|

|

|

|

|||||

|

|

|

Disney's DIS recent partnership with Amazon AMZN-owned Amazon Ads represents a strategic move to enhance its advertising capabilities, but investors should exercise patience before adding shares to their portfolios. While the integration of Disney's Real-Time Ad Exchange with Amazon's demand-side platform promises improved ad targeting and revenue optimization, the deal alone does not constitute a compelling reason to buy Disney stock at current levels.

The partnership, announced at the Cannes Lions Festival, grants Amazon DSP direct access to premium inventory across Disney+, ESPN, and Hulu platforms. This makes Amazon only the third demand-side platform, alongside Google and The Trade Desk, to integrate with Disney's DRAX system. The collaboration enables advertisers to combine Disney's audience data with Amazon's extensive commerce insights, creating more precise targeting capabilities that could theoretically command higher advertising rates.

The Amazon partnership addresses a critical need for Disney's advertising business as the company seeks to maximize revenues from its ad-supported streaming tiers. By leveraging Amazon's commerce data, Disney can offer advertisers more sophisticated targeting options, potentially reducing ad frequency for consumers while improving campaign effectiveness. This enhanced capability could prove valuable as Madison Avenue grapples with an oversupply of connected TV inventory, particularly as more streaming services introduce ad-supported options.

However, the integration's impact on Disney's financial performance remains uncertain. The partnership will launch with select advertisers in the third quarter of 2025, meaning meaningful revenue contributions are unlikely to materialize until fiscal 2026. Additionally, while the deal expands Disney's addressable advertising market internationally to countries, including France, Germany, Italy, and the United Kingdom, the advertising business remains a relatively small portion of Disney's overall revenues compared to its Experiences and traditional content businesses.

The announcement follows Disney's solid second-quarter fiscal 2025 performance, which demonstrated the company's continued execution across its strategic priorities. Revenues increased 7% to $23.6 billion, while adjusted earnings per share grew 20% compared to the prior year. The Entertainment segment showed particular strength with operating income rising 61 percent, driven by improved Direct-to-Consumer results and Content Sales/Licensing performance.

Disney's streaming business continues its trajectory toward profitability, with Entertainment Direct-to-Consumer operating income reaching $336 million in the quarter. The company ended the period with more than 180 million Disney+ and Hulu subscriptions, representing an increase of 2.5 million from the previous quarter. Disney+ specifically grew to 126 million subscribers, demonstrating the platform's continued appeal despite increased competition in the streaming landscape.

The Zacks Consensus Estimate for fiscal 2025 revenues is pegged at $94.89 billion, indicating 3.86% year-over-year growth, with earnings expected to increase 15.9% to $5.76 per share. These projections suggest steady growth ahead.

The Walt Disney Company price-consensus-chart | The Walt Disney Company Quote

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Despite strong operational performance, Disney faces significant headwinds that warrant caution from investors. The company operates in an increasingly competitive streaming environment where content costs continue to escalate while subscription growth faces natural limits. Netflix NFLX, Amazon Prime Video, and newer entrants like Apple AAPL-owned Apple TV+ are all vying for the same subscriber base and advertising dollars, potentially pressuring Disney's ability to raise prices or maintain market share.

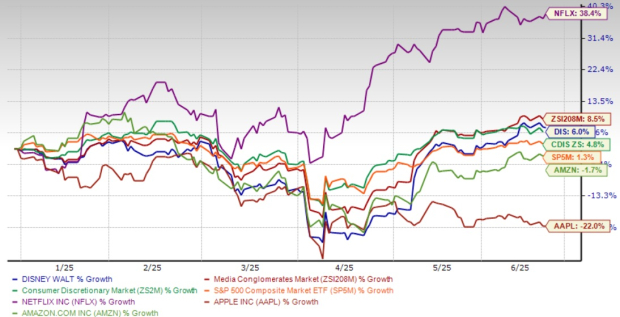

Shares of Disney have returned 6% in the year-to-date period against the Zacks Consumer Discretionary sector’s growth of 4.8%. While Netflix has returned 38.4% year to date, shares of Amazon and Apple have lost 1.7% and 22%, respectively.

The traditional linear television business continues its secular decline, with Disney's Linear Networks segment showing mixed results. The company's Sports segment also experienced headwinds, with operating income declining 12% due to higher programming costs despite revenue growth. Disney's Experiences segment, historically a reliable growth driver, showed resilience with operating income increasing 9%. However, international parks faced softness, particularly in China, reflecting broader macroeconomic uncertainties that could impact the company's global operations.

From a valuation perspective, Disney shares have reflected these mixed fundamentals. The company currently trades at 19.32 times forward 12-month price-to-earnings, notably below the Zacks Media Conglomerates industry average of 20.26 times. Investors should consider whether current prices adequately reflect the ongoing transformation challenges facing traditional media companies.

The Amazon partnership represents a positive step in Disney's advertising evolution, but it does not fundamentally alter the company's near-term investment thesis. Current shareholders should maintain their positions given Disney's strong brand portfolio, improving streaming economics, and robust Experiences business. However, prospective investors may benefit from waiting for a better entry point, potentially in fiscal 2026, when the benefits of the Amazon partnership and other strategic initiatives become more apparent in financial results.

Disney remains a high-quality company with valuable intellectual property and diverse revenue streams, but the stock requires patience as management navigates the ongoing media industry transformation. Disney currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour |

Warren Buffett's company invests in the New York Times six years after he sold all his newspapers

AAPL

Associated Press Finance

|

| 1 hour | |

| 2 hours |

Berkshire Hathaway Takes Stake In New York Times, Cuts Apple, Amazon Holdings

AAPL AMZN

Investor's Business Daily

|

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite