|

|

|

|

|||||

|

|

|

Merck MRK and Pfizer PFE are leading pharmaceutical companies with strong product and pipeline portfolios in oncology. Both companies also have presences in vaccines, neuroscience, and immunology.

However. oncology accounts for more than 50% of Merck’s total revenues. Blockbuster PD-L1 inhibitor, Keytruda, approved for several types of cancers, alone accounts for around 50% of its pharmaceutical sales.

As regards Pfizer, oncology sales comprise around 25% of its total revenues. Its position in oncology was strengthened with the acquisition of Seagen in 2023.

Both companies are seeing consistent sales and earnings growth. Both boast robust pipelines with promising candidates in late-stage development. But which one is a better investment today? Let’s take a closer look at their fundamentals, growth prospects and challenges to make an informed choice.

Pfizer is one of the largest and most successful drugmakers in oncology. After witnessing possibly its worst slowdown in 2023/early 2024, the company seems to be gradually making a comeback and entering a transition phase. With its COVID-related uncertainties diminishing, its revenue volatility is declining.

Though COVID revenues are declining, Pfizer’s non-COVID operational revenues improved in 2024, driven by its key in-line products like Vyndaqel, Padcev and Eliquis, new launches and newly acquired products like Nurtec and those from Seagen. The positive trend continued in the first quarter of 2025.

The continued growth of Pfizer’s diversified portfolio of drugs, particularly oncology, should support top-line growth in 2025.

Pfizer expects cost cuts and internal restructuring to deliver savings of $7.7 billion by the end of 2027. Pfizer’s significant cost-reduction and efforts to improve R&D productivity measures should drive profit growth.

Pfizer faces its share of challenges, the key being declining sales of its COVID-19 products. Pfizer also expects a significant impact from the loss of patent exclusivity in the 2026-2030 period, as several of its key products, including Eliquis, Vyndaqel, Ibrance, Xeljanz and Xtandi, will face patent expirations. The Medicare Part D redesign is also expected to hurt sales of Pfizer’s higher-priced drugs like Vyndaqel, Ibrance and Xeljanz in 2025.

The company has also faced its share of setbacks. Last month, Pfizer said it is discontinuing the development of its GLP-1R agonist, danuglipron, which was being developed as a weight loss pill. Pfizer took the decision after one of the participants in the dose-optimization studies developed a potentially drug-induced liver injury, which resolved after danuglipron was discontinued. Eli Lilly LLY and Novo Nordisk NVO currently dominate the obesity space.

Also, uncertainties around tariffs and a volatile macro environment remain headwinds. Moreover, stocks of vaccine makers like Pfizer have been under pressure with the appointment of Robert F. Kennedy Jr., a well-known vaccine skeptic, as the Secretary of Health and Human Services (HHS).

As of March 31, 2025, Pfizer had cash and cash equivalents of $17.3 billion on its balance sheet and $57.6 billion in long-term debt. Its debt-to-capital ratio of 0.41 is slightly higher than the industry's average of 0.38.

Merck boasts more than six blockbuster drugs in its portfolio, with Keytruda being the key top-line driver. Keytruda has played an instrumental role in driving Merck’s steady revenue growth in the past few years. Keytruda’s sales are gaining from rapid uptake across earlier-stage indications, mainly early-stage non-small cell lung cancer. Continued strong momentum in metastatic indications is also boosting sales growth. The company expects continued growth from Keytruda, particularly in early lung cancer. Merck is also developing a subcutaneous formulation of Keytruda that can extend its patent life. Merck is working on different strategies to drive Keytruda's long-term growth.

Merck has been making meaningful regulatory and clinical progress across areas like oncology (mainly Keytruda), vaccines and infectious diseases while executing strategic business moves. Merck’s phase III pipeline has almost tripled since 2021, supported by in-house pipeline progress as well as the addition of candidates through M&A deals.

Merck’s new products, Capvaxive and Winrevair, are witnessing strong launches and have the potential to generate significant revenues over the long term

However, sales of Gardasil, which is Merck’s second-largest product, are declining due to a weak performance in China, which resulted from sluggish demand trends amid an economic slowdown. Merck is also seeing weakness in the diabetes franchise and the generic erosion of some drugs.

Merck is heavily reliant on Keytruda. Though Keytruda may be Merck’s biggest strength and a solid reason to own the stock, it can also be argued that the company is excessively dependent on the drug and it should look for ways to diversify its product lineup.

There are rising concerns about the firm’s ability to grow its non-oncology business ahead of the upcoming loss of exclusivity of Keytruda in 2028.

Also, competitive pressure might increase for Keytruda in the near future.

It exited 2024 with cash and cash equivalents of $9.2 billion against long-term debt of $33.5 billion, resulting in a debt-to-capital ratio of 0.41, which is higher than the industry's average of 0.38.

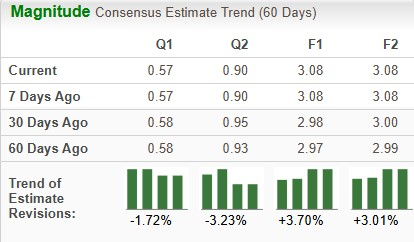

The Zacks Consensus Estimate for PFE’s 2025 sales implies a year-over-year decrease of 0.6% and 1%, respectively. EPS estimates for both 2025 and 2026 have risen over the past 60 days.

The Zacks Consensus Estimate for MRK’s 2025 sales and EPS implies a year-over-year increase of 0.9% and 16.7%, respectively. EPS estimates for both 2025 and 2026 have declined over the past 60 days.

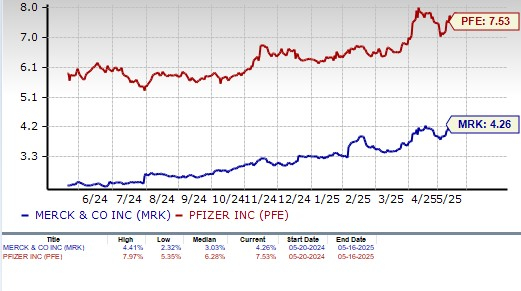

Year to date, Pfizer’s stock has declined 10.8% and Merck’s stock has plunged 22.9% compared with the industry’s decrease of 4.0%

Both MRK and PFE are priced lower than the industry from a valuation standpoint. MRK is more expensive than PFE, going by the price/earnings ratio. Merck’s shares currently trade at 8.24 forward earnings, higher than 7.41 for Pfizer.

However, both Merck and Pfizer are cheaper than other large drugmakers like AbbVie, AstraZeneca, Eli Lilly and Novo Nordisk.

Pfizer’s dividend yield of 7.5% is higher than MRK’s 4.3%.

Pfizer’s return on equity of 20.3% is lower than Merck’s 43.2%

The potential impact of tariffs imposed by the United States and some other countries is a concern. Although both Pfizer and Merck’s 2025 earnings guidance accounts for the impact of tariffs already in place, the potential expansion of tariffs in other geographies or increases in retaliatory tariffs would have a negative impact. Though pharmaceuticals have been exempted from tariffs this time around, they could well be Trump’s target in the next round, considering the President’s goal to shift pharmaceutical production back to the United States, mostly from European and Asian countries.

However, both Pfizer and Merck said on their respective first-quarter conference calls that if the import tariffs are implemented on pharmaceutical products, they are well placed to manage the impact.

Trump and the Republican government also continue to stress on the control of drug prices with the latest attempt being his “most favored nations’ policy.”

Merck has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Merck has one of the world’s best-selling drugs in its portfolio, generating billions of dollars in revenues. Though Keytruda will lose patent exclusivity in 2028, its sales are expected to remain strong until then. However, the company’s problems are too many at present, including persistent challenges for Gardasil in China, potential competition for Keytruda and rising competitive and generic pressure on some drugs. All these factors have raised doubts about Merck’s ability to navigate the Keytruda loss of exclusivity period successfully. Consistently declining estimates also reflect analysts’ pessimistic outlook for the stock.

Pfizer, on the other hand, with its improving growth prospects, rising estimates, cheaper valuation, and higher dividend yield, is a better bargain for investors looking to invest in drug/biotech stocks with higher growth potential. Pfizer, with a Zacks Rank #2 (Buy), is a clear-cut winner.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 |

How Novo Nordisk Is Striking Back As Eli Lilly Plans Its Newest Weight-Loss Launch

LLY

Investor's Business Daily

|

| Apr-02 | |

| Apr-02 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite