|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

SentinelOne S shares have plunged 22.7% over the past three months, underperforming both the Zacks Security industry's 3% dip and the broader Zacks Computer & Technology sector's 14.2% slide.

Despite its position as a key player in endpoint security—leveraging AI-driven tools to protect network-connected devices across a wide cybersecurity platform—the stock has stumbled, now sitting 38.6% below its 52-week high of $29.29.

SentinelOne’s 3-Month Price Performance

The technical setup is also currently cautious. The stock has been under pressure and remains below key moving averages (50-day and 200-day) – a bearish sign signaling downward momentum. In fact, trading under both the 50-day and 200-day simple moving averages implies that rallies have been limited and sellers still have the upper hand.

SentinelOne has underperformed industry peers, including Okta OKTA, CrowdStrike CRWD and Fortinet FTNT, over the same timeframe. Okta, CrowdStrike and Fortinet shares have appreciated 11.7%, 10.8% and 4.1%, respectively.

SentinelOne has projected 23% revenue growth for fiscal 2026, sharply down from the previous year's 32% growth rate. This slowdown came in below analyst expectations and raises concerns about potential valuation pressure, especially for a company viewed as a high-growth cybersecurity player. Management pointed to sales execution issues and ongoing transitions in its go-to-market strategy as contributing factors to the reduced outlook.

Although the company added more than 500 new customers and maintained a healthy 115% net revenue retention rate, it experienced a sequential decline in revenue per customer. This trend signals weak upsell momentum and challenges in expanding within existing accounts—an issue that undermines the company’s land-and-expand model and long-term growth scalability.

Amid persistent market volatility fueled by trade policy uncertainties, inflation concerns, and changing consumer sentiment, the question remains: can SentinelOne stage a comeback in the face of these headwinds?

SentinelOne is facing a pivotal moment as it grapples with slowing growth and execution challenges. However, its platform diversification will drive growth momentum. The company is undergoing a successful transformation from an endpoint-centric business to a broader AI-native cybersecurity platform. In the fiscal fourth quarter, more than 50% of bookings came from non-endpoint products, including cloud, data, and AI solutions. SentinelOne’s Singularity Platform, now spanning seven solution areas, saw accelerating adoption — 40% of enterprise customers used three or more solution categories, and 20% used four or more. Flagship offerings like AI SIEM and Purple AI gained substantial traction, contributing significantly to platform wins, customer expansion, and competitive displacements.

SentinelOne continued to lead with innovation, notably through Purple AI—its generative AI capability now embedded by default across the Singularity platform. The company executed more than 300 Purple AI-related deals during the fiscal fourth quarter, highlighting strong adoption. Its AI SIEM platform also helped clients cut costs and improve response times, supporting competitive wins. Cloud security remained another growth pillar, with the fiscal fourth quarter marking the largest CNAPP deal since the PingSafe acquisition.

The company emphasized robust momentum in international markets, including EMEA and APJ, which together contributed significantly to new business growth in the fiscal fourth quarter. Additionally, SentinelOne's FedRAMP Moderate In Process designation and traction within the U.S. public sector indicate untapped opportunities in highly regulated verticals. These segments could drive incremental growth and revenue diversification moving forward.

Annual recurring revenue (ARR) grew 27% year over year to $920 million, with $60 million in net new ARR added in the quarter. This marked a turnaround from the slower first half of fiscal 2025 and showcased improved execution. However, some churn—particularly due to the planned retirement of the legacy deception product—muted headline ARR numbers. Adjusting for that impact, quarterly net new ARR grew in the mid-single digits, pointing to underlying strength in upsells and new business wins.

SentinelOne's win rates improved in the fiscal fourth quarter, with large customer acquisitions including a Fortune 100 airline and significant deals replacing legacy SIEM providers like Splunk. The company also deepened relationships with managed security service providers, helping expand recurring revenue visibility and contributing to record RPO (remaining performance obligations), which grew 30% to $1.2 billion.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at 18 cents per share, unchanged over the past 60 days. That said, the estimated figure calls for 260% growth from a year ago.

SentinelOne’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters, missing in one occasion, the average surprise being 125.0%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

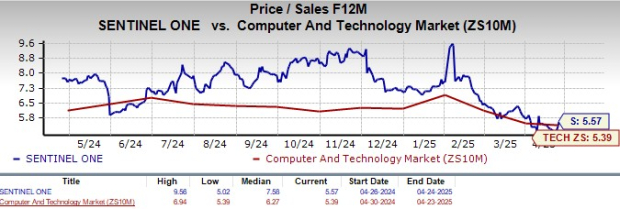

From a valuation standpoint, the company is currently trading at a slight premium relative to its industry. In terms of the forward 12-month price-to-sales (P/S) ratio, SentinelOne is trading at 5.57X, higher than the sector’s 5.39X.

SentinelOne’s stock has underperformed recently, reflecting growth deceleration, sales execution issues, and technical weakness. However, the company is making notable progress in evolving beyond endpoint security, with growing traction in AI-driven products like Purple AI and cloud security. Strong ARR growth, international expansion, and improved customer wins point to early signs of recovery. While short-term challenges persist, its innovation, platform diversification, and long-term potential justify its Zacks Rank#3 (Hold) as the company works through its transition. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-22 |

Anthropic Jolts Cybersecurity Stocks, JFrog After Finance, Health Care, Legal Drama

CRWD

Investor's Business Daily

|

| Feb-22 | |

| Feb-22 | |

| Feb-22 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite