|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Dillard’s, Inc. DDS is expected to register year-over-year top and bottom-line declines when it reports first-quarter fiscal 2025 numbers.

The Zacks Consensus Estimate for fiscal first-quarter revenues of $1.54 billion indicates a 0.6% decline from the year-ago reported figure. The consensus estimate for fiscal first-quarter earnings is pegged at $9.10 per share, implying a 17.9% decrease from the year-ago quarter’s reported figure. The consensus estimate has been unchanged in the past 30 days.

In the last reported quarter, the company registered an earnings surprise of 39.5%. We note that in the trailing four quarters, its bottom line beat the Zacks Consensus Estimate by 14.1%, on average. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

Dillard's, Inc. price-eps-surprise | Dillard's, Inc. Quote

Our proven model does not conclusively predict an earnings beat for Dillard’s this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Dillard’s currently has an Earnings ESP of 0.00% and a Zacks Rank #3.

Dillard’s has been witnessing the adverse impacts of a tough retail environment due to the cautious buying behavior of consumers for a while now. This has continued to impact its sales and comparable-store sales (comps), and has led to higher operating expenses. The persistence of these trends is expected to have affected the top and bottom lines in the to-be-reported quarter.

Our model predicts a comps decline of 1.1% for the fiscal first quarter due to a challenging retail environment. Retail sales are expected to dip 1.3% year over year in the fiscal first quarter.

Additionally, higher payroll and payroll-related expenses are likely to have dented margins and the bottom line in the fiscal first quarter.

While we expect SG&A expenses to increase 2% for the first quarter of fiscal 2025, the SG&A expense rate is anticipated to expand 90 basis points to 28%. Our model predicts an 18% year-over-year decline in operating profit, with a 260-bps contraction in the operating margin.

However, Dillard's has been gaining from better inventory management initiatives and strong consumer demand. The company’s focus on inventory management, store and e-commerce development and offering trendy merchandise has strengthened its position in the competitive retail landscape.

The company’s efforts to capture growth opportunities in brick-and-mortar stores and e-commerce have been key drivers. It has been focused on enhancing brand relationships, remodeling stores and optimizing its activewear segment. Gains from these initiatives are likely to have widened the customer base and boosted the company's overall sales in the fiscal first quarter.

On the storefront, DDS has been gaining from initiatives to enhance brand relations, focus on in-trend categories, store remodels and increased rewards to store personnel. Its activewear brands are expected to have gained market share in the to-be-reported quarter.

Also, the e-commerce business has been well-placed on the enhancement of merchandise assortments and effective inventory management. We expect the company’s fiscal first-quarter performance to have been driven by its focus on increasing productivity at existing stores, improving the omnichannel platform and enhancing domestic operations.

From a valuation perspective, Dillard’s is trading at a premium relative to industry and historical benchmarks. The company has a forward 12-month price-to-sales ratio of 0.87X, higher than the Retail - Regional Department Stores industry’s average of 0.28X. The company is trading below the five-year high of 1.24X, reflecting the potential for further upside.

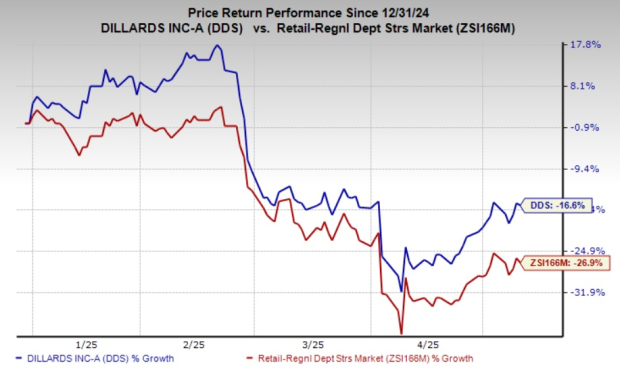

The recent market movements show that DDS shares have lost 16.6% in the year-to-date period compared with the industry's 26.9% decline.

Here are some companies that you may want to consider, as our model shows that these have the right combination of elements to post an earnings beat this time around.

Home Depot HD has an Earnings ESP of +0.43% and a Zacks Rank #3 at present. HD is likely to register top-line growth when it reports first-quarter fiscal 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $39.3 billion, indicating 8% growth from the figure reported in the prior-year quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Home Depot’s fiscal first-quarter earnings is pegged at $3.59 per share, indicating a 1.1% decline from the year-ago quarter’s actual. The consensus mark has been unchanged in the past 30 days.

Ross Stores ROST presently has an Earnings ESP of +1.27% and a Zacks Rank #3. ROST is likely to register top-line growth when it reports first-quarter fiscal 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $5 billion, implying a 2.3% rise from the figure reported in the prior-year quarter.

The Zacks Consensus Estimate for ROST’s fiscal first-quarter earnings is pegged at $1.43 per share, implying a year-over-year decline of 2.1%. The consensus mark for earnings has moved up by a penny in the past seven days.

Urban Outfitters URBN currently has an Earnings ESP of +1.03% and a Zacks Rank of 3. The company is likely to register top and bottom-line growth when it reports first-quarter fiscal 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $1.29 billion, suggesting a 7.1% jump from the figure reported in the prior-year quarter.

The Zacks Consensus Estimate for Urban Outfitters’ earnings is pegged at 81 cents per share, indicating a 17.4% rally from the year-ago quarter’s actual. The consensus mark has been unchanged in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 4 hours | |

| 6 hours | |

| 10 hours | |

| 12 hours | |

| 14 hours | |

| Feb-21 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite