|

|

|

|

|||||

|

|

|

Norwegian Cruise Line trades for much lower revenue and forward earnings multiples than its peers.

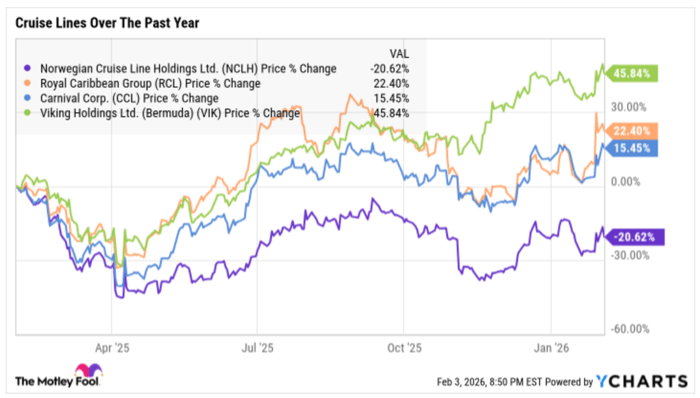

It has declined over the past year, a sharp contrast to the double-digit gains by Carnival, Royal Caribbean, and Viking.

It will have a lot to prove when it offers up its fourth-quarter results in a few weeks.

They say you get what you pay for, and that's pretty apparent when it comes to cruise line stocks. Stack up Norwegian Cruise Line (NYSE: NCLH) against larger rivals Royal Caribbean (NYSE: RCL) and Carnival (NYSE: CCL) -- and even river cruise leader Viking Holdings (NYSE: VIK) for good measure -- and one of them stands out for its low relative valuation.

Pick a metric, any metric. Norwegian is, in theory, the cheapest. But that doesn't make it the best stock. You could have said that a year ago, too. How did that work out?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

NCL also stands out from the pack for some distinctively bad reasons. The one head-shaking reason I want to start with is a chart. NCL isn't just lagging its peers' share performance over the past year. It's the only cruise line stock trading lower during that time.

Sliding more than 20% as the three other cruise line stocks have posted double-digit percentage gains isn't a good look. It's proof that a rising tide doesn't lift all ships.

NCL is textbook cheap. Let's start with forward earnings. This is the P/E ratio for all four stocks based on what analysts believe each company will earn in fiscal 2026. If this was a limbo contest, NCL would win.

Image source: Getty Images.

Head over to the other end of the income statement. NCL also stands out for its lowest trailing revenue multiple relative to its market cap. Let's go over the revenue multiples of all four companies.

Market cap divided by revenue for each stock:

If you're a value investor, it's understandable if you'd want to put NCL under the microscope. A stock in a growing industry with a forward P/E in the single digits is going to turn heads. Don't let that get you dizzy.

Some of the most frustrating stocks are the ones that seem too cheap to be true. On the surface, NCL appears to be a value trap. It trades at multiples well below its peers. I haven't delved into it yet, but NCL is also at the back of the pack when it comes to margins. After all, when it trades at half the forward earnings multiple of Royal Caribbean but less than a quarter of its revenue, it's clearly lacking the ability of its closest competitor to convert more of its sales to the bottom line.

Where does NCL stand out? Viking is growing a lot faster than the other three stocks, justifying its market premium. Carnival and Royal Caribbean pay dividends, wooing income investors. But if it just comes down to the lowest valuation metrics, that's more of a surrender than a victory lap. White flags can also be red flags.

The rub is that I'm not prepared to give up on NCL's chances to run with its more successful -- and, over the past few years, more lucrative -- seafaring competitors. The buoyant industry dynamics should eventually lift even the weakest ship.

Viking has the opportunity to follow in the footsteps of Carnival and Royal Caribbean this earnings season. Those companies offered up fourth-quarter revenue growth that more than doubled their year-over-year performance in the third quarter, three months earlier. NCL is in a similar situation. After NCL posted 5% top-line growth in the seasonally potent third quarter, Wall Street pros are targeting an 11% increase for the fourth quarter, which it will announce later this month.

Can NCL prove itself worthy? Can a strong report lead to sustainable upticks? Can the industry laggard turn around like its peers, transforming headwinds into tailwinds? The market is waiting for NCL to stop acting so cheap. If that happens, you won't mind paying up for something good.

Before you buy stock in Norwegian Cruise Line, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Norwegian Cruise Line wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $431,111!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,105,521!*

Now, it’s worth noting Stock Advisor’s total average return is 906% — a market-crushing outperformance compared to 195% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 4, 2026.

Rick Munarriz has positions in Royal Caribbean Cruises and Viking. The Motley Fool recommends Carnival Corp. and Viking. The Motley Fool has a disclosure policy.

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite