|

|

|

|

|||||

|

|

|

International Business Machines Corporation IBM and Amazon.com, Inc. AMZN are leading players in the global cloud computing industry. IBM offers cloud and data solutions that aid enterprises in digital transformation. In addition to hybrid cloud services, the company provides advanced information technology solutions, computer systems, quantum computing and supercomputing solutions, enterprise software, storage systems and microelectronics.

On the other hand, Amazon Web Services (“AWS”) is the world’s most comprehensive and widely adopted on-demand cloud computing platform, offering more than 200 fully featured services from data centers globally. Millions of customers, including the fastest-growing startups, largest enterprises and leading government agencies, are using AWS to lower costs, become more agile and innovate faster. It reportedly offers the widest variety of databases that are purpose-built for different types of applications to enable subscribers to choose the right tool for the job.

With a focus on hybrid cloud and AI (artificial intelligence), both IBM and Amazon are strategically positioned in the cloud infrastructure market and have the wherewithal to cater to the evolving demands of business enterprises. Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

IBM is poised to benefit from healthy demand trends for hybrid cloud and AI, which drive the Software and Consulting segments. The company’s growth is expected to be aided by analytics, cloud computing and security in the long term. IBM has extended its collaboration with NVIDIA Corporation NVDA to scale AI workloads and agentic AI applications. Per the latest agreement, IBM aims to launch a content-aware storage (CAS) capability for its hybrid cloud infrastructure offering (dubbed IBM Fusion) and expand its watsonx integrations with NVIDIA while introducing new IBM Consulting capabilities.

The CAS capability will enable firms to extract the hidden meaning of unstructured data for inferencing to scale and enhance AI applications without compromising security. The integration of watsonx with NVIDIA Inference Microservices will offer firms greater accessibility to leading AI models across multiple cloud environments. IBM’s watsonx platform is likely to be the core technology platform for its AI capabilities. This enterprise-ready AI and data platform delivers the value of foundational models to the enterprise, enabling them to be more productive.

Despite solid hybrid cloud and AI traction, IBM is facing stiff competition from AWS and Microsoft Corporation’s MSFT Azure. Increasing pricing pressure is eroding margins, and profitability has trended down over the years, barring occasional spikes. The company’s ongoing, heavily time-consuming business model transition to the cloud is a challenging task. Weakness in its traditional business and foreign exchange volatility remain significant concerns.

Amazon is the leading provider of cloud infrastructure as a service to enterprise customers. The expanding customer base of AWS, driven by its strengthening cloud offerings, will continue to aid Amazon's dominance in the global cloud space. Amazon’s strategic expansion of its Bedrock platform has positioned it as a frontrunner in the enterprise AI race. Amazon Bedrock has emerged as a game-changing, fully managed service that offers enterprises seamless access to high-performing foundation models from leading AI companies. The platform's recent developments, including automated reasoning checks and multi-agent collaboration capabilities, address critical challenges in AI adoption while opening new revenue streams for Amazon's cloud division.

The company is investing heavily in AI infrastructure, including the development of custom AI silicon like Trainium 2, which offers 30-40% better price performance than competing GPU-powered instances. Amazon aims to extend AWS’ AI and machine learning (ML) capabilities to facilitate improved decision-making. It intends to expand its global infrastructure for faster and more reliable service with low latency and maximum availability. From cloud-native applications and AI-driven solutions to edge computing and sustainability initiatives, AWS is likely to push the limits in the realm of cloud computing technology.

However, the substantial capital expenditure required for AI infrastructure expansion may weigh on margins in the coming quarters. In addition, while AWS' growth remains impressive, the company faces capacity constraints in AI services that could limit near-term growth potential. Moreover, AWS has historically been less open to hybrid cloud than rivals like Microsoft Azure, which integrates well with on-premise environments via tools like Azure Arc. Data localization laws and stricter regulatory requirements create friction for AWS' global expansion, while stringent government scrutiny in regions like the EU and China adds compliance complexity.

The Zacks Consensus Estimate for IBM’s 2025 sales and EPS implies year-over-year growth of 5.5% and 6%, respectively. The EPS estimates, however, have remained static over the past 60 days.

The Zacks Consensus Estimate for Amazon’s 2025 sales and EPS implies year-over-year growth of 8.9% and 12.7%, respectively. The EPS estimates have been trending northward over the past 60 days.

Over the past year, IBM has gained 52.6% compared with the industry’s growth of 7.2%. Amazon rose 16.9% over the same period.

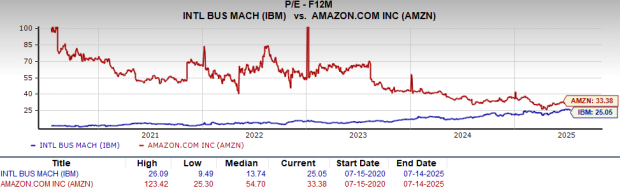

IBM looks more attractive than Amazon from a valuation standpoint. Going by the price/earnings ratio, IBM’s shares currently trade at 25.05 forward earnings, significantly lower than Amazon’s 33.38.

IBM carries a Zacks Rank #3 (Hold), while Amazon carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both companies expect their sales and profits to improve in 2025. Long-term earnings growth expectations for IBM and AMZN are 4.3% and 21.4%, respectively. IBM has a better price performance and attractive valuation metric compared with Amazon. However, Amazon has shown steady revenue and EPS growth for years, while IBM has been facing a bumpy road. With a VGM Score of A and a superior Zacks Rank, Amazon seems to be a better investment option at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 37 min | |

| 53 min | |

| 1 hour | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite