|

|

|

|

|||||

|

|

|

Diageo plc DEO reported net sales data for third-quarter fiscal 2025 and issued other updates. On a reported basis, net sales of $4.4 billion jumped 2.9% year over year, due to organic growth, partly offset by foreign exchange headwinds and disposals. The Zacks Consensus Estimate is currently pegged at $4.1 billion.

Organic net sales climbed 5.9% year over year, with robust organic volumes increasing 2.8% and favorable price/mix of 3.1%. Significant phasing gains are likely to have contributed almost 4% to organic net sales growth. Organic net sales jumped 6% in North America, 2% in Asia Pacific, 29% in Latin America and the Caribbean and 10% in Africa, while the metric remained broadly flat in Europe.

All regions saw positive price/mix except Asia Pacific, where persistent consumer downtrading and negative market mix hurt sales. Management expects the majority of this phasing benefit to unwind in the fourth quarter.

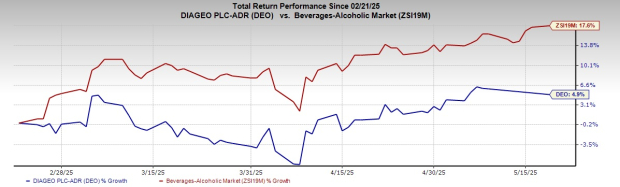

This Zacks Rank #3 (Hold) company’s shares have gained 4.9% in the past three months compared with the industry’s 17.6% growth.

Assuming the present 10% tariff on both U.K. and European imports into the US, Mexican and Canadian spirits imports into the US are exempt under USMCA, with no other changes to tariffs. The unmitigated effect of such tariffs is estimated to be C$150 million annually.

Tariffs between the US and China do not hurt the company’s business materially. Considering the actions, before any pricing, management looks to mitigate almost half of this effect on operating profit on an ongoing basis. Moving forward, management looks to continue taking measures to neutralize this impact further. The anticipated impact in fiscal 2025 and fiscal 2026 is included in the company’s guidance.

In addition, Diageo has introduced the first phase of its Accelerate program, which defines clear cash delivery goals as well as a controlled approach to operational excellence and cost efficiency. This program focuses on how the company does business, shifting to a more agile global operating model and robust digital and data capabilities. This simplified approach looks to develop a solid platform to optimize investment and allocate resources toward long-term growth.

It forecasts to sustainably deliver C$3 billion free cash flow per year from fiscal 2026, which will be higher as performance improves. This is buoyed by C$500 million cost savings over the three years, hence enabling reinvestment in future growth and higher operating leverage. The company expects to return to its target leverage ratio range of 2.5-3x net debt/EBITDA no later than fiscal 2028, hence offering higher flexibility.

Solid organic growth and leveraged operating costs, coupled with robust capital discipline and appropriate disposals in the coming years, will help DEO in achieving such targets.

Diageo sees the near-term industry pressures to be highly macroeconomic-driven, with uncertainty hurting the timing and pace of recovery. Management reiterated organic net sales and operating profit views for fiscal 2025. In the second half of fiscal 2025, DEO continues to anticipate a sequential improvement in organic net sales growth compared with the first half. It still expects a slight drop in organic operating profit for the second half compared with the prior year, broadly in line with the decrease in the first half. This reflects the tariff impacts on results in fiscal 2025.

From and including results for fiscal 2025, Diageo is changing how it reports the effective tax rate, for both pre and post-exceptional items. It will also exclude the share of after-tax results of associates and joint ventures from profit before tax. Considering the new basis, DEO predicts the tax rate before exceptional items for fiscal 2025 to be approximately 25%, broadly in line with 25.1% seen in fiscal 2024.

Taking the present market conditions and DEO’s debt maturity profile, the effective interest rate for fiscal 2025 is likely to be slightly below 4.3% seen in fiscal 2024. It expects capital expenditure toward the upper end of its earlier-guided range of $1.3-$1.5 billion.

Nomad Foods NOMD, which manufactures frozen foods, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

NOMD delivered a trailing four-quarter earnings surprise of 3.2%, on average. The Zacks Consensus Estimate for Nomad Foods’ current financial-year earnings per share (EPS) indicates growth of 7% from the year-ago number.

United Natural Foods UNFI, which is a distributor of natural, organic and specialty food in the United States, currently carries a Zacks Rank #2 (Buy).

UNFI delivered a trailing four-quarter earnings surprise of 408.7%, on average. The Zacks Consensus Estimate for UNFI’s current financial-year sales and EPS indicates growth of 1.9% and 488.6%, respectively, from the year-ago numbers.

Utz Brands UTZ manufactures salty snacks under popular brands and has a Zacks Rank of 2 at present. UTZ delivered a trailing four-quarter average earnings surprise of 6.9%.

The Zacks Consensus Estimate for UTZ’s current financial-year sales and EPS implies growth of 1.4% and 10.7%, respectively, from the year-ago numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite