|

|

|

|

|||||

|

|

|

The Kraft Heinz Company KHC posted fourth-quarter 2025 results, with the top line missing the Zacks Consensus Estimate but the bottom line exceeding the same. However, both metrics declined year over year.

The company has greater-than-expected potential to modernize its brands and address operational challenges, many of which are within its control. To sharpen its focus on performance improvement, the company has paused the separation initiative and shifted resources toward executing its core strategy. Kraft Heinz is also launching a $600 million investment across marketing, sales, R&D, product improvement, and selective pricing, supported by a strong balance sheet and robust free cash flow, which management believes will accelerate the company’s recovery and growth trajectory.

Kraft Heinz posted adjusted earnings of 67 cents per share, beating the Zacks Consensus Estimate of 61 cents. Quarterly earnings fell 20.2% year over year, mainly due to lower adjusted operating income, elevated taxes on adjusted earnings, and increased interest expense, partially offset by favorable changes in other income/expense and a lower share count.

Kraft Heinz Company price-consensus-eps-surprise-chart | Kraft Heinz Company Quote

The company generated net sales of $6,354 million, down 3.4% year over year. The metric missed the Zacks Consensus Estimate of $6,418 million. Net sales included a favorable foreign currency impact of 0.8 percentage points. Organic net sales decreased 4.2% compared with the prior year period. Our model expected a 4.1% dip in organic sales.

Pricing contributed a positive 0.5 percentage point impact, driven by increases in the International Developed Markets and Emerging Markets segments, while pricing in North America remained flat. Favorable pricing primarily reflected actions taken in select categories to offset higher input costs.

Volume/mix declined by 4.7 percentage points year over year, with decreases across all segments. The unfavorable volume/mix was mainly due to declines in coffee, cold cuts, Indonesia, bacon and Ore-Ida.

The adjusted gross profit of $2,101 million decreased from the $2,262 million reported in the year-ago quarter. The adjusted gross margin contracted 130 bps to 33.1%. We had expected an adjusted gross margin decline of 50 bps to 33.9%.

Adjusted operating income declined 15.9% to $1,164 million, primarily due to inflation in commodities and manufacturing exceeding productivity gains, while higher marketing spend and lower volumes further weighed on margins. These factors more than offset the benefits of pricing actions.

North America: Net sales of $4,700 million declined 5.4% year over year. Organic sales fell 5.4%. We expected a 6% decline in segment organic sales. During the quarter, pricing remained flat and the volume/mix fell 5.4 percentage points.

International Developed Markets: Net sales of $930 million were up 1.8% year over year. Organic sales declined 2.4%, with pricing up 1.8 percentage points and volume/mix dipping 4.2 percentage points. We expected a 0.7% decline in segment organic sales.

Emerging Markets: Net sales of $724 million were up 4.3% year over year. Organic sales grew 2.2%. We expected 5% growth in segment organic sales. Pricing up 2.4 percentage points, but volume/mix down 0.2 percentage points.

Kraft Heinz ended the quarter with cash and cash equivalents of $2,615 million, long-term debt of $19,311 million and total shareholders’ equity (excluding noncontrolling interest) of $41,664 million. Net cash provided by operating activities was $4,462 million for the year ended Dec. 27, 2025, and free cash flow was $3,661 million.

In fiscal 2025, the company returned significant capital to shareholders, paying $1.9 billion in cash dividends and repurchasing $436 million of common stock. Approximately $400 million of these repurchases were executed under the company’s publicly announced share repurchase program. As of Dec. 27, 2025, the company had approximately $1.5 billion remaining under its authorized share repurchase program.

For fiscal 2026, Kraft Heinz expects organic net sales to decline 1.5% to 3.5% year over year, reflecting an estimated 100 bps impact from incremental SNAP-related headwinds.

Constant currency adjusted operating income is projected to decline 14% to 18%. Adjusted gross profit margin is expected to decrease 25-75 bps versus the prior year.

The company anticipates adjusted EPS to be between $1.98 and $2.10.

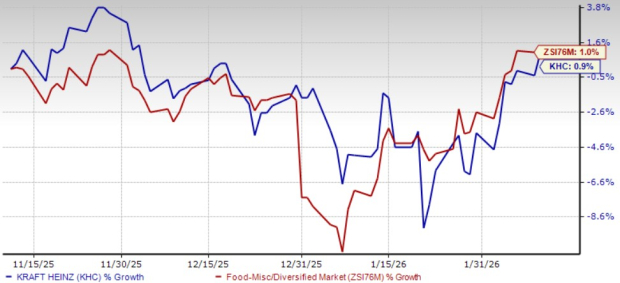

Shares of this Zacks Rank #4 (Sell) company have gained 0.9% in the past three months compared with the industry’s growth of 1%.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It holds a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Hershey’s current financial-year sales and earnings indicates growth of 4.4% and 21.2%, respectively, from the prior-year reported levels. HSY delivered a trailing four-quarter earnings surprise of 17.2%, on average.

The Simply Good Foods Company SMPL, a consumer-packaged food and beverage company, engages in the development, marketing, and sale of snacks and meal replacements, and other products in North America and internationally. It carries a Zacks Rank #1 at present. SMPL delivered a trailing four-quarter earnings surprise of 5.5%, on average.

The Zacks Consensus Estimate for Simply Good Foods’ current fiscal-year earnings implies growth of 1.6%, from the year-ago figures.

Monster Beverage Corporation MNST is a marketer and distributor of energy drinks and alternative beverages. It currently carries a Zacks Rank #2 (Buy). MNST delivered a trailing four-quarter earnings surprise of 5.5%, on average.

The Zacks Consensus Estimate for Monster Beverage’s current financial-year sales and earnings indicates growth of 9.5% and 22.8%, respectively, from the prior-year reported levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 10 hours | |

| 10 hours | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Kraft Heinz Strikes Deal With Disney to Supply Resorts and Tap Characters

KHC

The Wall Street Journal

|

| Jul-21 | |

| Jul-20 |

Monster Stock Creates Add-On Entry After Powerful Earnings-Fueled Breakout

MNST

Investor's Business Daily

|

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite