|

|

|

|

|||||

|

|

|

Nebius Group N.V. NBIS will report its first-quarter 2025 results on May 20, before market open.

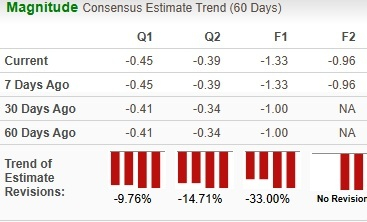

The Zacks Consensus Estimate for the bottom line in the to-be-reported quarter is pegged at a loss of 45 cents. The estimate has remained unchanged in the past seven days but has been revised downward by 4 cents in the past 60 days. The consensus estimate for total revenues is pinned at $63.8 million.

Based in Amsterdam, Nebius is positioning itself as a specialized AI infrastructure company. Its core operation is Nebius, which is an AI-powered cloud platform designed for intensive AI and ML workloads in both owned and colocation data center capacity. It resumed trading as a public company in October 2024.

Our proven model does not conclusively predict an earnings beat for NBIS this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. But that is not the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

NBIS has an Earnings ESP of -7.87% and a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Nebius Group N.V. price-eps-surprise | Nebius Group N.V. Quote

Nebius is focused on boosting its data center footprint and its GPU deployments as part of its strategy to ramp up installed capacity across the United States and Europe. Establishing facilities in the United States means lower latency while serving domestic clients and boosting the advantages of the AI-native cloud. In March 2025, NBIS also announced the setting up of a new data center in New Jersey. This data center will boast a total capacity of 300 MW, and the first phase is expected to be completed by the summer of 2025. The same day, it also announced incremental capacity additions at its existing colocation facility in Kansas City. The additional capacity is expected to come online by the end of the second quarter of 2025. As it expands AI infrastructure in Europe, NBIS also announced a new colocation deployment in Keflavik, Iceland.

It is focusing on establishing more GPU clusters across the United States amid soaring demand for high-quality AI infrastructure. NBIS is also focused on strengthening its global sales and marketing efforts with a specific focus on the US market. These factors are likely to have aided the top-line performance. In the last reported quarter, NBIS unveiled its new AI cloud platform and migrated all its customers onto it. The company also introduced an Inference-as-a-Service platform called AI Studio. Given these factors, along with contracts in place, NBIS expects its March run rate revenue to be at least $220 million.

Apart from its core cloud platform, other notable offerings by Nebius include Toloka, an AI development platform; TripleTen, an edtech service; and Avride, an autonomous vehicle platform. Contract wins for its Avride autonomous technology platform business augur well. Efforts to diversify the client base for its Toloka platform and transition to a new platform, which is tuned for complex GenAI tasks, are likely to have aided in driving revenues from this business. Revenues for the full year 2024 grew 140% for Toloka.

Nonetheless, a challenging global macroeconomic environment and increasing lead times as customers become more selective are expected to weigh on the top-line expansion. NBIS is investing significantly in expanding capacity, which is expected to keep margins under pressure, at least in the near term.

Nebius is a relatively new entrant in the AI cloud infrastructure space, which boasts behemoths like Amazon AMZN, Microsoft MSFT and Alphabet GOOGL. These behemoths already have a global-scale AI cloud, whereas NBIS is still expanding its infrastructure. Amazon Web Services and Microsoft’s Azure cloud platform together dominate more than half of the cloud infrastructure services market.

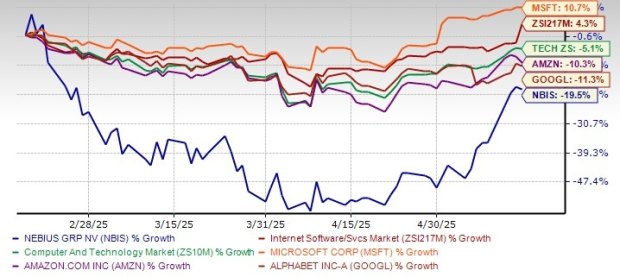

Nebius shares have lost 19.5% over the past three months, underscoring broader and company-specific challenges. The stock has also underperformed the Zacks Computer & Technology sector decline of 5.1% and the Zacks Internet Software Services industry’s gain of 4.3%.

The company has underperformed its peers like Microsoft, Alphabet and Amazon. Alphabet and Amazon shares have plunged 11.3% and 10.3%, respectively, in the same time frame, while Microsoft has gained 10.7%.

In terms of Price/Book, NBIS shares are trading at 2.59X, lower than the Internet Software Services industry’s ratio of 4.12, but it could mean more risk than opportunity.

Given Nebius' ongoing investments in its core AI infrastructure platform and promising growth in Toloka and Avride platforms, long-term potential remains. However, significant margin pressure owing to ongoing investments and fierce competition from behemoths clouds the outlook. The negative Earnings ESP and muted stock performance further temper expectations. Retaining NBIS stock ahead of earnings appears prudent, but cautious optimism is warranted.

With strong demand tailwinds in the AI space, it is an exciting growth story, but one with competitive pressures that investors must closely monitor.

NBIS currently carries a Zacks Rank #3 (Hold), which indicates that investors should wait for a better entry point. However, existing investors can hold the stock as its growth prospects remain intact.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 14 hours | |

| 15 hours | |

| 17 hours | |

| 20 hours | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite