|

|

|

|

|||||

|

|

|

Mondelez has had an impressive run over the past six months as its shares have beaten the S&P 500 by 11.6%. The stock now trades at $67.14, marking a 16% gain. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Mondelez, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

We’re glad investors have benefited from the price increase, but we don't have much confidence in Mondelez. Here are three reasons why we avoid MDLZ and a stock we'd rather own.

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Looking at the trend in its profitability, Mondelez’s operating margin decreased by 6.8 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 11.8%.

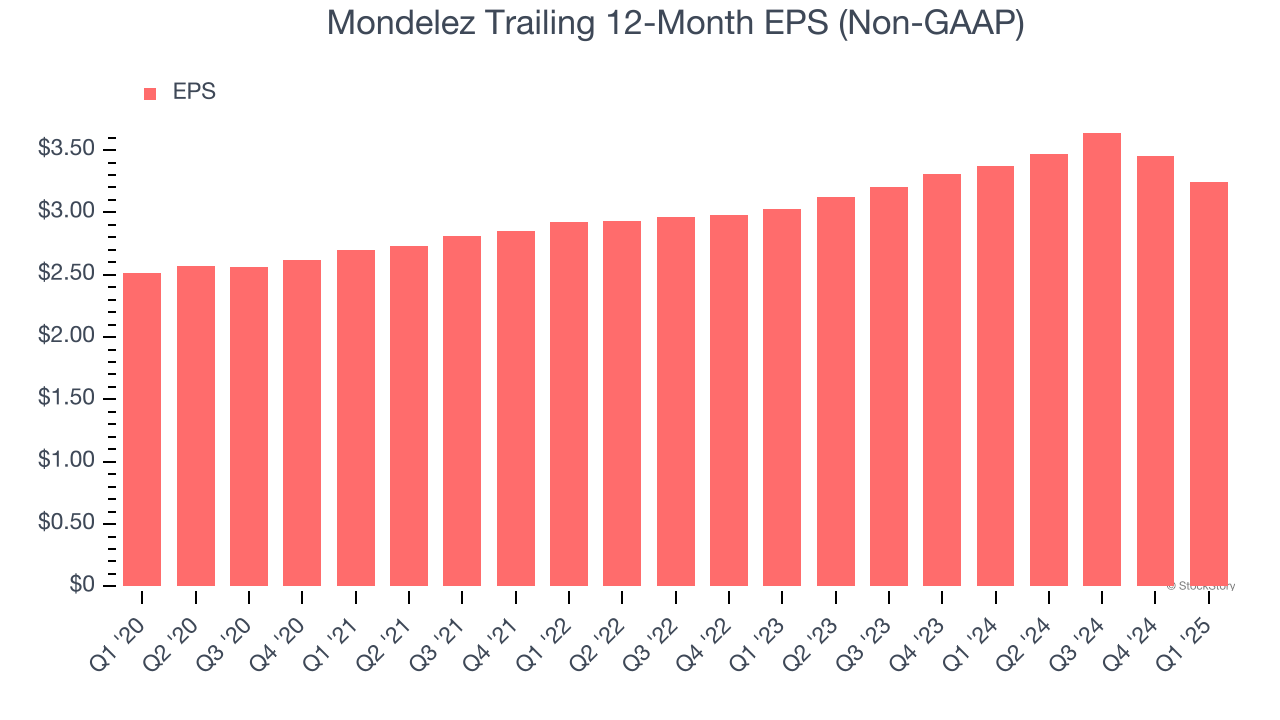

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Mondelez’s EPS grew at an unimpressive 3.5% compounded annual growth rate over the last three years, lower than its 7.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

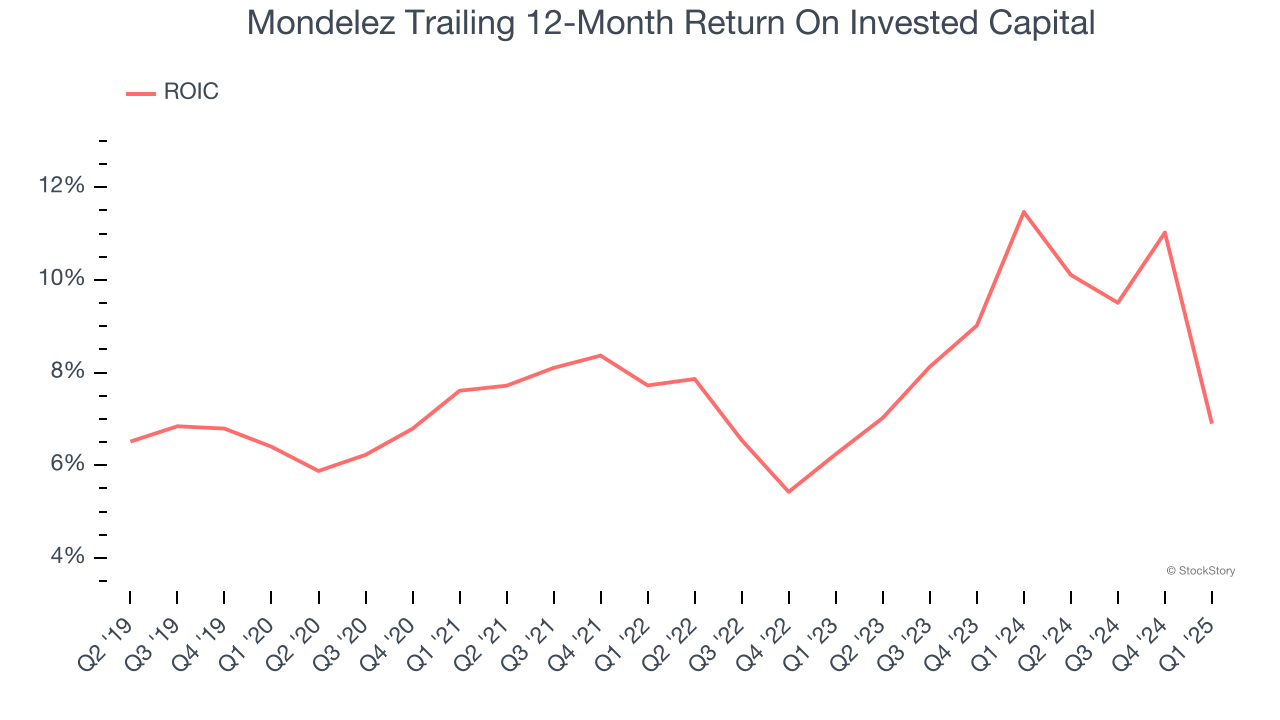

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Mondelez historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

Mondelez’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 22.4× forward P/E (or $67.14 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at the Amazon and PayPal of Latin America.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-19 | |

| Feb-19 | |

| Feb-17 | |

| Feb-17 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite