|

|

|

|

|||||

|

|

|

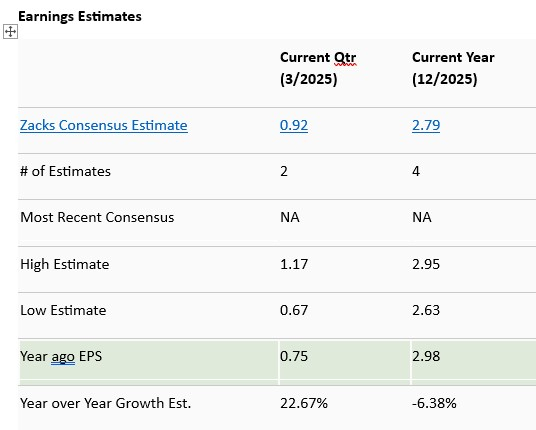

Petroleo Brasileiro S.A., or Petrobras PBR, is slated to release first-quarter 2025 results on May 12. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings per share (EPS) and revenues is pegged at 92 cents and $21.7 billion, respectively. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

The earnings estimates for the to-be-reported quarter have been revised downward by 14% over the past 30 days. The bottom-line projection indicates an improvement of 22.7% from the year-ago reported number. The Zacks Consensus Estimate for quarterly revenues, however, suggests a year-over-year decrease of 8.7%.

For full-year 2025, the Zacks Consensus Estimate for Petrobras’ revenues is pegged at $83.9 billion, implying a fall of 8.2% year over year. The consensus mark for 2025 EPS is pegged at $2.79, indicating a contraction of around 6.4%.

In the trailing four quarters, the Rio de Janeiro-based Brazil's state-run energy giant surpassed EPS estimates twice, met once and missed in the other, as reflected in the chart below.

Petroleo Brasileiro S.A.- Petrobras price-eps-surprise | Petroleo Brasileiro S.A.- Petrobras Quote

Petrobras is the largest integrated energy firm in Brazil and one of the largest in Latin America. The company’s activities include: exploration, exploitation and production of oil from reservoir wells, shale and other rocks, as well as refining, processing, trading and transportation of oil and oil products, natural gas and other fluid hydrocarbons, in addition to other energy-related activities.

Our proven model does not conclusively predict an earnings beat for Petrobras this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Earnings ESP: PBR has an Earnings ESP of 0.00%.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Per its ‘Production and Sales Report’ issued late last month, Petrobras is likely to have experienced a marginal 0.2% year-over-year drop in oil and gas production to 2.77 million barrels of oil equivalent per day (boed) in the first quarter of 2025, signaling a relatively flat performance despite operational improvements. Crude oil output in Brazil declined by 1% to 2.21 million bpd, partially offset by the addition of 11 new wells and the start-up of the Almirante Tamandaré FPSO at the Búzios field. The Campos and Santos Basins also contributed new volumes. While these additions boosted capacity, the company continued to face natural field decline, which tempered growth. Nonetheless, output remained within Petrobras’ annual production guidance of ±4% around a 2.8 million boed target, reflecting disciplined operations in a sluggish macroeconomic backdrop.

On the commercial side, Petrobras experienced notable softness, with total oil, gas, and derivatives sales down 1.9% to 2.86 million boed. The impact was more pronounced in exports, which tumbled 10.4% year-over-year to 760,000 bpd. Lower shipments to China and the United States were only partially offset by a pivot toward other Asian markets. The company reported a surge in non-China Asian exports from 10% to 33% of the total mix, highlighted by a new deal with India’s Bharat Petroleum to export up to 6 million barrels annually from 2025. However, the broader decline in exports amid volatile pricing and weak global demand puts pressure on the revenue potential for the quarter, despite strategic realignments. Domestic refined product sales rose 2.9%, aided by demand for diesel and jet fuel, but Brazil’s refined petroleum exports fell over 20% from January to February, while Russian imports surged.

PBR stock is down 12% year to date, underperforming the energy sector. In the same time frame, American supermajors ExxonMobil XOM and Chevron CVX have lost 3% and 6%, respectively.

ExxonMobil and Chevron both reported earnings last Friday. XOM came up with adjusted earnings of $1.76 per share, which beat the Zacks Consensus Estimate of $1.72. ExxonMobil’s better-than-expected quarterly earnings were fueled by higher production from Guyana, Permian and structural cost savings. Meanwhile, Chevron reported adjusted first-quarter earnings per share of $2.18, beating the Zacks Consensus Estimate of $2.15. The outperformance stemmed from higher-than-expected U.S. natural gas production in Chevron’s key upstream segment.

From a valuation standpoint, Petrobras trades at a notable discount compared to Western oil majors. The stock's forward price-to-earnings (P/E) ratio of 4.10 is far lower than ExxonMobil and Chevron, which trade at around 15X earnings. This undervaluation reflects concerns over political risks and government influence.

Petrobras' earnings are deeply tied to oil prices, which are trending lower amid mounting recession fears, especially with rising geopolitical tensions and trade uncertainties. Confidence and economic activity indicators in the United States show a sharp decline, dragging Brent crude prices closer to the $60/barrel support level. If a global slowdown materializes, oil prices could breach this threshold, hurting Petrobras’ top line. Given its high-cost exploration plans and increasing CapEx, a sustained drop in oil prices would pressure margins and impair dividend potential — already under scrutiny — leading to further investor caution around the stock.

Investors should tread carefully with Petrobras as it approaches its Q1 results. Earnings estimates have been revised down 14% in the past month, and revenues are expected to fall nearly 9% year over year. Despite operational discipline, the company saw flat production and weak export volumes. Sales to key markets, such as China and the United States, declined, while increased exports to other Asian countries may not fully offset the shortfall.

The broader picture adds to the unease. Petrobras trades at a steep valuation discount, reflecting persistent political risks. Meanwhile, lower Brent prices—driven by global economic slowdown concerns—could further squeeze margins. With Petrobras’ exposure to volatile markets and no strong signals of an upside earnings surprise, the risk-reward balance looks unfavorable. Selling into potential Q1 weakness seems prudent.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 11 hours |

Stock Market Today: Dow Rises Ahead Of Fed Minutes; Nvidia Jumps On Meta Deal (Live Coverage)

CVX

Investor's Business Daily

|

| 11 hours | |

| 12 hours | |

| Feb-17 |

Warren Buffett's company invests in The New York Times 6 years after he sold all his newspapers

CVX

Associated Press Finance

|

| Feb-17 |

Berkshire Hathaway Takes Stake In New York Times, Cuts Apple, Amazon Holdings

CVX

Investor's Business Daily

|

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite