|

|

|

|

|||||

|

|

|

SAP SE SAP stock has proven resilient with a year-to-date (“YTD”) gain of 21.2%, outperforming the Computer-Software industry and the S&P 500 composite’s growth of 6.4% and 0.3%, respectively. Pivot to the cloud has been the driving force behind SAP stock’s good run.

Closing at $298.41 as of yesterday’s trading session, SAP stock is currently hovering near its 52-week high of $303.40.

With substantial gains YTD, the question is whether investors should still remain invested in SAP stock or book profits and exit. Let us address this question by evaluating the company’s pros and cons.

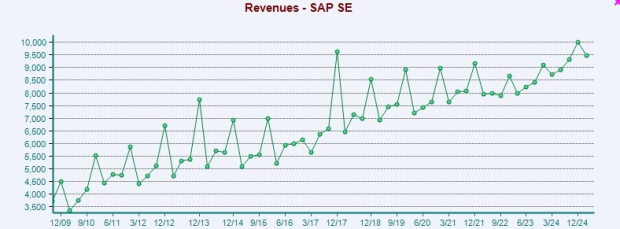

Continued momentum in the cloud business is driving SAP's top-line growth. Current cloud backlog, a key indicator of go-to-market success in the cloud business, surged 28% (up 29% at cc) to €18.2 billion in the first quarter. Cloud revenues surged 27% year over year to €4.99 billion (up 26% at cc) on a non-IFRS basis, powered by solid 34% growth (up 33% at cc) in Cloud ERP Suite revenues, reaching €4.25 billion. The suite accounted for 85% of total cloud revenues, highlighting its rising significance as a core driver of the company’s overall cloud growth. The continued strength in Rise with SAP and Grow with SAP solutions is also noteworthy.

At present, 86% of SAP’s total revenues are now categorized as predictable, a vital quality for long-term earnings visibility and stability.

This robust cloud performance, along with growing focus on data and Business AI, is poised to play a pivotal role in driving revenue growth through 2027. A major innovation in SAP’s cloud strategy is the launch of SAP Business Data Cloud, designed to harmonize all enterprise data (SAP and non-SAP, structured and unstructured) under a single semantic layer. It also boasts integration with platforms like Databricks. SAP signed 20 Business Data Cloud deals in the first quarter.

Recently, SAP teamed up with Accenture to introduce ADVANCE, a state-of-the-art offering developed jointly to help companies with annual revenues of up to $5 billion rapidly transition to the cloud. Designed as a purpose-built suite of solutions, ADVANCE empowers high-growth organizations to become more connected by leveraging preconfigured, ready-to-consume packages. These solutions are tailored by industry and function, allowing businesses to move at speed, implementing cloud transformations in as little as six to 12 months.

The company is also working on flexible licensing options that let customers seamlessly upgrade and transition to its latest cloud solutions across the entire SAP business suite, eliminating the burden of extra negotiations.

Despite global uncertainty, SAP has reaffirmed the growth outlook and remains confident in its trajectory. For the year, management continues to anticipate cloud revenues in the range of €21.6-€21.9 billion, indicating an increase of 26-28% at cc on a year-over-year basis from €17.14 billion. Cloud and software revenues are expected in the band of €33.1-€33.6 billion, with an increase of 11-13% at cc on a year-over-year basis from €29.83 billion.

SAP remains optimistic about the generative-AI trend and expects it to positively impact revenues going forward. Management highlighted that it has incorporated more than 1,300 skills into AI co-pilot, which can now automate 80% of the most-used activities by users.

In 2025, SAP is strengthening its commitment to AI with heavy investments. More than 30,000 developers will focus on improving SAP’s AI foundation and building new use cases.

Declining software license and service revenues owing to a shift to cloud remain a concern. In the first quarter, software licenses revenues declined 10% year over year (both at normal and cc) to €0.18 billion. Services business posted revenues of €1.07 billion, falling 1% year over year (down 2% at cc).

A volatile macroeconomic backdrop, along with increasing costs and stiff competition in the cloud space, is an additional headwind.

SAP has solid growth opportunity driven by demand for its solutions in the cloud space. Generative AI is emerging as another revenue driver.

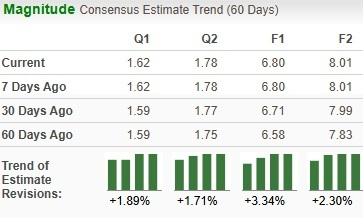

In the past 60 days, analysts have increased their earnings estimates for the current and the next quarter by 1.9% and 1.7%, respectively. The same for the current and the next year is revised upward by 3.3% and 2.3%, respectively.

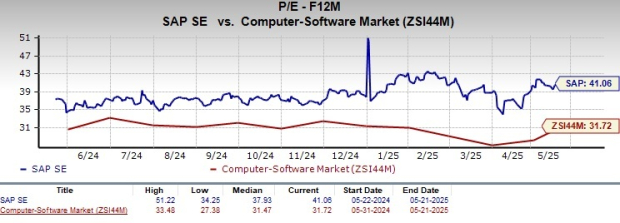

However, a volatile macroeconomic backdrop, along with increasing costs, stiff competition and expensive valuation warrants caution. SAP is trading at a premium with a forward 12-month price/earnings ratio of 41.06X compared with the industry’s 31.72X.

At present, SAP carries a Zacks Rank #3 (Hold). Consequently, it might not be wise to bet on the stock at the moment, but long-term investors already owning it can stay put.

Some better-ranked stocks from the broader technology space are Blackbaud Inc. BLKB, CommVault Systems. CVLT and Pegasystems PEGA. BLKB currently sports a Zacks Rank #1 (Strong Buy), whereas CVLT and PEGA carry a Zacks Rank #2 (Buy) each. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for BLKB’s 2025 EPS is pegged at $4.23, unchanged in the past seven days. BLKB’s earnings beat the Zacks Consensus Estimate in two of the trailing four quarters, while missing and reporting in line on the remaining two occasions, with the average surprise being 1.2%. The stock has declined 21.6% in the past year.

The Zacks Consensus Estimate for CVLT’s fiscal 2026 earnings is pegged at $4.11, unchanged in the past seven days. CVLT’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 10.7%. Its shares have risen 57.7% in the past year.

The Zacks Consensus Estimate for PEGA’s fiscal 2025 EPS is pegged at $3.26, unchanged in the past seven days. PEGA’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 94.1%. The stock has risen 64.2% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| May-13 | |

| May-13 | |

| May-13 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-11 | |

| May-11 | |

| May-08 | |

| May-05 | |

| May-05 | |

| May-04 | |

| May-04 | |

| May-04 | |

| May-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite