|

|

|

|

|||||

|

|

|

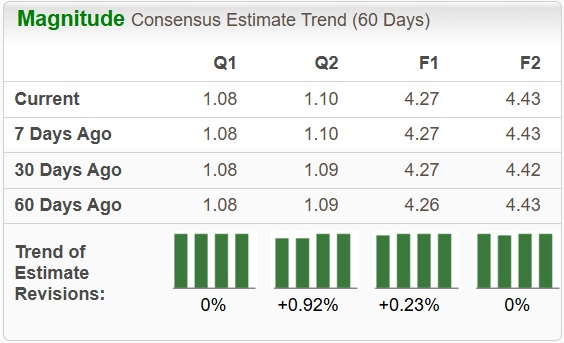

Realty Income Corporation O, a leader in the net lease sector, is slated to release fourth-quarter 2025 results on Feb. 24, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s adjusted funds from operations (AFFO) and revenues is pegged at $1.08 per share and $1.46 billion, respectively.

While the Zacks Consensus Estimate for fourth-quarter 2025 AFFO per share has remained unrevised at $1.08 over the past two months, it suggests 2.86% growth year over year. The Zacks Consensus Estimate for quarterly revenues implies a notable year-over-year increase of 9.08%.

For the current year, the Zacks Consensus Estimate for Realty Income’s revenues is pegged at $5.72 billion, implying a rise of 8.54% year over year. The consensus mark for 2025 AFFO per share stands at $4.27, calling for an expansion of around 1.91% on a year-over-year basis.

Estimate Revision

Over the trailing four quarters, the company’s AFFO per share surpassed the Zacks Consensus Estimate on one occasion, met in another and missed in the other two periods. This is depicted in the graph below:

Realty Income Corporation price-eps-surprise | Realty Income Corporation Quote

Our proven model predicts a surprise in terms of AFFO per share for Realty Income this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an AFFO beat, which is the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Realty Income currently carries a Zacks Rank of 3 and has an Earnings ESP of +0.99%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Investors heading into fourth-quarter results from Realty Income are likely focused on one question: Can the company keep delivering steady growth while scaling new capital partnerships? The net-lease REIT has spent much of 2025 positioning itself for larger and more diversified deal flow. The fourth quarter is expected to indicate whether that strategy has translated into earnings momentum and continued balance sheet strength.

Through the first nine months of 2025, Realty Income generated AFFO of $3.19 per share. Management raised full-year AFFO guidance to $4.25-$4.27 per share, implying roughly $1.06-$1.08 in the fourth quarter. The company expected more than $6 billion in full-year investments. Same-store rental revenue growth was 1.3% through September, while portfolio occupancy remained strong at 98.7%.

In the fourth quarter, Realty Income is likely to have witnessed stable operational performance, driven by its well-diversified, high-quality property portfolio. A large share of its rental revenues comes from tenants with a non-discretionary, low price point and service-oriented focus, supporting steady cash flow. Its disciplined acquisition strategy and emphasis on high-performing assets are likely to have underpinned portfolio strength and operational consistency during the period.

Its sustained occupancy, reflecting prudent underwriting and resilient tenant demand, is likely to have supported earnings stability. Focus on defensive sectors and proactive asset management is believed to have enhanced portfolio durability.

The company has completed billions in property investments in recent years, and fourth-quarter results are likely to reflect incremental income from those transactions. During the fourth quarter, the company announced a $800 million preferred equity commitment tied to CityCenter real estate, broadening its opportunity set beyond traditional retail net leases and reflecting strong institutional relationships. This deal expands Realty Income’s presence in high-quality mixed-use real estate and introduces a structured investment with attractive yield characteristics.

On the balance sheet front, the company is likely to have maintained a strong financial footing, backed by investment-grade credit ratings of A3 from Moody’s and A- from S&P. Its capital structure is expected to have remained sound, with manageable leverage, a well-laddered debt maturity profile and ample liquidity, all of which are likely to have enhanced flexibility to fund growth and manage refinancing risk.

The consensus mark for rental revenues (excluding reimbursable) is pegged at $1.30 billion, in line with the prior quarter and up from $1.20 billion in the year-ago quarter.

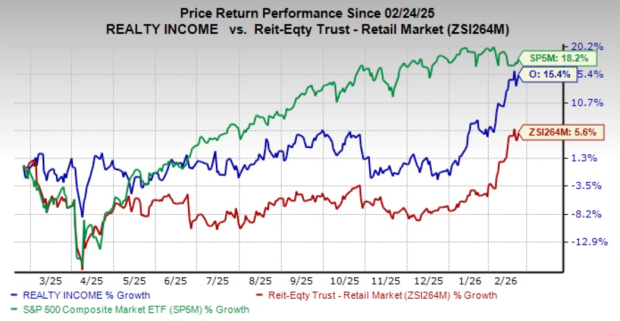

Shares of Realty Income have rallied 15.4% in the past year, closing at $66.14 yesterday on the NYSE. The Zacks REIT and Equity Trust - Retail industry has declined 5.6%, while the S&P 500 composite has increased 18.2% over the same time frame.

One Year Price Performance

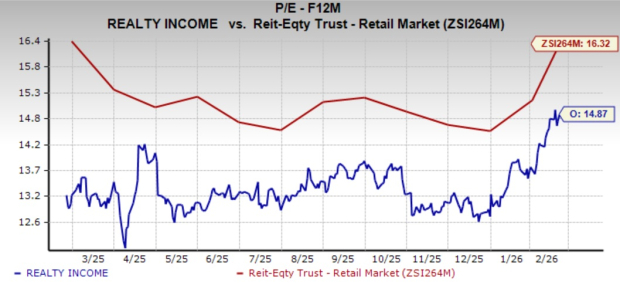

Valuation-wise, Realty Income trades at a forward price-to-FFO of 14.87X, below the retail REIT industry average of 16.32X and slightly above its one-year median of 13.23X. The stock appears reasonably priced versus its peers. It is cheaper than Agree Realty Corporation ADC yet pricier than NNN REIT NNN. Agree Realty is trading at a forward 12-month price-to-FFO of 17.14X, while NNN is trading at 12.44X. However, its Value Score of D suggests that it may not be a bargain at current levels.

Forward 12 Month Price-to-FFO (P/FFO) Ratio

Realty Income remains a reliable choice for investors focused on steady income and capital preservation. The company benefits from a large, diversified property base, a tenant roster concentrated in essential businesses and long-term net leases that provide predictable rental revenues. Ongoing efforts to broaden its investment scope beyond traditional retail add durability to the model. A healthy dividend yield and an investment-grade balance sheet further support its reputation as a defensive REIT.

The stability that defines Realty Income limits its growth pace. Same-store revenue typically increases at a measured rate, and the structure of long-duration net leases caps earnings acceleration when economic conditions are strong. In addition, the company’s broad diversification, while reducing risk, can dilute exposure to higher-growth property niches, which are likely to have modestly restrained near-term upside.

The stock trades at a slight discount to peers such as Agree Realty and a premium to NNN, reflecting measured expectations.

With a balanced risk-reward setup, holding the shares appears reasonable. Current investors can continue collecting dependable dividends, while new buyers may wait for a more compelling valuation.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-07 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 | |

| Jun-30 | |

| Jun-29 | |

| Jun-25 | |

| Jun-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite