|

|

|

|

|||||

|

|

|

ASML Holding ASML and Taiwan Semiconductor Manufacturing Company TSM are two titans at the heart of the global semiconductor ecosystem. ASML, a Dutch-based powerhouse, builds the extreme ultraviolet (EUV) lithography systems needed to fabricate the world’s most advanced chips. TSM, based in Taiwan and also known as TSMC, is the largest contract chipmaker globally and ASML’s biggest customer.

Both companies are essential to the production of high-performance computing and artificial intelligence (AI) chips. However, from an investment point of view, one stock offers a more favorable outlook than the other right now.

ASML Holding has a clear advantage in the chip equipment market. It is the only company capable of producing extreme ultraviolet (EUV) lithography machines at scale. These machines are needed to make chips at 5nm, 3nm, and soon 2nm levels — key to powering AI processors, mobile devices and data centers.

The company is already rolling out its next-generation High-NA EUV machines, which will be used for even smaller chips. As demand for faster and more efficient chips rises, especially with the growth of AI, ASML Holding stands to benefit. Its machines are a necessary part of the chip supply chain, and its customers, including TSMC, Intel and Samsung, will rely on ASML’s technology for years to come.

Financially, ASML Holding is performing well. In the first quarter of 2025, it reported revenue growth of 46% and a 93% jump in earnings per share. For the full year, it expects revenues to increase 15%, which shows continued demand, even in a challenging global environment.

However, one concern is the company’s exposure to China. In 2024, China made up 41% of ASML’s shipments. U.S. pressure on the Dutch government has led to export restrictions on some of ASML’s most advanced equipment, which could limit future sales in that market. Still, strong demand from other regions may offset that risk.

TSM manufactures chips for the world’s top tech companies, including NVIDIA, Advanced Micro Devices and Broadcom. Taiwan Semiconductor Manufacturing is known for its advanced production capabilities and has already moved into 3nm production, with 2nm coming soon. Its large scale allows it to handle rising AI chip demand better than most competitors.

In the first quarter of 2025, Taiwan Semiconductor Manufacturing reported a 35% increase in revenues and a 53% jump in profit. Its 3nm and 5nm chips accounted for nearly 58% of wafer sales. AI-related revenues tripled in 2024 and are expected to double again in 2025. With AI likely to be a long-term driver, TSMC’s future growth potential looks strong.

Taiwan Semiconductor Manufacturing is also investing heavily to stay ahead. It plans to spend up to $42 billion in 2025, mostly on advanced manufacturing. This is up from $29.8 billion in 2024 and shows its commitment to keeping its lead in cutting-edge chip production.

However, challenges do linger. Taiwan Semiconductor Manufacturing’s heavy presence in Taiwan leaves it exposed to geopolitical tensions between China and the United States. While the company is building new fabs in the United States, Japan and Europe, these projects are costly and take time. Rising energy prices in Taiwan and weakness in the smartphone and PC markets could also pressure profits in the short term.

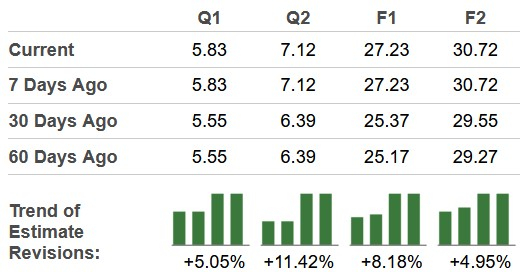

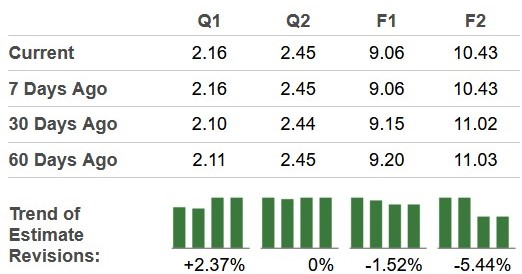

The Zacks Consensus Estimate for ASML Holding’s 2025 sales and EPS implies year-over-year growth of 21.5% and 20.8%, respectively. Importantly, analysts have raised their earnings estimates over the past 30 days, reflecting an improving sentiment.

Taiwan Semiconductor Manufacturing is expected to see faster growth, with revenues projected to rise by 24.6% and earnings by 28.7%. However, earnings estimates have been revised downward recently, suggesting some caution about near-term performance.

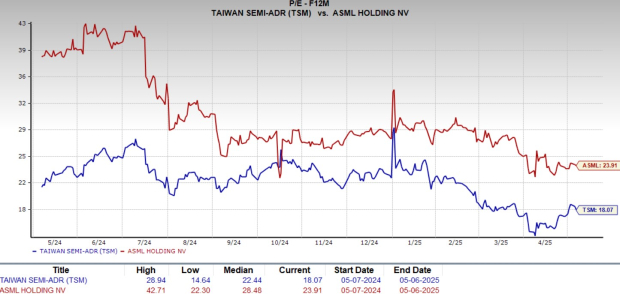

On the valuation front, ASML trades at 23.91 times forward earnings compared to 18.07 times for TSM. While ASML looks more expensive, its positive earnings momentum justifies the premium. TSMC’s lower valuation reflects its risks, including higher capital spending and geopolitical concerns.

Year to date, ASML stock is down about 1.9%, while TSM shares have declined 12.7%. This difference shows how investors are weighing the risks and rewards of each company.

ASML Holding and Taiwan Semiconductor Manufacturing are both critical to the future of semiconductors, but ASML stands out as the more attractive stock at this moment. Its monopoly on EUV technology, consistent demand from top customers and strong earnings growth make it a solid long-term investment.

While TSMC’s growth prospects are impressive, especially in AI chips, the company faces more external risks — from geopolitical tensions to rising costs and supply-chain issues. Its recent downward earnings revisions and heavier capital investments add further uncertainty.

In contrast, ASML Holding offers a strong combination of innovation, financial strength and global relevance. For investors seeking reliable exposure to the backbone of chipmaking, ASML is the smarter buy.

Currently, ASML Holding carries a Zacks Rank #2 (Buy), making the stock a stronger pick than Taiwan Semiconductor Manufacturing, which has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite