|

|

|

|

|||||

|

|

|

Shopify SHOP is currently overvalued, as suggested by a Value Score of F.

In terms of the 12-month Price/Sales, SHOP is currently trading at 11.10X compared with the broader Computer & Technology sector’s 5.58X.

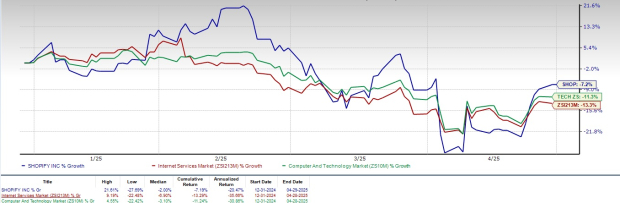

SHOP shares have plunged 7.2% in the year-to-date period compared with the broader Zacks Computer & Technology sector’s decline of 11.3%. The Zacks Internet - Services industry has risen 13.3% in the same time frame.

The company’s share price movement has declined due to increasing macroeconomic challenges driven by U.S. President Donald Trump’s decision to impose tariffs on top trading partners, including China, Mexico and Canada, which has increased the chances of a trade war.

However, the share price movement can be attributed to robust growth in its merchant base, driven by its merchant-friendly tools, including Shop Pay, Shopify Pay Instalments, Sign in with Shop and the Shop App. The strong adoption of these solutions is enabling Shopify to attract merchants, even amid challenging economic conditions.

Shopify’s expanding portfolio has been a key catalyst. Its merchant-friendly tool Shop Pay stands out as a key driver. The app processed $27 billion in gross merchandise value in the fourth quarter of 2024, up 50% year over year. It now represents 41% of gross payment volume, boosting Shopify’s transaction volume.

Shopify’s investment in AI-driven tools like Shopify Sidekick and Shop Inbox is helping merchants improve customer engagement and streamline operations. By leveraging AI, Shopify makes its platform more powerful and user-friendly.

Shopify’s expanding footprint in the B2B space has been noteworthy. In the fourth quarter of 2024, it saw 132% growth in B2B Gross Merchandise Value, marking an impressive performance in a growing market for the platform.

Building on this momentum, Shopify recently announced a suite of new partner solutions tailored for B2B businesses. These solutions offer advanced storefront solutions, seamless back-office integrations, and native apps designed to speed up digital commerce for manufacturers and distributors. These solutions aim to streamline operations and enhance the B2B buying experience with faster time-to-market and lower costs.

Shopify's rich partner ecosystem has been a major growth driver. The company continues to benefit from its partnerships with prominent names like TikTok, Instagram, Target, PayPal PYPL, Roblox RBLX, Alphabet, Manhattan Associates, Oracle, COACH and Adyen.

Through its expanded partnership with PayPal, SHOP is diversifying its Payments product offerings, providing merchants with more flexibility in payment solutions. This expanded collaboration with PayPal further enhances Shopify’s ability to offer comprehensive financial tools for its global merchant base.

In its commerce integration partnership with Roblox, Shopify has opened new avenues for merchants to reach a younger and more engaged audience. This collaboration with Roblox allows Shopify to strengthen its position in the digital commerce space.

The Zacks Consensus Estimate for SHOP’s 2025 earnings is currently pegged at $1.45 per share, unchanged over the past 30 days and indicating year-over-year growth of 11.54%.

The consensus mark for SHOP’s 2025 revenues is currently pegged at $10.77 billion, indicating year-over-year growth of 21.26%.

Shopify Inc. price-consensus-chart | Shopify Inc. Quote

SHOP beat the Zacks Consensus Estimate for earnings in each of the trailing four quarters, the average surprise being 22.08%.(Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Shopify is facing stiff competition in the e-commerce marketplace against the likes of Alibaba and Amazon AMZN.

Shopify’s acquisition of Deliverr, a startup fulfillment service, makes it a direct competitor of Amazon. Additionally, Amazon’s “Buy with Prime”, which combines its payments and fulfillment services and makes them available at checkout on other websites and promises faster delivery for Prime members, intensifies competition for Shopify.

SHOP is benefiting from strong growth in its merchant base and expanding footprint. Its focus on improving its client base is a key catalyst. Hence, investors who already own the stock may expect the company’s growth prospects to be rewarding over the long term.

However, challenging macroeconomic conditions and a cautious spending environment are headwinds along with a stretched valuation.

Stiff competition has also been a headwind. Shopify plans to shift to a three-month paid trial in certain markets compared with its previous one-month paid trial practice to boost merchant durability and retention. This negatively impacted fourth-quarter Monthly Recurring Revenue (MRR) growth and is expected to hurt the first quarter of 2025 and the second quarter of 2025 MRRs.

Shopify currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable time to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 31 min | |

| 46 min | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 5 hours | |

| 6 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite