|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Visa Inc. V, a global leader in payment processing, continues to impress with strong financials, rising cross-border volumes, and the growing adoption of digital payments. Resilient consumer spending, across both discretionary and essential categories, alongside increased demand for Visa’s value-added services, is helping fuel its momentum.

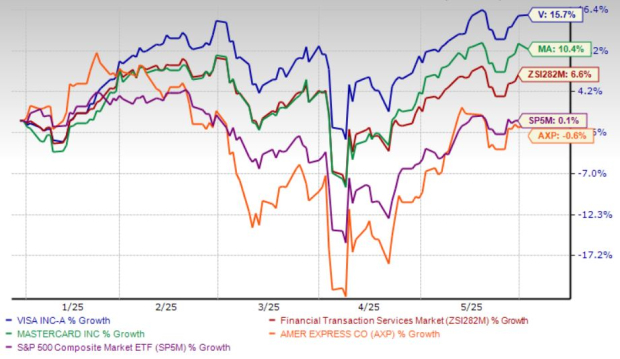

So far in 2025, Visa’s stock is up 15.7%, outperforming the broader industry, the S&P 500, and key rivals like Mastercard Incorporated MA and American Express Company AXP.

As macroeconomic uncertainty looms and questions arise over the durability of certain fintech business models, Visa continues to showcase the strength of its robust network. With pricing power, stable revenue growth, strong cash flows, and high profitability, its fundamentals remain solid. Let’s dive into the key drivers and assess whether Visa still has room to run, or if a pullback is due.

Visa is benefiting from steady spending trends among affluent consumers, modest gains in retail, and stable demand in sectors like travel and dining. In fiscal 2024, processed transactions rose 10%, followed by another 10.2% gain in the first half of fiscal 2025. Payments volume climbed 6.7% in fiscal 2024 and 6.3% in 1H FY25, continuing to be a major revenue driver.

Emerging markets, where a large portion of the population remains underbanked, present further expansion opportunities. In the first half of fiscal 2025, payments volume grew 6.1% year over year in Latin America and 14.2% in CEMEA. However, the same witnessed a 1.2% decline in Asia Pacific during this time. Nevertheless, we expect total payments volume to grow 6.5% in fiscal 2025.

Strong operating cash flow — up 26.4% in the first half of fiscal 2025 — enables Visa to reinvest in technology and strategic partnerships. These investments continue to drive cross-border transaction growth and reinforce its competitive edge. Its trailing 12-month return on capital stands at 35.7%, well above the industry average of 26.4%.

Visa also continues to innovate. It is advancing contactless, tap-to-pay, and scan-to-pay technologies while exploring crypto payment solutions. In April 2025, it launched “Visa Intelligent Commerce,” a new initiative to integrate AI into payments. This enables AI agents to securely search, compare and purchase items on behalf of users — yet another step toward building a smarter payments ecosystem. These initiatives, along with its value-added services, will help Visa diversify revenue sources.

Visa projects high single-digit to low double-digit revenue growth in fiscal 2025 (adjusted for nominal dollars), with operating expenses expected to grow at a similar pace. EPS is projected to grow at the high end of the low double-digit range.

The Zacks Consensus Estimate for Visa’s fiscal 2025 and fiscal 2026 EPS implies a 12.9% and 12.6% uptick, respectively, on a year-over-year basis. The earnings estimates remained stable over the past week. Also, the consensus mark for fiscal 2025 and fiscal 2026 revenues suggests a 10.3% and 10.5% increase, respectively.

It beat earnings estimates in each of the past four quarters, with an average surprise of 3%.

Visa Inc. price-eps-surprise | Visa Inc. Quote

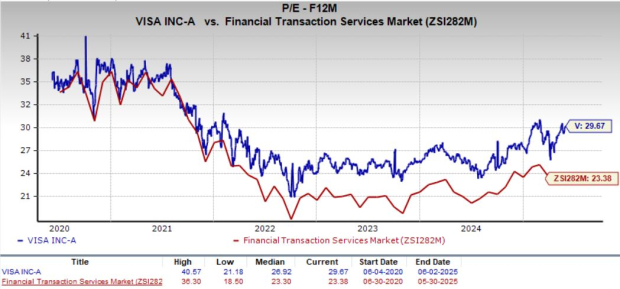

From a valuation perspective, Visa is trading higher than the industry. Going by its price/earnings (P/E) ratio, the company is trading at a forward earnings multiple of 29.67X, higher than its five-year median of 26.92X and the industry average of 23.38X. By comparison, Mastercard trades at 33.98X and American Express at 18.36X, placing Visa somewhere in the middle.

Visa's business faces challenges from rising expenses and potential regulatory hurdles that could impact its growth in the short term. Adjusted operating expenses jumped 10.8% and 9.2% in fiscal 2024 and the first half of fiscal 2025, respectively. Also, client incentives (a contra-revenue item) grew 11.9% and 14% year over year during those periods.

Legal and regulatory challenges are also mounting. In the United States, the Department of Justice has accused Visa and Mastercard of leveraging their market dominance to impose high fees on merchants. The Credit Card Competition Act of 2023 could increase competition and cap fee structures, potentially weighing on future growth.

In Europe, regulators are ramping up scrutiny as well. The European Commission and the U.K.’s Payment Systems Regulator are investigating the sharp rise in fees charged by Visa and Mastercard, which could result in new regulations or fee caps.

Visa remains a fundamentally strong company with a wide moat, impressive cash flows, and long-term growth potential. As such, for existing shareholders, holding the stock makes sense.

However, new investors may want to exercise caution. With shares trading near their 52-week high of $369.15 and valuation on the higher side, the short-term upside appears limited, especially amid regulatory uncertainty.

Visa currently has a Zacks Rank #3 (Hold), signaling a neutral outlook. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite