|

|

|

|

|||||

|

|

|

Shares of Bank of America BAC, one of the most interest rate-sensitive among big banks, gained 18.2% in the past month, outperforming the S&P 500 Index. Meanwhile, its close peers – JPMorgan JPM and Citigroup C – rallied 10.8% and 18.5%, respectively.

BAC One-Month Price Performance

The U.S. stock market experienced notable volatility over the past month, largely due to developments in trade policy and monetary decisions from the Federal Reserve. Early in the period, investor sentiment soured amid escalating trade tensions with China, pushing the Nasdaq into bear market territory. However, a temporary tariff truce between the United States and China sparked a sharp rebound in equities. Yesterday, the Dow Jones, S&P 500 and Nasdaq all recorded their biggest single-day gains in over a month, marking a strong recovery in response to easing trade concerns.

In such an uncertain operating environment, let’s try to decipher how BAC stock is expected to perform.

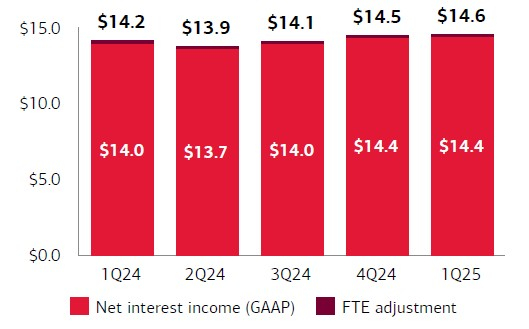

Path for Interest Rate: When the Federal Reserve lowered the interest rates by 100 basis points last year, the company’s net interest income (NII) benefited from it. Fixed-rate asset repricing, higher loan balance and a gradual decline in deposit costs drove the sequential increase in NII since the second quarter of 2024, which was partly offset by lower interest rates.

Bank of America’s Net Interest Income (FTE, $B)

At the May 6-7 FOMC meeting, the central bank kept the interest rates unchanged at 4.25-4.5% . Further, the Fed Chair Jerome Powell noted that there is no “need to be in a hurry” to make any monetary policy change until there is clarity on the impact of Trump's tariffs on employment and inflation. As such, interest rates are likely to stay higher for a longer time.

Bank of America is seeing an upside in NII in 2025, driven by decent loan demand, higher-for-longer interest rates and robust deposit balance. The company expects a sequential rise in NII for all quarters this year, with growth likely to accelerate in the second half of the year and the fourth-quarter number likely to touch the $15.5-$15.7 billion level. Hence, for 2025, NII is expected to rise 6-7%.

Branch Expansion & Digital Initiatives: Bank of America’s aggressive branch expansion across the United States as part of a broader strategy to solidify customer relationships and tap into new markets will drive NII growth over time. The company announced plans to open more than 165 new financial centers by 2026. This new wave of expansion follows the branch network growth plans announced by Bank of America in June 2023. The plan focused on entering nine new markets, including Omaha, Boise and Milwaukee.

The bank's strategic investment in new financial centers and expansion into new markets reflects a broader industry shift toward optimizing branch networks to deepen customer relationships and tap into new business opportunities. In this competitive environment, the ability to blend digital convenience with in-person expertise is expected to give Bank of America long-term leverage in the evolving banking landscape.

The company plans to continue strengthening its technology initiatives and spend heavily on these. These efforts help it attract and retain customers and boost cross-selling opportunities.

Digital Adoption

Fortress Balance Sheet & Solid Liquidity: Bank of America’s liquidity profile remains solid. As of March 31, 2025, average global liquidity sources were $942 billion. Also, the company’s investment-grade long-term credit ratings of A1, A- and AA- from Moody’s, S&P Global Ratings and Fitch Ratings, respectively, and a stable outlook facilitate easy access to the debt market.

BAC continues to reward shareholders handsomely. After it cleared the 2024 stress test, the company increased its quarterly dividend by 8% to 26 cents per share. In the last five years, it hiked dividends four times, with an annualized growth rate of 8.84%. Currently, the company's payout ratio is 31% of earnings.

In July 2024, the company authorized a $25 billion stock repurchase program, effective Aug. 1, 2024. As of March 31, 2025, almost $14.4 billion worth of buyback authorization remained available. The company intends to buy back shares worth almost $4.5 billion every quarter in the near term.

Weak Investment Banking (IB) Business: As global deal-making came to a grinding halt at the beginning of 2022, it weighed substantially on Bank of America’s IB business. Though the company’s total IB fees plunged 45.7% in 2022 and 2.4% in 2023, the trend reversed in 2024. Thus, the company’s IB fees soared 31.4% year over year.

However, the anticipated resurgence in mergers and acquisitions (M&As) following President Donald Trump’s re-election and expectations of favorable regulatory changes failed to materialize. Nonetheless, the first-quarter 2025 performance was better than expected (IB fees in the Global Banking division of $847 million were relatively stable as the plunge in equity underwriting income was almost offset by the improvement in advisory revenues and higher debt underwriting income).

However, deal-making activities have paused as ambiguity over the tariff and ensuing trade war has resulted in extreme market volatility and economic uncertainty. Amid such a backdrop, companies are rethinking their M&A plans despite stabilizing rates and having significant investible capital. Hence, in the near term, this will significantly hurt the IB businesses of Bank of America, JPMorgan and Citigroup, which generate billions in revenues from M&A advisory fees.

Nonetheless, as the operating backdrop gradually turns favorable for deal-making activities, global M&As are expected to witness a solid rise. Eventually, Bank of America will report growth in IB fees, driven by a healthy IB pipeline and an active M&A market.

Deteriorating Asset Quality: Bank of America’s asset quality has been weakening. While the company recorded negative provisions in 2021, a substantial jump in provisions was recorded in the years that followed because of the worsening macroeconomic outlook. The metric surged 115.4% in 2022, 72.8% in 2023 and 32.5% in 2024. Similarly, net charge-offs grew 74.9% in 2023 and 58.8% in 2024. The uptrend for both continued in the first quarter of 2025.

As interest rates are less likely to come down substantially in the near term, it is expected to hurt the borrowers’ credit profile. The company remains vigilant about the effects of continuous high rates and quantitative tightening on its loan portfolio. Also, the impact of tariffs on inflation is to be seen. Hence, the company’s asset quality is likely to remain subdued.

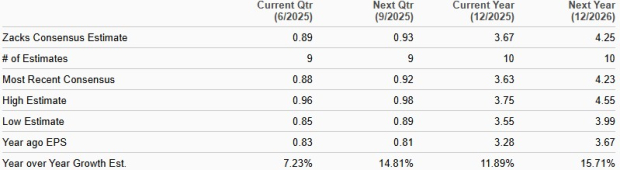

Over the past month, the Zacks Consensus Estimate for earnings for 2025 has moved marginally higher to $3.67. On the other hand, the consensus estimate for 2026 earnings moved modestly lower to $4.25. The consensus estimate for earnings indicates an 11.9% and 15.7% growth for 2025 and 2026, respectively.

Bank of America Earnings Estimates

Bank of America stock is currently trading at a 12-month trailing price-to-tangible book (P/TB) of 1.64X, which is below the industry’s 2.61X. This shows the stock is inexpensive.

Price-to-Tangible Book Ratio (TTM)

BAC stock is inexpensive compared with JPMorgan, which has a P/TB of 2.75X. On the other hand, it is trading at a premium compared with Citigroup’s P/TB of 0.84X.

Bank of America's global presence, diversified revenue streams, ongoing branch openings and high interest rates for long term and technological innovations aimed at attracting and retaining customers provide a strong foundation for organic growth. Further, bullish analyst sentiments and attractive valuation make the stock a compelling option for investors.

However, BAC faces near-term challenges, such as increased regulatory capital requirements under the Basel III framework and macroeconomic uncertainty because of the imposition of tariffs and its impact on interest rate cuts. Additionally, weak business performance in the IB sector and deteriorating asset quality are near-term concerns. So, investors must wait for clarity on macroeconomic issues before buying the stock.

Those who already own Bank of America stock can retain it for solid long-term gains. At present, Bank of America carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| 6 hours | |

| 10 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite