|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

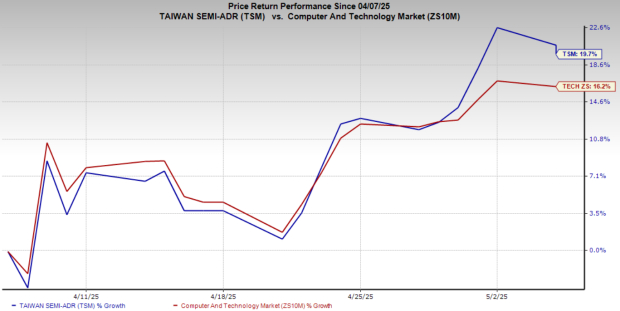

Taiwan Semiconductor Manufacturing Company TSM has seen its share price soar 19.7% over the past month. This surge has significantly outperformed the broader Zacks Computer and Technology sector, which gained 16.2% during the same period.

This outperformance raises the question: Should investors book profits and exit, or continue holding the stock?

Taiwan Semiconductor Manufacturing’s recent rally stemmed from broader market optimism. Whispers of progress in U.S.-China trade negotiations significantly boosted market sentiment in late April. Protracted trade tensions had previously dampened global economic forecasts and corporate earnings expectations due to tariffs and retaliatory measures.

Hints of a potential deal suggested easing tensions, possible tariff reductions and smoother international trade flows. This improved outlook fostered investor confidence, leading to a rally in the equity market as fears of further economic disruption subsided and prospects for global growth seemed brighter.

Semiconductor stocks, including Taiwan Semiconductor Manufacturing, Broadcom, Inc. AVGO, Marvell Technology, Inc. MRVL and NVIDIA Corporation NVDA, were the prime gainers from this rally as they had witnessed a tremendous selloff previously following the Trump administration’s reciprocal tariff announcement on April 2. Over the past month, shares of Broadcom, Marvell Technology and NVIDIA soared 30.5%, 21.2% and 16.3%, respectively.

Taiwan Semiconductor Manufacturing’s long-term growth potential, along with invigorated investor optimism, makes the stock worth holding at the moment.

Taiwan Semiconductor Manufacturing continues to dominate the semiconductor foundry space with its technological superiority and production scale. The ongoing artificial intelligence (AI) boom has placed Taiwan Semiconductor at the center of a multi-year structural growth cycle.

The company has established itself as the preferred manufacturing partner for AI accelerators, including graphics processing units (GPUs) and custom silicon developed by major players like NVIDIA, Marvell Technology and Broadcom.

In 2024, AI-related revenues tripled, making up a mid-teen percentage of Taiwan Semiconductor Manufacturing’s total revenues, and the momentum is far from over. The company expects AI-related sales to double again in 2025, with an impressive 40% compound annual growth rate over the next five years. This positions TSM as the undisputed backbone of AI-driven technological advancements.

Taiwan Semiconductor Manufacturing has started 2025 on a strong note by reporting overwhelming first-quarter results, wherein revenues surged 35% year over year to $25.53 billion, while net income jumped 53% to nearly $11 billion. This growth was driven by explosive demand for its 3nm and 5nm nodes, which together contributed nearly 58% of total wafer revenues.

Taiwan Semiconductor Manufacturing’s first-quarter EPS also jumped 53.6% to $2.12 and surpassed the Zacks Consensus Estimate of $2.03. The stock beat the consensus mark for earnings in each of the trailing four quarters, the average surprise being 6.9%.

Taiwan Semiconductor Manufacturing Company Ltd. price-consensus-eps-surprise-chart | Taiwan Semiconductor Manufacturing Company Ltd. Quote

Taiwan Semiconductor Manufacturing is not only growing but also scaling at an unprecedented pace to capitalize on the AI-driven growing demand for advanced chips. The company is set to invest between $38 billion and $42 billion in capital expenditures in 2025, far outpacing its $29.8 billion investment in 2024. The bulk of this spending, around 70%, is focused on advanced manufacturing processes, ensuring TSM stays ahead of the curve.

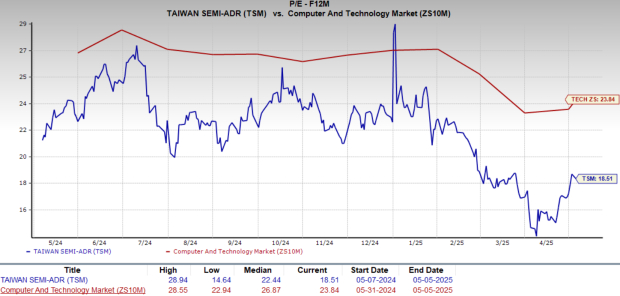

Taiwan Semiconductor Manufacturing trades at a forward 12-month price-to-earnings (P/E) ratio of 18.51, below the sector average of 23.84. This reasonable valuation, coupled with the company’s growth potential, offers an appealing entry point for investors seeking exposure to the semiconductor sector.

Taiwan Semiconductor Manufacturing also trades at a lower P/E ratio than other semiconductor players, including Broadcom, Marvell Technology and NVIDIA. At present, Broadcom, Marvell Technology and NVIDIA trade at P/E ratios of 27.74, 20.95 and 24.8, respectively.

Despite its strengths, Taiwan Semiconductor Manufacturing faces near-term headwinds. Higher energy prices in Taiwan, following a 25% electricity hike in 2024, pose a considerable challenge, especially as advanced nodes demand greater power.

Softness in key markets like PCs and smartphones also dampens near-term prospects. These traditionally strong revenue drivers are projected to see only low single-digit growth in 2025, limiting Taiwan Semiconductor Manufacturing’s growth despite rising AI demand.

Additionally, rising operational costs, especially from its overseas expansion into Arizona, Japan and Germany, are other concerns. These new facilities, while strategically important for diversification, are expected to dilute gross margins by 2-3% annually over the next three to five years due to higher labor and utility costs, coupled with lower initial utilization rates.

Geopolitical tensions, particularly between the United States and China, further cloud the outlook. With significant revenue exposure to China, export restrictions and supply-chain disruptions could pressure Taiwan Semiconductor Manufacturing’s operations.

Taiwan Semiconductor Manufacturing’s technological leadership and strategic investments make it a compelling long-term player in the semiconductor space. However, short-term challenges, including rising costs, tariff wars and geopolitical risks, warrant caution. For now, holding TSM stock remains the most prudent strategy, allowing investors to benefit from its industry leadership while navigating near-term uncertainties.

Currently, Taiwan Semiconductor Manufacturing carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 18 min |

How Will Dow Jones Futures React After Trump Hikes Global Tariff To 15%?

TSM NVDA

Investor's Business Daily

|

| 47 min | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite