|

|

|

|

|||||

|

|

|

Netflix NFLX delivered a strong fourth quarter of 2025, but the road ahead is defined by a deliberate tradeoff: spend more to grow more. Whether that calculus works in investors' favor depends on how well the streaming giant executes on a content-heavy 2026 strategy that is already testing the market's patience.

For the fourth quarter, Netflix reported revenues of $12.05 billion, up 18% year over year, while operating income rose 30% to $2.96 billion, with operating margin expanding to 24.5%. The company ended the year with 325 million paid subscribers and generated $9.5 billion in free cash flow for full-year 2025, surpassing its own guidance of $9 billion. Full-year 2025 revenues reached $45 billion, with an operating margin of 29.5%, up from 26.7% in 2024.

For 2026, Netflix projects revenues between $50.7 billion and $51.7 billion, suggesting 12% to 14% growth and a 31.5% operating margin. However, that margin target factors in roughly $275 million in acquisition-related expenses tied to its pending deal for Warner Bros. Studios and HBO, as well as roughly 10% year-over-year growth in content amortization. The company has also paused its share buyback program to preserve cash for the acquisition, having repurchased $2.1 billion in shares during the fourth quarter alone.

Content spending is deliberately front-loaded in the first half of 2026, which the company says will pressure operating income early in the year before recovering in the second half. The near-term slate reflects this investment: March 2026 alone features Peaky Blinders: The Immortal Man, the second season of live-action One Piece, Virgin River Season 7, the MLB Opening Night live event, and a BTS comeback special — a mix of prestige drama, live sports, and global content designed to sustain engagement across its subscriber base.

Advertising revenues, which grew 2.5 times in 2025, are projected to roughly double again to approximately $3 billion in 2026, representing a growing but still modest contribution to overall revenues. Free cash flow guidance stands at approximately $6 billion for the year, a notable step down from 2025's $9.5 billion, reflecting the elevated investment cycle.

For investors, Netflix presents a company with clear revenue momentum and a well-defined content engine, offset by rising cost commitments, acquisition uncertainty, and a compressed free cash flow outlook that warrants careful monitoring heading into the year.

Netflix is not alone in navigating the tension between content investment and profitability. Amazon AMZN, through its Prime Video unit, continues to scale content spending as part of a broader subscription and advertising strategy, with Amazon committing billions annually to originals and live sports rights, including its NFL Thursday Night Football deal. Disney DIS, meanwhile, has been moving in the opposite direction — actively pulling back on content costs as Disney pursues a path toward sustained streaming profitability. While Amazon prioritizes content volume to drive Prime ecosystem value, Disney has leaned on franchise depth and cost discipline, underscoring how differently Amazon and Disney are approaching the same challenge Netflix faces.

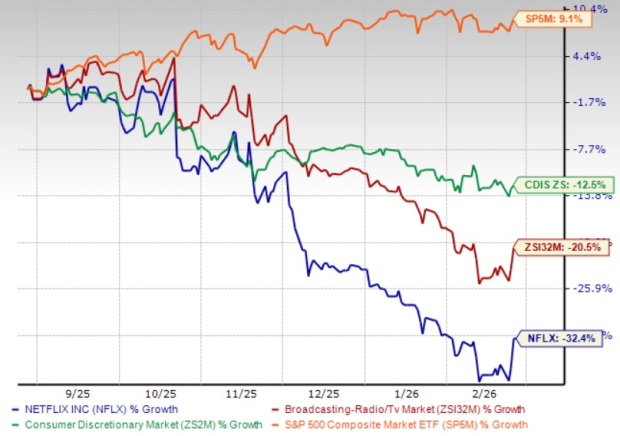

Shares of Netflix have plunged 32.4% in the past six-month period compared with the Zacks Broadcast Radio and Television industry’s decline of 20.5%.

From a valuation standpoint, Netflix appears overvalued, trading at a forward 12-month price-to-sales ratio of 6.7X compared with the broader Zacks Broadcast Radio and Television industry's forward sales multiple of 4.04X. NFLX carries a Value Score of C.

The Zacks Consensus Estimate for NFLX’s 2026 revenues is pegged at $51.91 billion, suggesting 13.3% year-over-year growth. The consensus mark for 2026 earnings is pegged at $3.12 per share, indicating a 23.23% increase from the previous year.

Netflix, Inc. price-consensus-chart | Netflix, Inc. Quote

NFLX stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite