|

|

|

|

|||||

|

|

|

National Vision has been on fire lately. In the past six months alone, the company’s stock price has rocketed 59.1%, reaching $18.55 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in National Vision, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re happy investors have made money, but we're cautious about National Vision. Here are three reasons why EYE doesn't excite us and a stock we'd rather own.

A retailer’s store count often determines how much revenue it can generate.

National Vision operated 1,237 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 3.8% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

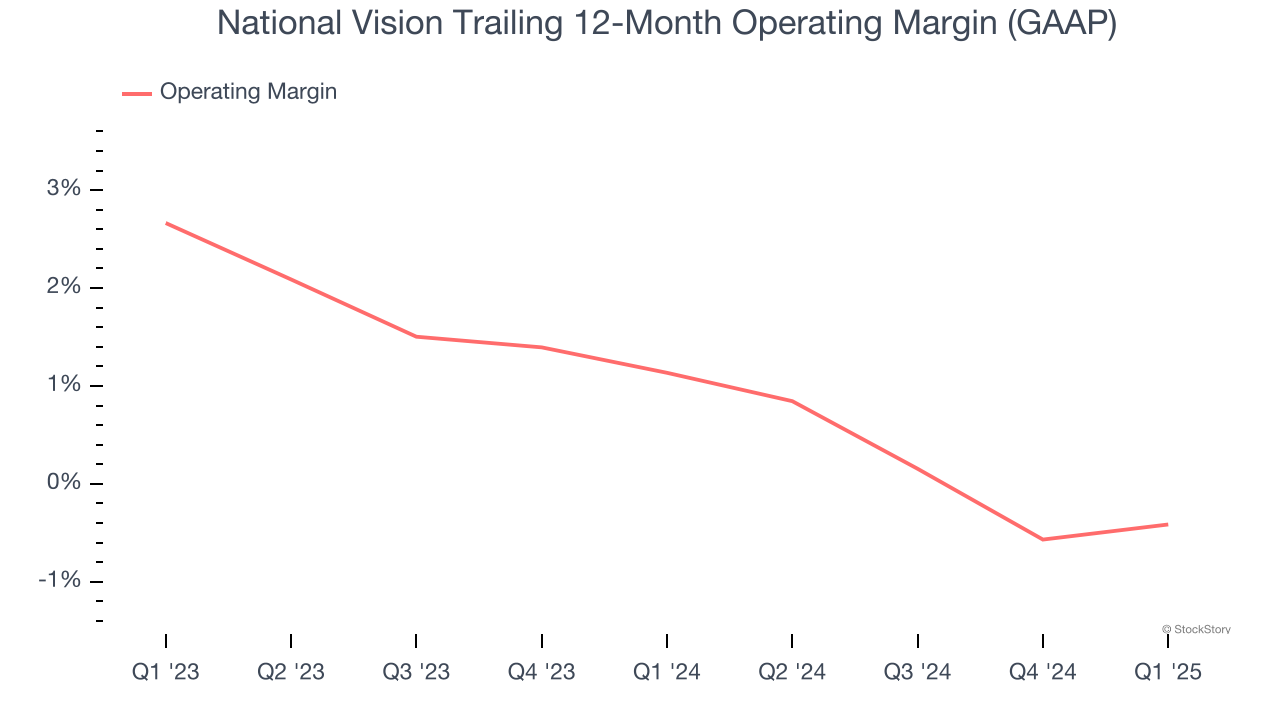

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

National Vision was roughly breakeven when averaging the last two years of quarterly operating profits, inadequate for a consumer retail business. This result is surprising given its high gross margin as a starting point.

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

National Vision historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

We cheer for all companies serving everyday consumers, but in the case of National Vision, we’ll be cheering from the sidelines. Following the recent surge, the stock trades at 30.9× forward P/E (or $18.55 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Mar-24 | |

| Mar-23 | |

| Mar-17 | |

| Mar-12 | |

| Mar-12 | |

| Mar-10 | |

| Mar-10 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite