|

|

|

|

|||||

|

|

|

Howmet Aerospace Inc.’s HWM investors have been witnessing some short-term gains from the stock of late. Shares of the advanced engineered solutions provider for the aerospace and transportation industries have surged 65.6% in the year-to-date period, outpacing the S&P 500 composite’s rise of 6.2% and the industry’s 22.2% growth. The company has also outperformed other industry players like GE Aerospace GE and RTX Corporation RTX, which have returned 48% and 26%, respectively, over the said time frame.

Closing at $181.06 on Thursday, the stock is trading near its 52-week high of $187.51 and significantly higher than its 52-week low of $77.22. The stock is trading above both its 50-day and 200-day moving averages, indicating solid upward momentum and price stability. This reflects a positive market sentiment and confidence in the company's financial health and long-term prospects.

The strongest driver of Howmet Aerospace’s business at the moment is the commercial aerospace market. The strength in air travel continues, with wide-body aircraft demand picking up, supporting continued OEM spending. Pickup in air travel has been a growth driver for the company because the increased usage of aircraft spurs spending on parts and products that it provides.

Revenues from the commercial aerospace market increased 9% year over year in the first quarter of 2025, constituting 52% of its business. The primary driver of HWM’s performance was attributed to increased demand for new, more fuel-efficient aircraft with reduced carbon emissions and increased spare demand for engines. The Boeing Company BA is also anticipated to witness a gradual production recovery, particularly in the Boeing 737 MAX aircraft, which is likely to boost demand for Howmet Aerospace’s products in the market.

Howmet Aerospace is also benefiting from the positive momentum of the defense business, cushioned by steady government support. HWM has been experiencing robust orders for engine spares for the F-35 program and other legacy fighters. Revenues from the defense aerospace market increased 19% year over year in the first quarter, constituting 17% of the company’s business.

In August 2024, the U.S. Senate Committee on Appropriations approved the fiscal year 2025 Defense Appropriations Act, which provides $852.2 billion in total funding. Such robust budgetary provisions set the stage for Howmet Aerospace, focused on the defense business, to win more contracts, which is likely to boost its top line.

Howmet Aerospace’s measures to reward shareholders are also encouraging. In first-quarter 2025, the company paid dividends of $42 million and repurchased shares worth $125 million. Also, in 2024, it paid dividends worth $109 million and repurchased shares for $500 million.

In January 2025, Howmet Aerospace hiked its quarterly dividend by 25% to 10 cents per share. Also, in July 2024, its board approved an increase in the share repurchase program by $2 billion to $2.487 billion of its common stock. As of April 30, 2025, HWM’s total share repurchase authorization available was $2 billion.

The company’s sound liquidity position is an added positive. Exiting the first quarter, Howmet Aerospace’s cash equivalents and receivables were $536 million against short-term maturities of $7 million. While HWM generated net cash of $253 million from operating activities, its healthy free cash flow totaled $134 million in the first three months of 2025.

Earnings estimates for HWM have moved north over the past 60 days, reflecting analysts’ optimism. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

The Zacks Consensus Estimate for 2025 earnings is pegged at $3.47 per share, indicating an increase of 2.4% in the past 60 days. The figure indicates year-over-year growth of 29%. The consensus mark for 2026 earnings is pinned at $4.11 per share, increasing 5.7% in the same period. The figure also indicates year-over-year growth of 18.7%.

HWM’s Return on Assets (ROA) is 11.48%, compared with the industry’s 2.39%, indicating that the company has been utilizing its assets efficiently to generate returns. In comparison, ROA for GE Aerospace, RTX Corp. and Boeing is pegged at 4.51%, 4.84% and (8.6%), respectively.

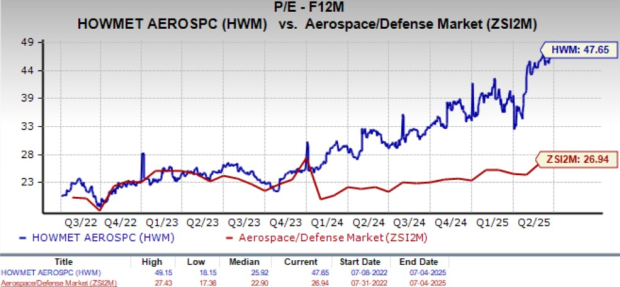

Despite the positives, Howmet Aerospace’s lofty valuation remains a concern. The stock is trading at a forward 12-month price-to-earnings (P/E) ratio of 47.65X, much higher than the industry average of 26.94X. Also, the stock is overvalued compared with GE Aerospace and RTX Corp., which are trading at 41.18X and 22.92X, respectively.

Strong momentum across the commercial and defense aerospace markets, supported by impressive build rates, spare demand for engines and increased defense budget, positions Howmet Aerospace favorably for solid growth in the quarters ahead. Built on a sound liquidity position, HWM’s shareholder-friendly policies also add to its appeal.

Despite its expensive valuation, positive analyst sentiment and robust growth prospects indicate it is the right time for potential investors to bet on this Zacks Rank #1 (Strong Buy) company. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours |

Boeing Wins Big As Farnborough Airshow Takes Off. Airbus, RTX Land Deals.

BA

Investor's Business Daily

|

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite