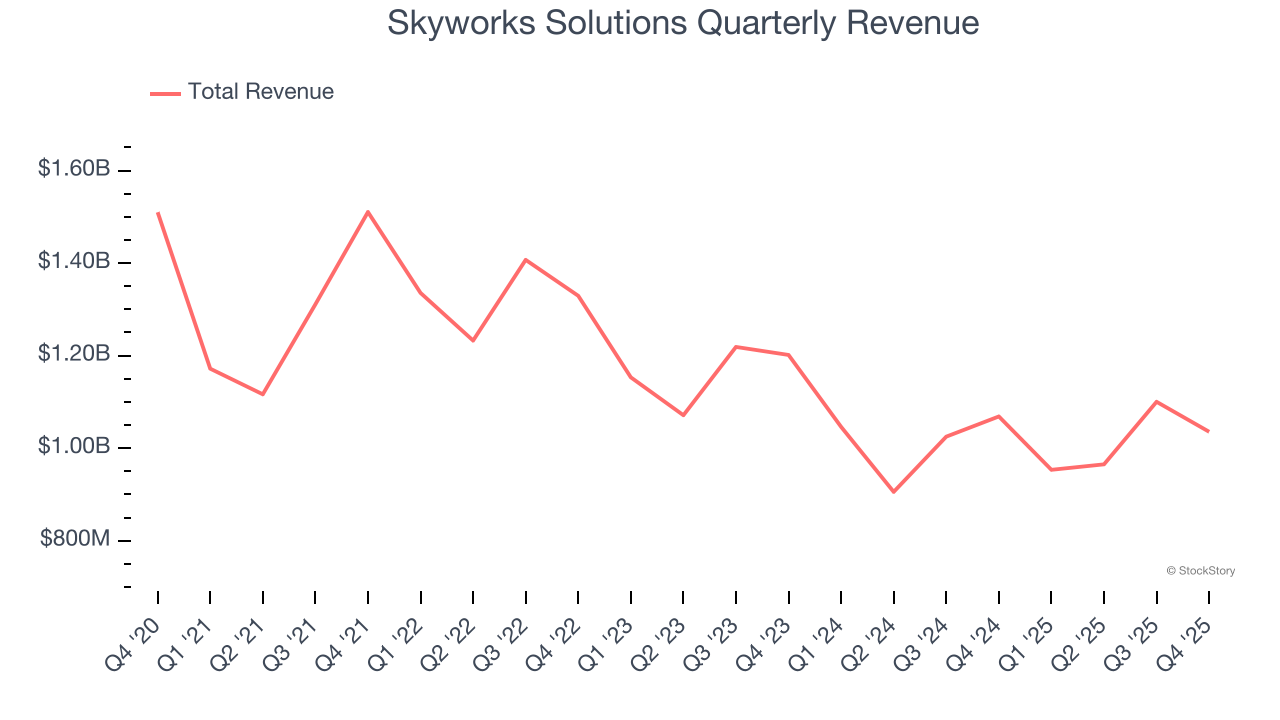

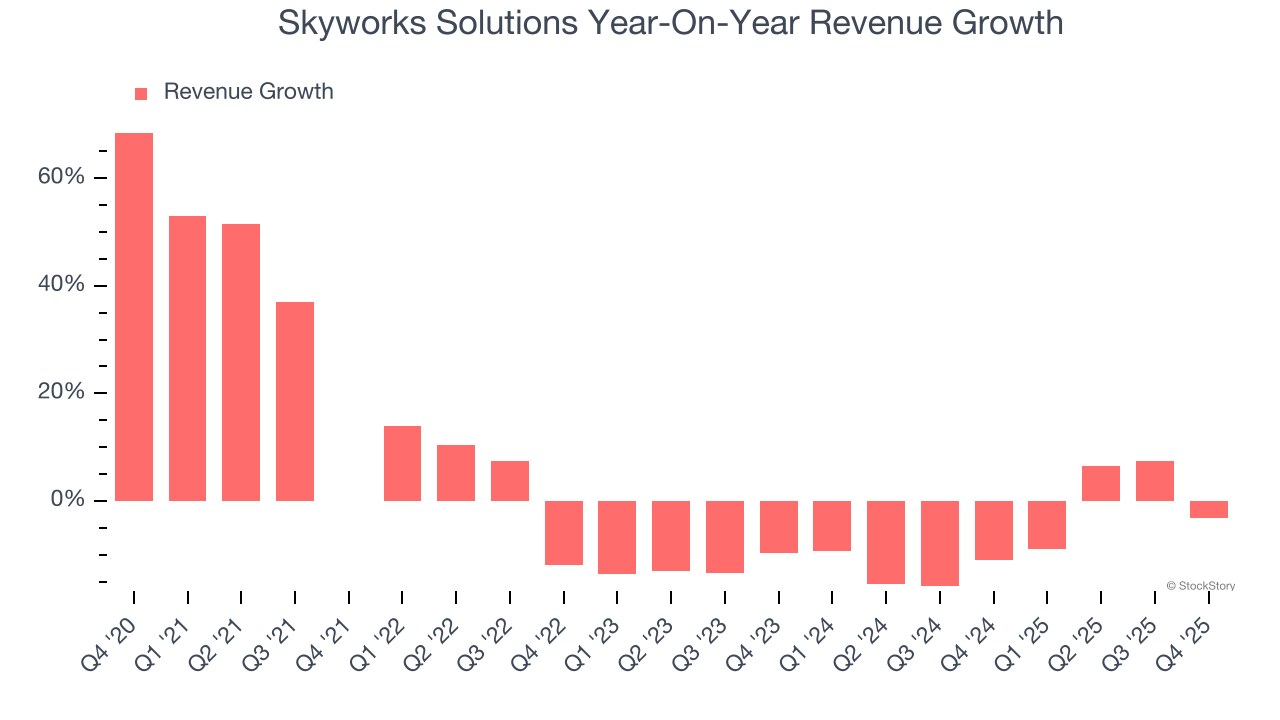

Wireless chips maker Skyworks Solutions (NASDAQ: SWKS) announced better-than-expected revenue in Q4 CY2025, but sales fell by 3.1% year on year to $1.04 billion. On top of that, next quarter’s revenue guidance ($900 billion at the midpoint) was surprisingly good and 103,166% above what analysts were expecting. Its non-GAAP profit of $1.54 per share was 10.1% above analysts’ consensus estimates.

Is now the time to buy Skyworks Solutions? Find out by accessing our full research report, it’s free.

“We delivered results above our expectations for the fourth consecutive quarter, with outperformance across revenue, gross margin, and non-GAAP earnings,” said Phil Brace, chief executive officer and president of Skyworks.

Result of a merger of Alpha Industries and the wireless communications division of Conexant, Skyworks Solutions (NASDAQ: SWKS) is a designer and manufacturer of chips used in smartphones, autos, and industrial applications to amplify, filter, and process wireless signals.

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Skyworks Solutions struggled to consistently increase demand as its $4.05 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a low quality business. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Skyworks Solutions’s recent performance shows its demand remained suppressed as its revenue has declined by 6.6% annually over the last two years.

This quarter, Skyworks Solutions’s revenue fell by 3.1% year on year to $1.04 billion but beat Wall Street’s estimates by 3.4%. Company management is currently guiding for a 94,319% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 10.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

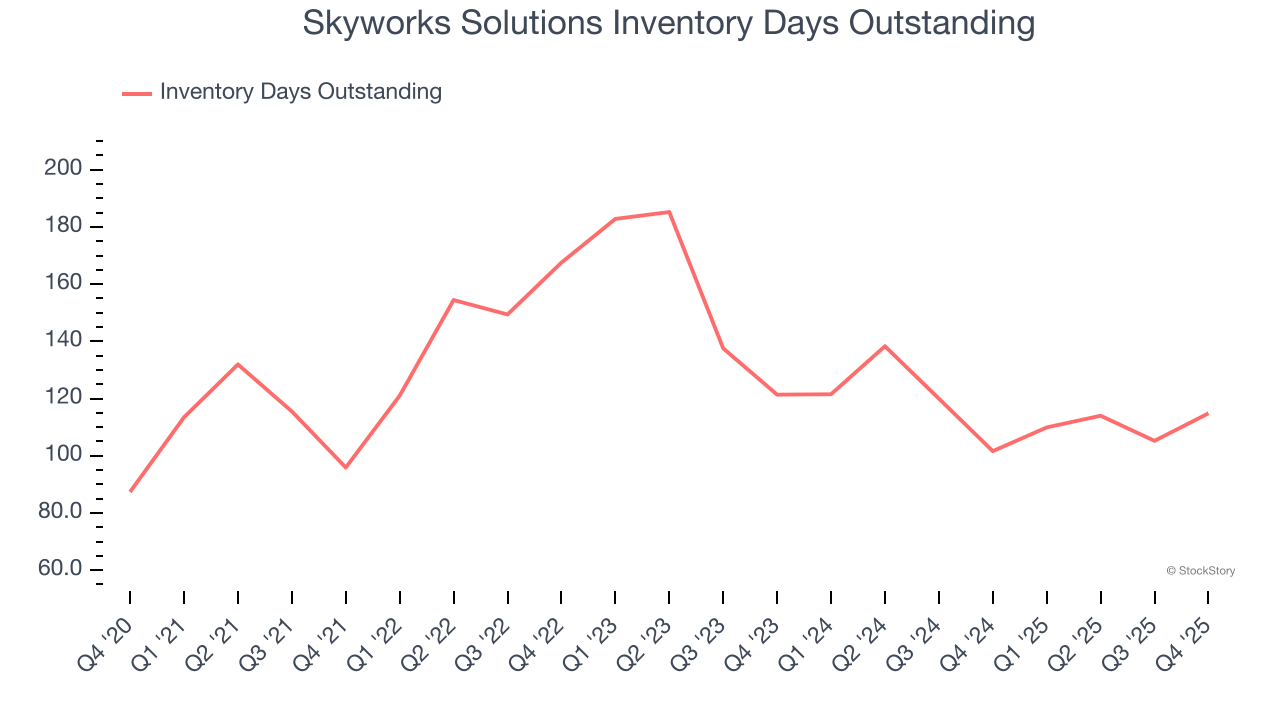

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Skyworks Solutions’s DIO came in at 115, which is 15 days below its five-year average. These numbers show that despite the recent increase, there’s no indication of an excessive inventory buildup.

It was good to see Skyworks Solutions beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its inventory levels materially increased. Zooming out, we think this quarter featured some important positives. The stock traded up 1.8% to $57.04 immediately following the results.

Skyworks Solutions had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-04 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-15 | |

| Jul-14 | |

| Jun-29 | |

| Jun-16 | |

| Jun-11 | |

| Jun-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite