|

|

|

|

|||||

|

|

|

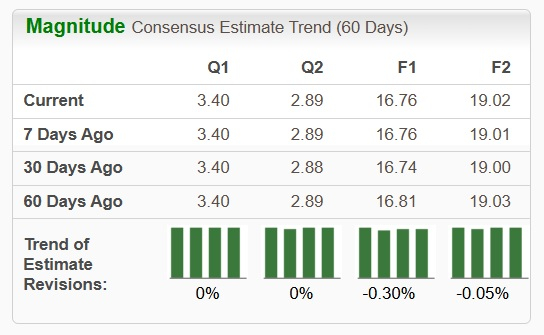

Aon plc AON is scheduled to release second-quarter 2025 results on July 25, before the opening bell. The Zacks Consensus Estimate for earnings is pegged at $3.40 per share, which indicates an improvement of 16% from the prior-year quarter’s number. Management expects it to witness 15-18% year-over-year growth in the same time frame.

The second-quarter earnings estimate remained stable over the past 30 days. Meanwhile, the Zacks Consensus Estimate for revenues is pegged at $4.1 billion, implying 9.7% growth from the year-ago quarter’s figure.

Aon’s bottom line beat estimates in two of the trailing four quarters and missed the mark twice, the average surprise being 0.99%. This is depicted in the chart below:

Aon plc price-eps-surprise | Aon plc Quote

Our proven model predicts an earnings beat for Aon this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here.

Earnings ESP: Aon has an Earnings ESP of +1.27% because the Most Accurate Estimate of $3.45 per share is pegged higher than the Zacks Consensus Estimate of $3.40. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

Zacks Rank: AON currently carries a Zacks Rank of 3.

In the second quarter, Aon's revenues are expected to have gained on strong contributions from Commercial Risk Solutions, Reinsurance Solutions, Health Solutions and Wealth Solutions businesses. Performance of Commercial Risk Solutions is anticipated to have benefited from a strong international property and casualty business, which, in turn, is likely to have been driven by strong retention rates and new business growth.

The Zacks Consensus Estimate for Commercial Risk Solutions’ revenues is pegged at $2.2 billion, indicating 7.5% year-over-year growth. Our estimate for the metric indicates a 6% year-over-year rise in the to-be-reported quarter.

The Reinsurance Solutions unit is expected to have benefited on the back of improved treaty placements and strong growth in facultative placements and insurance-linked securities. The consensus mark for Reinsurance Solutions revenues is $665 million, marking a 4.7% year-over-year increase. Our estimate is $654.1 million.

Additionally, revenues of Health Solutions are likely to have received an impetus in the to-be-reported quarter, attributable to new business growth and strong performance of its core Health and Benefits business. The Zacks Consensus Estimate for Health Solutions revenues is pegged at $750 million, indicating a rise of 13.3% from the prior-year quarter’s reported number. We expect the metric to register a year-over-year rise of 22% in the second quarter.

Improved NFP asset inflows are likely to drive the results of Wealth Solutions. The consensus mark for the unit’s revenues is $550 million, which implies 18.8% growth from the prior-year quarter’s reported figure. Our estimate for the metric stands at $527.8 million.

However, the upside is expected to have been partially offset by an elevated cost level resulting from higher compensation and benefits, and information technology expenses. Our model suggests the two expense components to witness year-over-year increases of 5.9% and 6.1%, respectively. Meanwhile, we expect total operating costs of $3.2 billion in the second quarter, up 4.6% year over year. Management anticipates interest expenses of $209 million in the second quarter.

Here are some other companies from the insurance space, which according to our model, have the right combination of elements to beat on earnings this time around:

Root, Inc. ROOT has an Earnings ESP of +58.29% and a Zacks Rank of 1 at present. The Zacks Consensus Estimate for ROOT’s second-quarter earnings is pegged at $1.06 per share. A loss of 52 cents per share was incurred in the prior-year quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

Root’s earnings beat estimates in each of the trailing four quarters, the average surprise being 208.89%.

Skyward Specialty Insurance Group, Inc. SKWD currently has an Earnings ESP of +2.51% and a Zacks Rank of 2. The Zacks Consensus Estimate for SKWD’s second-quarter earnings is pegged at 86 cents per share, which implies a 7.5% rise from the year-ago quarter’s figure.

Skyward Specialty’s earnings beat estimates in each of the trailing four quarters, the average surprise being 12.86%.

Primerica, Inc. PRI has an Earnings ESP of +0.12% and a Zacks Rank of 3 at present. The Zacks Consensus Estimate for PRI’s second-quarter earnings is pegged at $5.17 per share, which implies a 9.8% rise from the year-ago quarter’s figure.

Primerica’s earnings beat estimates in each of the trailing four quarters, the average surprise being 7.83%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-10 | |

| Jul-10 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-02 | |

| Jun-24 | |

| Jun-04 | |

| Jun-03 | |

| May-28 | |

| May-28 | |

| May-19 | |

| May-18 | |

| May-15 | |

| May-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite