|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

General Motors GM has lowered its 2025 earnings forecast, warning that new U.S. auto tariffs could cost the company $4-$5 billion. The updated guidance, released yesterday, comes two days after the company released its first-quarter results and withdrew its previous outlook, which didn’t take tariffs into account. It has also temporarily suspended the buyback of shares amid uncertainty. The move reflects rising pressure from global trade tensions, as Trump’s tariffs target foreign-built vehicles and parts.

GM’s closest peer Ford F will release results next week and chances are high that it will also slash its 2025 view. Ford’s previous outlook also didn’t take into account tariffs and the company’s CEO had already warned that tariff headwinds would cause a lot of chaos in the auto industry. U.S. motorcycle giant Harley-Davidson HOG has also withdrawn its guidance amid macroeconomic and tariff uncertainties.

GM, which holds the title of the top-selling automaker in the United States, now expects lower profit, cash flow, and earnings compared to earlier projections. After this revised guidance, investors might be wondering if it’s still worth holding onto the stock. Before we discuss that, let’s take a look at the revised guidance and see how General Motors is positioning itself to weather the tariff storm.

GM now expects adjusted EBIT in 2025 to range between $10 billion and $12.5 billion, down from its prior guidance of $13.7-$15.7 billion. Net income attributable to shareholders is expected to fall and be in the range of $8.2 billion to $10.1 billion compared with the earlier forecast of $11.2-$12.5 billion. Adjusted automotive free cash flow is also expected to be hit and is now projected in the range of $7.5-$10 billion, lower than $11-$13 billion guided earlier.

One of the biggest contributors to the downward revision is a projected $2 billion business hit from South Korea. Vehicles like the Buick Encore GX, Buick Envista, Chevrolet Trailblazer and Chevrolet Trax are all assembled there and made up nearly 18% of GM’s first-quarter vehicle sales. GM also cited lingering exposure to manufacturing facilities in Canada and Mexico.

At the end of the first quarter of 2025, GM had $4.3 billion repurchase capacity remaining. But it has put a temporary freeze on additional repurchases until there is more clarity on the tariff impact.

Analysts have started to make downward revisions to General Motors’ EPS forecasts for 2025 and more cuts might be on the way.

General Motors believes it can offset up to 30% of expected tariff-related costs through what it calls “self-help initiatives,” which have been accounted for in the updated guidance. These initiatives include ramping up U.S.-based vehicle and battery module production and tightening compliance with USMCA sourcing requirements.

CEO Mary Barra emphasized GM’s multi-year shift toward a more U.S.-centric manufacturing footprint. Since 2019, the company has raised its U.S. direct purchases by 27%, with more than 80% of U.S.-built vehicle content now meeting USMCA standards. Simultaneously, GM has drastically reduced its reliance on China for direct materials to under 3%, aligning its supply chain with evolving trade dynamics.

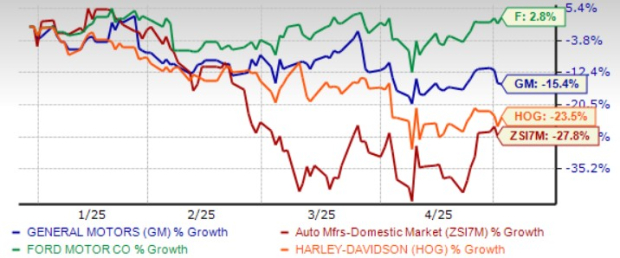

Year to date, shares of General Motors have declined 15%, outperforming the industry. The decline is also lower than Harley-Davidson, whose shares have plunged 23% so far in 2025. Meanwhile, Ford has gained 2.8% in the same timeframe.

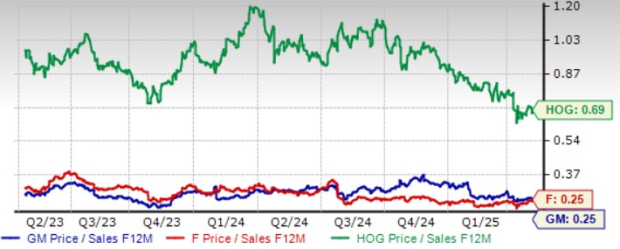

From a valuation standpoint, General Motors appears relatively undervalued. The stock trades at a forward price-to-sales (P/S) ratio of just 0.25, well below the industry average of 2.19. GM also boasts a Value Score of A, highlighting its attractive valuation. In comparison, Harley-Davidson trades at a P/S ratio of 0.69, while Ford’s multiple matches GM’s at 0.25.

GM is facing some short-term challenges, but its long-term strategy remains on track. It is on course with its long-term electric vehicle (EV) strategy. The company was the #2 EV seller in the United States, with Chevrolet becoming the fastest-growing EV brand in the market.

Importantly, GM’s EV lineup turned “variable profit positive” by late 2024, meaning it now covers its production costs. The company expects to cut EV-related losses further this year.

Financially, GM remains in solid shape. It finished the first quarter with $20.7 billion in cash and cash equivalents. Its restructuring efforts in China have started to show progress, with the company targeting a return to profitability in those regions.

The company remains profitable and committed to long-term growth, but near-term risks are clearly rising. Much will depend on how effectively GM can reduce the impact of tariffs and keep its costs under control.

Yes, tariffs will put pressure on GM’s margins this year and the recent halt in stock buybacks may shake investor confidence. Lowered earnings estimates could also weigh on sentiment in the near term. However, for long-term investors, GM’s story is far from broken. The company is managing costs, advancing in EVs, and still generating strong cash flow.

So, if you are thinking of selling the stock, it may be too soon. GM still has the fundamentals and the strategy to deliver over time. It currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

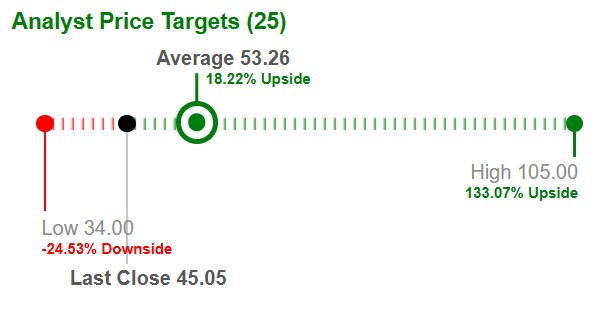

The Wall Street average target price for General Motors is $53.46, suggesting an 18.2% upside.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours |

Detroit Automakers Raise Concern to White House About Potential New Tariffs

F GM

The Wall Street Journal

|

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours | |

| 11 hours | |

| 14 hours | |

| 15 hours | |

| 16 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite