|

|

|

|

|||||

|

|

|

Amazon’s flexibility is the source of its competitive edge, and the reason it can continue growing indefinitely.

Uber Technologies is plugged into a major societal shift that could fuel big growth well into the distant future.

American Express’ business is more -- and more resilient -- than it seems on the surface.

Is your retirement nest egg where it needs to be right now? That is to say, is it big enough at this stage of your life to ensure it will be big enough then?

Most Americans don't think theirs is. Although most people are saving something, as data from The Motley Fool's in-house research arm highlights, only 34% of Americans feel like they're actually on track for the comfortable retirement they're envisioning for themselves. The other 66% fear their golden years are going to be underfunded.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

If you're one of the 66%, although you can't go back in time and change the past, you can change your current growth trajectory by owning more of the right growth stocks. Here's a closer look at three such names that could beef up the returns on your retirement savings.

Yes, Amazon (NASDAQ: AMZN) is a frequently recommended trade. It's almost a cliché, in fact. The stock's also one of the market's most reliable long-term performers, with a future that's just as bright as its brilliant past.

Amazon is not only one of the stock market's biggest companies in terms of market cap, it is the top name in North American e-commerce. Numbers from Digital Commerce 360 indicate that Amazon consistently controls roughly 40% of the continent's ever-growing online shopping industry. While its overseas reach isn't nearly as wide, its international arm is now at least reliably operationally profitable as well, thanks to several years of steady growth.

Yet, e-commerce isn't Amazon's breadwinning business. Although it only accounts for about 16% of its total top line, its cloud computing arm, Amazon Web Services, produces on the order of 60% of the company's total earnings. The growth of both types of business has produced consistent double-digit sales growth for years, which is expected to remain firm for least several more.

Image source: Getty Images.

Amazon's peer-beating growth rate could actually last indefinitely for one overarching reason. That's Amazon's ability and willingness to adapt -- or even enter new lines of business -- as merited.

Think about it. This company hasn't always been in the cloud computing business. That arm wasn't launched until 2006. Amazon Prime didn't exist until 2005. Even its most basic e-commerce operation has evolved since its infancy. While the website still looks about the same as it did years ago, it's now being monetized as an advertising medium more so than an e-commerce platform. Amazon collected more than $56 billion worth of high-margin ad revenue from its sellers last year, in exchange for featuring their goods. For perspective, that's more operating profit than its domestic and international e-commerce arms produced on a combined basis.

There's every reason to believe Amazon can and will remain a growth monster well into the distant future.

Ride-hailing outfit Uber Technologies (NYSE: UBER) isn't just catching on with consumers. It's tapped into a massive sociocultural shift. That's the fading interest in car ownership in favor of using alternative forms of personal mobility (like ride-hailing).

Data from the Federal Highway Administration puts things in perspective, highlighting how the number of licensed U.S. drivers between the ages of 16 and 19 has fallen from 65% as of 1995 to only about one-third now. That's just part of a much bigger paradigm. More and more people are never getting their license at any age.

Then again, why would they become licensed drivers if they're less and less likely to own a car to drive?

While older drivers remain relatively interested in ownership of a vehicle, data from a recent survey performed by Deloitte indicates that 44% of Americans between the ages of 18 and 34 would be willing to not own their own car. This disinterest is growing as time marches on, pointing not just to changing preferences, but a major societal shift as to what constitutes "normal" mobility options.

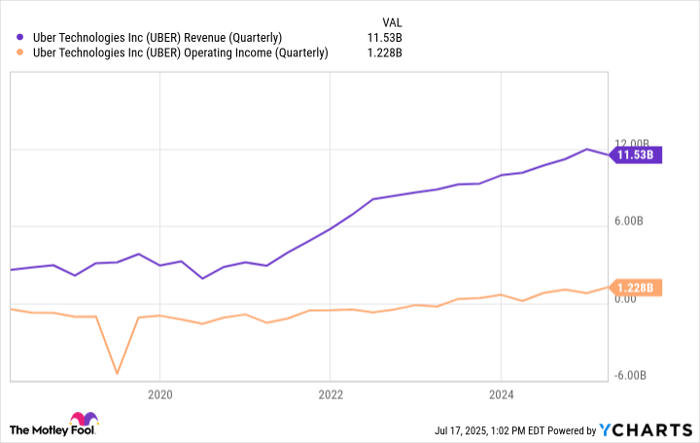

Uber Technologies' results have long reflected its role in this shift. Revenue growth in the mid-teens is the norm now, and likely to remain the norm for a long while as individual car ownership continues to decline. An outlook from Straits Research suggests that the worldwide ride-hailing and taxi market is poised to grow at an average annualized pace of more than 11% through 2033, although this pace of progress could last far longer than that.

UBER Revenue (Quarterly) data by YCharts.

The kicker: People are quickly falling in love with the idea of same-day delivery of online purchases too, which Uber now also offers. On a constant-currency basis, Uber's delivery revenue grew 22% to nearly $3.8 billion in the first quarter of this year, and now accounts for a little over 30% of the company's total top line.

Finally, add American Express (NYSE: AXP) to your list of stocks you can -- and arguably should -- buy and hold for decades in your retirement account.

Ostensibly it's a credit card outfit, in the same vein as Visa and Mastercard. There are certainly plenty of similarities between the three companies. There are also a couple of critical distinguishing factors, however.

Whereas Visa and Mastercard only manage payment networks and charge a modest fee for each purchase they facilitate, American Express manages its own payment network in addition to being the credit card issuer itself. This is no trivial detail, either. This much control of the purchase and payment process means serious operational savings.

Perhaps the more important factor at work here, however, is the fact that American Express isn't as much of a credit card middleman as it is an operator of a perks and rewards program that just so happens to be built around credit cards. Some people are willing to pay up to $695 per year just to be able to access private airport lounges, enjoy discounted hotel stays, and receive credit toward entertainment purchases and ride-hailing services (and more).

This makes American Express cards particularly appealing to a more affluent crowd that's less likely to curtail their spending or fail to make payments when economic headwinds constrict personal budgets. That's a nuance that the company's management wasn't shy about highlighting following April's release of its first-quarter results.

You'll probably never see double-digit growth from American Express. You certainly haven't in the recent or not-so-recent past! You will, however, see persistent revenue and profit growth supporting consistent dividend growth and stock buybacks, which quietly add value in their own often-overlooked way. That's how an investment in this stock has easily beaten the performance of the S&P 500 over the course of the past 30 years, when reinvesting the dividends it's paid since then.

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $652,133!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,056,790!*

Now, it’s worth noting Stock Advisor’s total average return is 1,048% — a market-crushing outperformance compared to 180% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 15, 2025

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. American Express is an advertising partner of Motley Fool Money. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Mastercard, Uber Technologies, and Visa. The Motley Fool has a disclosure policy.

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 11 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| 13 hours | |

| 14 hours | |

| 14 hours | |

| 15 hours | |

| 16 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite