|

|

|

|

|||||

|

|

|

Quantum computing is one of the most transformative emerging technologies, with the potential to revolutionize industries from healthcare to finance. Two companies at the forefront of this field are IonQ, Inc. IONQ and International Business Machines IBM. IonQ is a pure-play quantum computing upstart, while IBM is a diversified tech giant with a significant quantum computing division.

IonQ specializes exclusively in quantum computing and networking, aiming to commercialize quantum technology for real-world use. IBM, on the other hand, is a century-old enterprise IT leader that has expanded into cloud, AI, and quantum, leveraging its vast resources to pursue long-term innovation.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

IonQ is one of the few publicly traded pure-play quantum computing companies, and it has rapidly positioned itself as a leader in this nascent industry. IonQ develops advanced trapped-ion quantum computers known for high qubit fidelity and all-to-all connectivity. Its flagship system, IonQ Forte, features 36 algorithmic qubits and has outperformed classical computing in specific tasks. For example, a recent collaboration with Ansys demonstrated Forte’s ability to simulate a medical device 12% faster than a classical supercomputer, signaling a potential quantum advantage in practical applications. These achievements highlight IonQ's innovation and its focus on addressing complex real-world challenges.

IonQ’s growth is being propelled by a dual focus on commercial expansion and deepening its technological edge. The company continues to secure high-value government contracts, including over $75 million in aggregate deals with the U.S. Air Force, while also gaining recognition from DARPA, affirming its leadership in quantum computing. Internationally, IonQ has expanded into Japan through partnerships with Toyota Tsusho and AIST, and it continues to work with global companies like Hyundai and Airbus.

Strategic acquisitions in quantum networking, including stakes in ID Quantique and Qubitekk, have positioned IonQ as a frontrunner in secure quantum communications, now backed by nearly 400 patents. The company further advanced commercialization with its first-quarter 2025 launch of a quantum computing and networking hub in partnership with EPB, generating $22 million in revenues and embedding its Forte Enterprise system into real-world energy grid applications.

From the financial performance perspective, IonQ’s first-quarter 2025 revenues of $7.6 million reflect steady early-stage growth in a still-nascent industry. The company expects 2025 revenues of $75–$95 million, signaling strong momentum as new contracts and acquisitions begin contributing. While IonQ remains unprofitable, with a first-quarter net loss of $32.3 million, losses have narrowed and are well-supported by a solid financial foundation. As of March 31, 2025, the company held $697.1 million in cash and investments, ample capital to fund R&D and expansion for several years without immediate financial pressure.

IBM is a diversified technology leader with a storied history, and it has been investing in quantum computing research for over two decades. Unlike IonQ, IBM’s quantum initiatives are just one part of a broad portfolio spanning enterprise hardware, software, cloud services, and consulting.

IBM remains a global leader in quantum computing, with one of the largest operational quantum fleets and a clear roadmap toward scaling. The 2023 launch of “Condor,” the first 1,121-qubit superconducting processor, marked a major milestone, and the company aims to reach 100,000 qubits by 2033. Although quantum is not yet a major revenue driver, IBM’s vast R&D resources and long-term vision—supported by its cloud platform and academic partnerships—allow it to pursue breakthroughs methodically, integrating quantum capabilities into its broader enterprise and research ecosystem.

IBM’s investment case is anchored in its strong core businesses—hybrid cloud, software, and consulting—which continue to generate the cash flow fueling its quantum and AI ambitions. In first-quarter 2025, IBM reported $14.5 billion in revenues, up 0.6% year over year, with high-margin software growing 7% thanks to robust demand for Red Hat, automation, AI, and security solutions. Gross margin rose 170 basis points (bps) to 55.2%, and despite a slight dip in consulting revenue, IBM maintained its outlook for mid-single-digit growth in that segment. The company also posted $2 billion in free cash flow, its best first quarter in years, and reaffirmed its full-year target of $13.5 billion, supporting both reinvestment and a healthy 4–5% dividend yield.

Strategically, IBM has been streamlining and investing aggressively to position itself for long-term growth. After spinning off Kyndryl, IBM has focused on acquiring high-value assets such as HashiCorp to strengthen its cloud automation capabilities, alongside earlier buys like Turbonomic and Apptio. It is also expanding in AI and cybersecurity consulting. The 2023 launch of Watsonx marked a key step in delivering enterprise-grade generative AI, complementing IBM’s hybrid cloud and quantum computing efforts. These initiatives enhance IBM’s positioning at the intersection of AI, cloud, and quantum innovation.

IonQ stock surged 484.9% over the past year amid growing interest in the quantum computing sector. Even after some volatility in 2025, IonQ shares are still up 79.9% over the past three months. Meanwhile, IBM stock has surged 68.8% over the past year and 19.6% over the past three months. The market is recognizing IBM’s steady progress.

3-Month Share Price Performance

Having a market capitalization of around $10.8 billion, IonQ stock has been volatile, reflecting the high expectations built into its valuation. IonQ’s forward 12-month price/sales (P/S) ratio of 99.04 is far above the Zacks Computer - Integrated Systems industry average of 3.92.

IONQ Valuation

IBM trades at a forward 12-month P/S ratio of 4.00, above the industry.

IBM Valuation

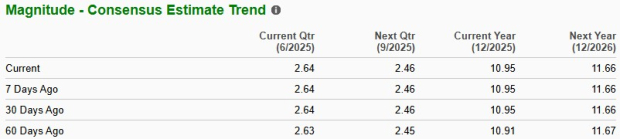

IONQ & IBM Estimate Revision Trend

For IONQ, the Zacks Consensus Estimate for 2025 loss per share has narrowed over the past 60 days, as you can see below, depicting analysts’ optimism. The estimated figure indicates a much narrower loss than the year-ago reported loss of $1.56 per share. The Zacks Consensus Estimate for 2025 revenues implies year-over-year growth of 97.3%.

For IONQ Stock

For IBM, the Zacks Consensus Estimate for 2025 earnings per share has increased over the past 60 days, as you can see below, depicting analysts’ optimism. The estimated figure indicates 6% growth from the year-ago profit level. The Zacks Consensus Estimate for 2025 revenues implies year-over-year growth of 5.5%.

For IBM Stock

Both IonQ and IBM are compelling in their ways, but they cater to different investor profiles. IonQ is a high-risk, high-reward play on pure quantum computing innovation. The company is growing rapidly, aiming to nearly double revenue this year, and has amassed strategic partnerships, government contracts, and technological milestones that position it at the forefront of the quantum race. With a Zacks Rank #2 (Buy), reflecting positive analyst sentiment, IonQ appears to have the stronger near-term upside potential. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

IBM, by contrast, offers a balanced investment grounded in present-day fundamentals with a foot in the future. IBM is a Zacks Rank #3 (Hold) stock – essentially a market-performer expectation — and that makes sense given its moderate growth outlook. It provides reliable income (via dividends) and has proven execution in cloud and software, which should deliver steady returns.

While IBM is an excellent company with a foothold in quantum, its stock is more of a steady compounder. Therefore, if you’re an investor bullish on quantum computing’s future and willing to embrace some risk, IonQ stock appears to hold better upside potential than IBM at this time.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 hours | |

| 11 hours | |

| 15 hours | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 |

Phonographs, Player Pianos and Betamax: The Inventions That Transformed Entertainment

IBM

The Wall Street Journal

|

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite