|

|

|

|

|||||

|

|

|

LendingClub Corporation LC and Pagaya Technologies Ltd. PGY operate in the same consumer credit ecosystem but with different business models. Both use advanced data analytics and technology to broaden credit access and enhance underwriting, often serving borrowers outside traditional prime categories. They also depend on capital markets and institutional funding to drive loan growth, making them sensitive to similar macro factors, such as credit demand, funding conditions and investor appetite for consumer loan assets.

However, while LendingClub operates as a regulated digital marketplace bank, originating personal loans and retaining some on its balance sheet through LendingClub Bank, PGY does not lend directly. Instead, it uses an artificial intelligence (AI)-powered network to partner with banks and fintech firms to underwrite and purchase loans that might otherwise be declined.

Thus, LendingClub’s earnings profile is more tied to credit performance, deposit costs and balance sheet management, whereas Pagaya’s model is more asset-light and capital-market-driven, with performance closely linked to loan volume across its partner network and securitization demand.

Now, let us see which of the two consumer credit firms, LendingClub or Pagaya, has greater upside potential. In order to understand this, we must dig deep into their fundamentals and growth prospects.

PGY has a capital-light, flexible operating model, which initially centered on personal lending, but the company has since broadened its reach into auto loans and point-of-sale financing. This expansion has spread risk across multiple asset classes, reducing the dependence on any single loan segment and supporting performance through varying economic conditions. On the funding side, PGY has cultivated relationships with more than 135 institutional investors and relies on forward-flow agreements, under which partners commit capital for future loan purchases. These arrangements enhance funding predictability and provide a buffer against market volatility.

A key differentiator is PGY’s proprietary tech and product suite. Its pre-screen solution allows lenders to present pre-approved offers to existing customers without formal applications, helping partners boost credit access and deepen relationships with minimal marketing spend.

Pagaya operates with minimal on-balance-sheet exposure. Loans are typically acquired immediately by asset-backed securities (ABS) vehicles or via forward flow agreements, thanks to capital raised in advance. This approach limits credit and market risk, preserving flexibility during turbulent environments. By relying on forward flow agreements and strategic ABS issuance, Pagaya has maintained liquidity and minimized loan write-downs.

In 2025, Pagaya hit an inflection point with improving fundamentals and profitability. Despite macroeconomic headwinds and regulatory risks, the company posted all four quarters of positive GAAP net income, a dramatic turnaround from substantial losses in the previous years. For the year, net income was a record $81.4 million against a net loss of $401.4 million incurred in 2024. The company reported solid total revenue and other income growth (rising 26.1% year over year), driven largely by higher fee income across its lending network. The adjusted EBITDA rose sharply (up 76.3% year over year), showing that the platform scaled efficiently as utilization increased.

Driven by both portfolio seasoning and structural changes in funding and underwriting, PGY’s credit-related losses and impairments improved drastically in 2025 from the 2024 reported levels. Lower impairments reflect better-performing loan vintages, more stable delinquency and charge-off trends, and improved accuracy of PGY’s AI-driven underwriting models.

LC’s earnings are fundamentally powered by a hybrid business model that blends a capital-light marketplace lending platform with a deposit-funded bank balance sheet. The marketplace channel generates fee-based revenue from loan originations and sales to institutional investors, which is highly scalable and reacts quickly to demand in the credit markets. Conversely, the bank balance sheet provides recurring net interest income (NII) from loans it retains, funded by customer deposits.

Of late, LendingClub has demonstrated robust growth in loan origination volumes, which directly drives revenues. In 2025, the company reported a 33% year-over-year increase in origination volumes, with total net revenues rising 23%, supported by both higher marketplace activity and an increased net interest margin on its balance sheet. NII reached record levels and marketplace revenues climbed significantly as pricing and volumes improved.

While LendingClub’s most transformative acquisition was Radius Bank in 2020, which enabled its shift into a regulated digital marketplace bank, the company has continued to acquire targeted technology assets. In 2024, LC joined PGY to acquire the intellectual property of Tally Technologies, a credit card management platform, aimed at expanding member tools for debt management and boosting engagement.

Later, LendingClub acquired the assets of a spending intelligence platform, building on the Tally acquisition to provide deeper visibility into financial obligations and better analytics for consumers.

A strong capital position allows LC to grow its balance sheet organically without excessive dilution. The company has developed diversified funding partnerships, including large commitments from Blue Owl and structured certificates involving BlackRock, to support loan originations without overreliance on a single funding source. Its deposit base, largely FDIC-insured and grown through products like high-yield savings accounts and checking, serves as a low-cost funding engine for balance-sheet growth.

In the past year, shares of Pagaya have lost 6.5%, whereas the LC stock has gained 28.5%. Hence, in terms of investor sentiments, LC has the edge.

From a valuation perspective, Pagaya is currently trading at a trailing 12-month price-to-book (P/B) of 1.78X, while the LC stock is trading at a trailing 12-month P/B of 1.24X. So, in terms of valuation, PGY is expensive compared with LendingClub.

Pagaya’s return on equity (ROE) of 44.45% is above LendingClub’s 9.47%. This reflects that PGY is more efficient in using shareholder funds to generate profits.

The Zacks Consensus Estimate for PGY’s 2026 and 2027 revenues indicates year-over-year growth of 14.3% and 15.3%, respectively.

The consensus estimate for PGY’s 2026 earnings suggests a year-over-year decline of 13.3%. For 2027, its earnings estimate indicates 25.8% growth.

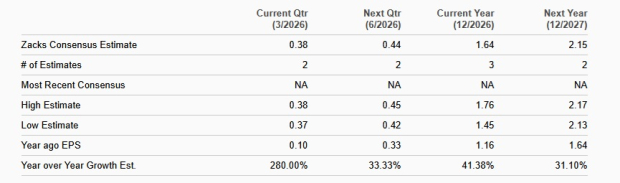

On the contrary, the Zacks Consensus Estimate for LC’s 2026 and 2027 revenues implies year-over-year increases 6.2% and 8.7%, respectively.

The consensus estimate for LendingClub’s earnings indicates 41.4% growth for 2026 and a 31.1% rise for 2027.

Given its resilient business model and capital-efficient funding strategy, PGY stands out in the fintech space. Its AI-driven platform and reliance on forward flow agreements shield it from market volatility and credit risks.

However, despite moving into profitability last year, there is uncertainty about the company’s prospects because of the outlook that management provided along with its fourth-quarter 2025 results, which signals slower near-term expansion. The company’s decision to tighten underwriting standards may improve long-term credit quality, but it immediately reduces lending volumes and growth momentum.

At present, LendingClub appears more attractive than Pagaya. Its hybrid bank-backed lending model delivers steadier earnings, stronger fundamentals and clearer cash flow visibility at a lower valuation. LC’s established revenue streams and lower risk profile make it a more compelling choice for investors seeking value and stability over higher-volatility growth.

PGY currently carries a Zacks Rank #4 (Sell), while LendingClub sports a Zacks Rank #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 | |

| Jul-09 | |

| Jun-30 | |

| Jun-15 | |

| Jun-11 | |

| Jun-10 | |

| Jun-08 | |

| Jun-02 | |

| Jun-02 | |

| Jun-01 | |

| Jun-01 | |

| May-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite