|

|

|

|

|||||

|

|

|

Rocket Lab USA, Inc. (RKLB) is making strong progress in the space services sector through a contract signing with Bollinger Shipyards (announced last week) to build an ocean landing platform for its upcoming Neutron reusable rocket. The 400-foot vessel, named Return On Investment, will be fitted with Rocket Lab’s technology, including systems to support rocket landings at sea. The platform is expected to be delivered in early 2026.

With 68 successful Electron missions and strong partnerships with NASA and the U.S. government, Rocket Lab is already enjoying a strong prominence in the small satellite launch market. With the Neutron project, the company plans to serve larger payload missions and thereby grow its services beyond small satellite launches.

As global demand for satellite services and national security solutions increases, investor interest in the space technology sector is on the rise. Against this backdrop, the latest contract signing news may lead space-focused investors to consider buying RKLB. However, before making a decision, let’s take a look at the stock’s performance, growth opportunities, valuation, and potential risks to make a more informed decision.

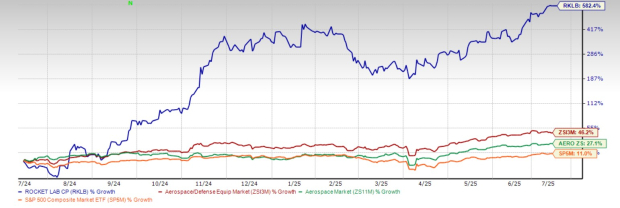

RKLB’s shares have surged a solid 582.4% in the past year, outperforming the Zacks Aerospace-Defense-Equipment industry’s growth of 46.2% and the broader Zacks Aerospace sector’s return of 27.1%. It has also surpassed the S&P 500’s return of 11% in the same time frame.

A similar stellar performance has been delivered by other defense stocks involved in the space industry, such as The Boeing Company (BA) and Intuitive Machines (LUNR), over the past year. Shares of LUNR have surged 150.8%, while BA shares have risen 26.7%.

Rocket Lab continues to build growth momentum through successful missions, strong partnerships and new product development. In June 2025, the company launched its 68th Electron rocket for a confidential commercial customer. This represented the 10th Electron mission, with 100% mission success so far this year.

These frequent launches should support Rocket Lab’s goal of completing more than 20 Electron missions this year, reflecting strong demand for its services and building trust among commercial and government clients. This, in turn, might attract more customers to select RKLB for their satellite launches and thereby boost the company’s revenue growth in future quarters.

Additionally, Rocket Lab is preparing for the first launch of its Neutron rocket, expected in the second half of 2025, to which the recent contract to build an ocean landing platform will play the role of a major catalyst. This should help Rocket Lab expand beyond small satellite launches and compete with larger players in the space industry.

Let’s take a look at RKLB’s near-term estimates to check if that reflects solid growth prospects.

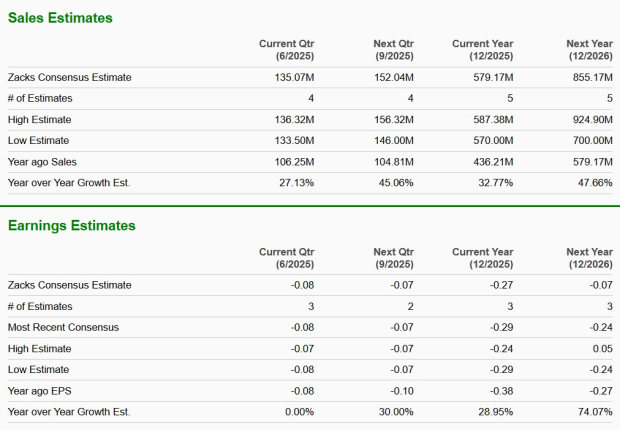

The Zacks Consensus Estimate for RKLB’s 2025 and 2026 sales suggests an improvement of 32.8% and 47.7%, respectively, year over year. A look at its 2025 and 2026 earnings estimates suggests a similar year-over-year improvement.

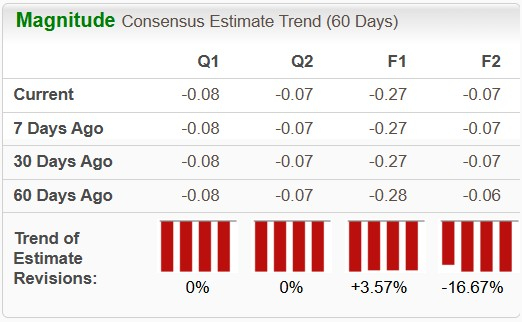

The upward revision of its 2025 estimates over the past 60 days indicates investors’ increasing confidence in the stock’s earnings generation capabilities. However, its 2026 estimates have moved south over the past 60 days.

Rocket Lab offers strong near-term growth prospects, but there are a few important risks investors should be aware of. One key concern is the company’s high operating costs, driven by continuous investments in advanced technologies like the Neutron rocket, satellite platforms, and various space components. These expenses often outweigh revenue growth, resulting in ongoing losses, as reflected in recent quarterly results.

Another challenge is Rocket Lab’s higher debt levels compared to its industry peers, as is evident from the below provided long-term debt-to-capital ratio of the stock. As the company continues to actively invest in the development and commercialization of new space systems, which are highly capital-intensive, its higher debt burden, which might cause financial risk during economic downturns, remains a concern. RKLB’s current long-term debt-to-capital ratio is pinned at 49.25 compared with the industry’s average of 46.51.

In terms of valuation, RKLB’s forward 12-month price-to-sales (P/S) is 24.36X, a premium to its peer group’s average of 9.88X. This suggests that investors will be paying a higher price than the company's expected sales growth compared to that of its industry.

Other space stocks, such as LUNR and BA, are trading at a discount to RKLB in terms of their forward P/S ratio. LUNR and BA have a forward sales multiple of 5.79X and 1.87X, respectively.

To conclude, despite its recent outperformance at the bourses and upbeat sales estimate, RKLB’s premium valuation and high leverage raise red flags. Given these concerns, it may be prudent for investors to wait for clearer signs of stability, in terms of leverage, before making a decision.

The stock’s Zacks Rank #4 (Sell) further supports our thesis.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 21 min | |

| 24 min | |

| 30 min | |

| 32 min | |

| 34 min | |

| 38 min | |

| 40 min | |

| 1 hour |

Rocket Lab Reports Earnings Tonight: What Do Prediction Markets Say About Neutron Launches in 2026?

RKLB

Benzinga Prediction Markets

|

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite