|

|

|

|

|||||

|

|

|

Over the past six months, Knowles’s shares (currently trading at $18.08) have posted a disappointing 7% loss, well below the S&P 500’s 6.9% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Knowles, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Even though the stock has become cheaper, we don't have much confidence in Knowles. Here are three reasons why KN doesn't excite us and a stock we'd rather own.

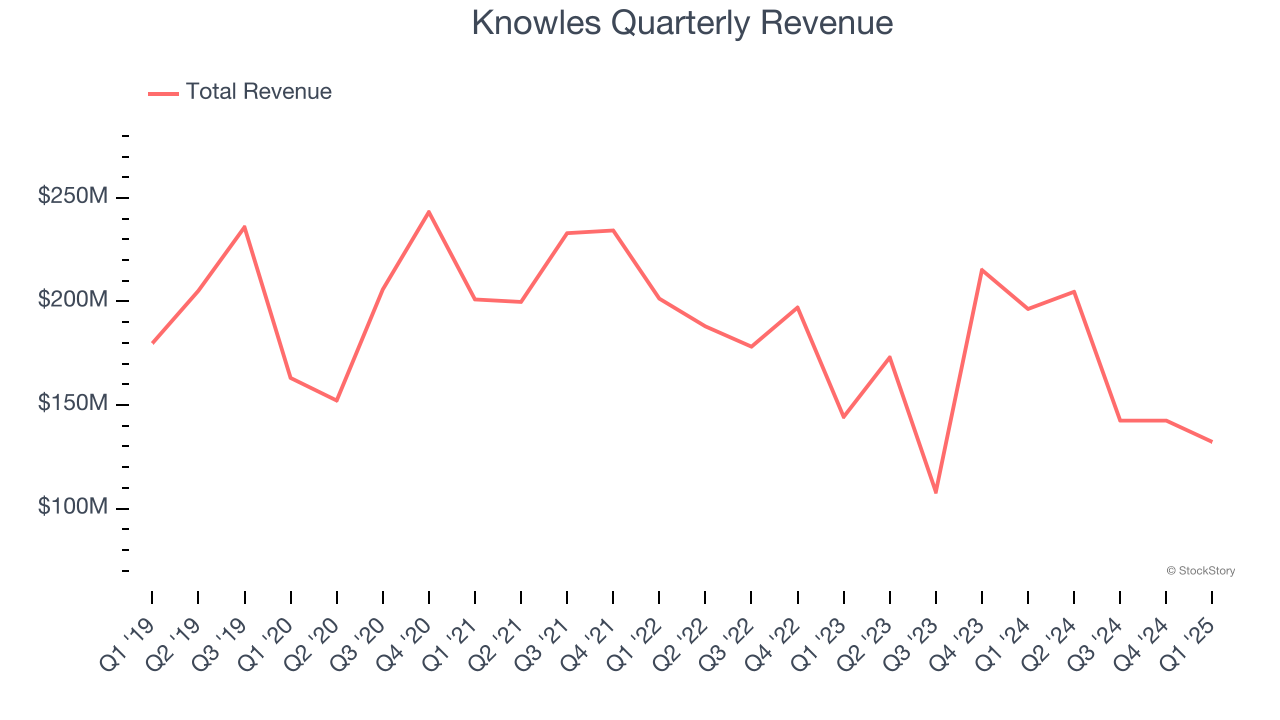

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Knowles’s demand was weak over the last four years as its sales fell at a 6.2% annual rate. This was below our standards and signals it’s a low quality business.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Knowles’s revenue to drop by 7.2%, close to its 6.2% annualized declines for the past four years. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

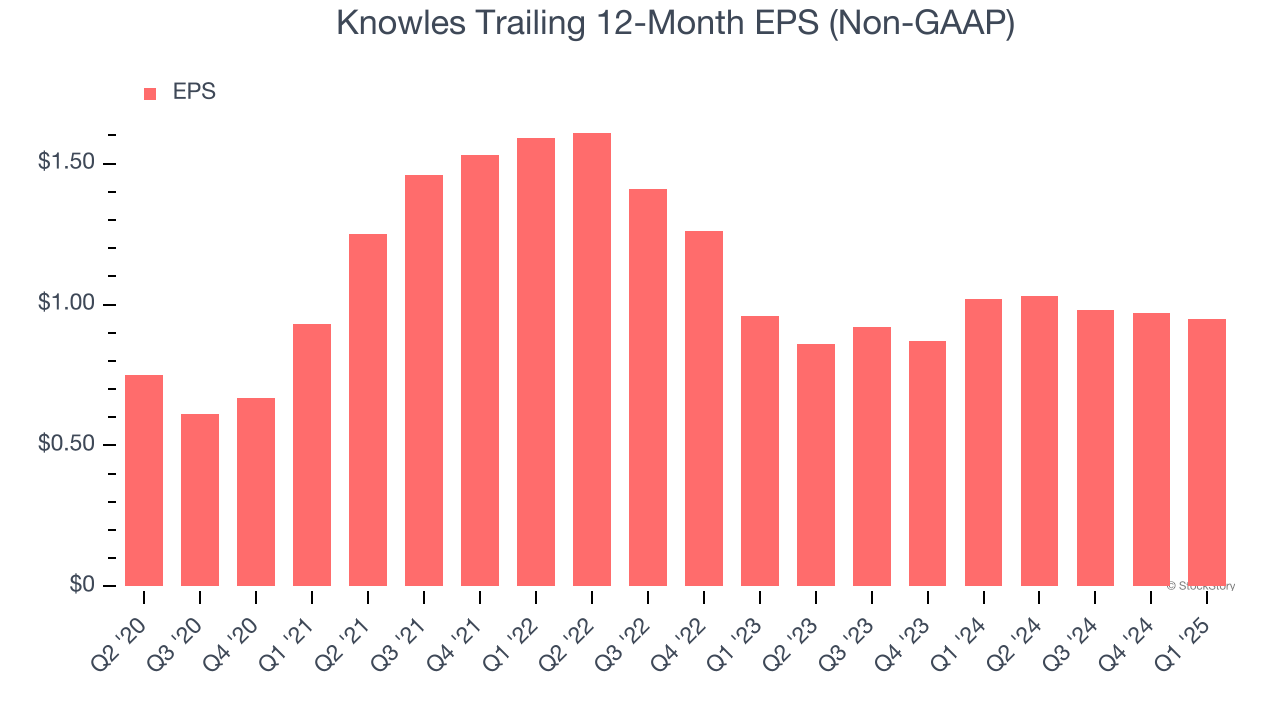

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Knowles’s full-year EPS dropped 6.9%, or 1.4% annually, over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Knowles’s low margin of safety could leave its stock price susceptible to large downswings.

Knowles doesn’t pass our quality test. After the recent drawdown, the stock trades at 16.3× forward P/E (or $18.08 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward one of our all-time favorite software stocks.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-06 | |

| Jul-06 | |

| Jul-01 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-13 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite