|

|

|

|

|||||

|

|

|

Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at Shoe Carnival (NASDAQ:SCVL) and its peers.

Footwear sales–like their apparel counterparts–are driven by seasons, trends, and innovation more so than absolute need and similarly face the bigger-picture secular trend of e-commerce penetration. Footwear plays a part in societal belonging, personal expression, and occasion, and retailers selling shoes recognize this. Therefore, they aim to balance selection, competitive prices, and the latest trends to attract consumers. Unlike their apparel counterparts, footwear retailers most sell popular third-party brands (as opposed to their own exclusive brands), which could mean less exclusivity of product but more nimbleness to pivot to what’s hot.

The 4 footwear retailer stocks we track reported a slower Q4. As a group, revenues missed analysts’ consensus estimates by 1.7% while next quarter’s revenue guidance was 0.6% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 27% since the latest earnings results.

Known for its playful atmosphere that features carnival elements, Shoe Carnival (NASDAQ:SCVL) is a retailer that sells footwear from mainstream brands for the entire family.

Shoe Carnival reported revenues of $262.9 million, down 6.1% year on year. This print fell short of analysts’ expectations by 2.7%. Overall, it was a softer quarter for the company with full-year EPS guidance missing analysts’ expectations.

“I would like to thank our team members and brand partners for their exceptional contributions to our growth during Fiscal 2024. We achieved the very top end of our annual profit guidance and drove solid sales growth despite a challenging economic landscape. Shoe Station expanded at a pace that made it the fastest growing retailer in our industry once again. We rapidly captured full synergies from our Rogan’s acquisition and grew our sales during key event periods throughout the year,” said Mark Worden, President and Chief Executive Officer.

Shoe Carnival delivered the slowest revenue growth and weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 20.8% since reporting and currently trades at $17.95.

Read our full report on Shoe Carnival here, it’s free.

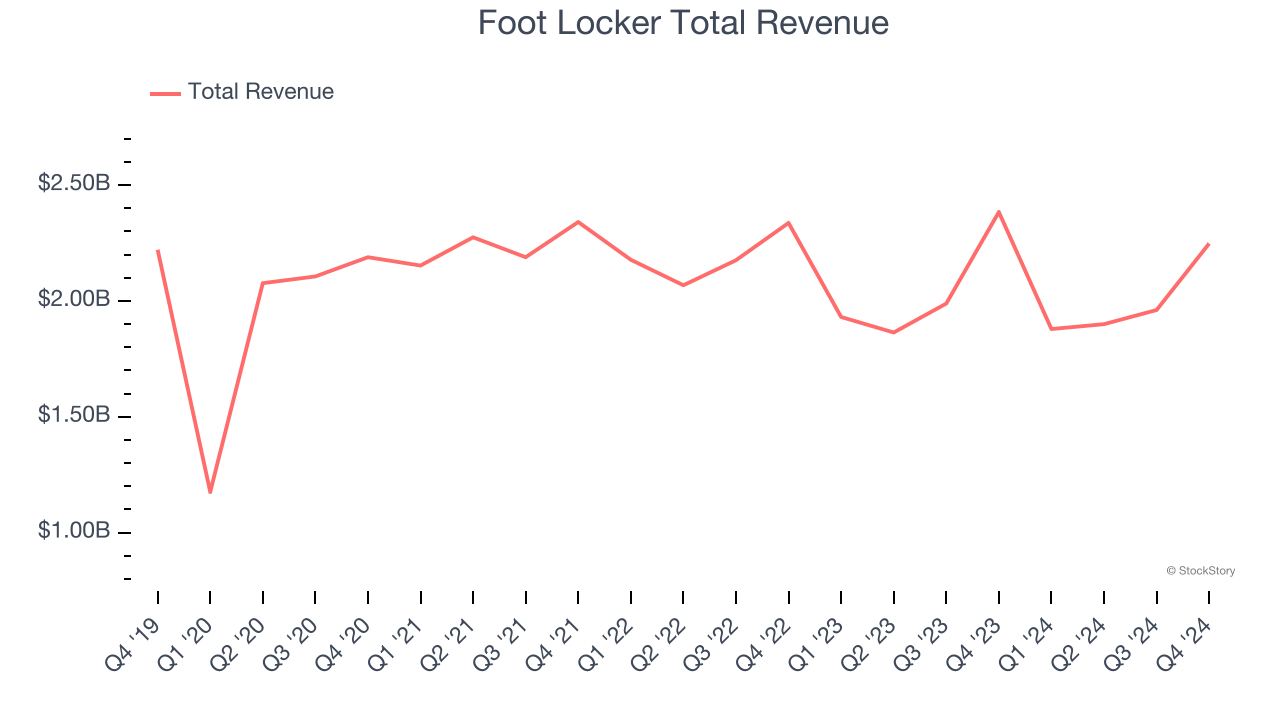

Known for store associates whose uniforms resemble those of referees, Foot Locker (NYSE:FL) is a specialty retailer that sells athletic footwear, clothing, and accessories.

Foot Locker reported revenues of $2.25 billion, down 5.7% year on year, falling short of analysts’ expectations by 3.2%. The business performed better than its peers, but it was unfortunately a mixed quarter with a solid beat of analysts’ EBITDA estimates but full-year EPS guidance missing analysts’ expectations significantly.

The stock is down 25.5% since reporting. It currently trades at $12.94.

Is now the time to buy Foot Locker? Access our full analysis of the earnings results here, it’s free.

Founded in 1969 as a shoe importer and distributor, Designer Brands (NYSE:DBI) is an American discount retailer focused on footwear and accessories.

Designer Brands reported revenues of $713.6 million, down 5.4% year on year, falling short of analysts’ expectations by 0.8%. It was a disappointing quarter as it posted full-year EPS guidance missing analysts’ expectations.

As expected, the stock is down 21.2% since the results and currently trades at $2.99.

Read our full analysis of Designer Brands’s results here.

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE:BOOT) is a western-inspired apparel and footwear retailer.

Boot Barn reported revenues of $608.2 million, up 16.9% year on year. This print met analysts’ expectations. More broadly, it was a mixed quarter as it also produced a decent beat of analysts’ EBITDA estimates but EPS guidance for next quarter missing analysts’ expectations.

Boot Barn scored the biggest analyst estimates beat, fastest revenue growth, and highest full-year guidance raise among its peers. The stock is down 40.6% since reporting and currently trades at $103.69.

Read our full, actionable report on Boot Barn here, it’s free.

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite