|

|

|

|

|||||

|

|

|

Energy drink company Celsius (NASDAQ:CELH) announced better-than-expected revenue in Q2 CY2025, with sales up 83.9% year on year to $739.3 million. Its non-GAAP profit of $0.47 per share was 93.1% above analysts’ consensus estimates.

Is now the time to buy Celsius? Find out by accessing our full research report, it’s free.

John Fieldly, Chairman and CEO of Celsius Holdings, said: “Celsius Holdings delivered strong results in the second quarter, supported by solid sales growth for the CELSIUS and Alani Nu brands and operational efficiencies across our business. As momentum builds across the energy category, our brands continue to lead - driving household penetration, expanding shelf space and outperforming expectations. We believe modern energy is one of the most exciting growth opportunities in beverages today, and Celsius Holdings is defining the category’s future. We remain focused on disciplined execution, organizational excellence and long-term growth.”

With its proprietary MetaPlus formula as the basis for key products, Celsius (NASDAQ:CELH) offers energy drinks that feature natural ingredients to help in fitness and weight management.

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

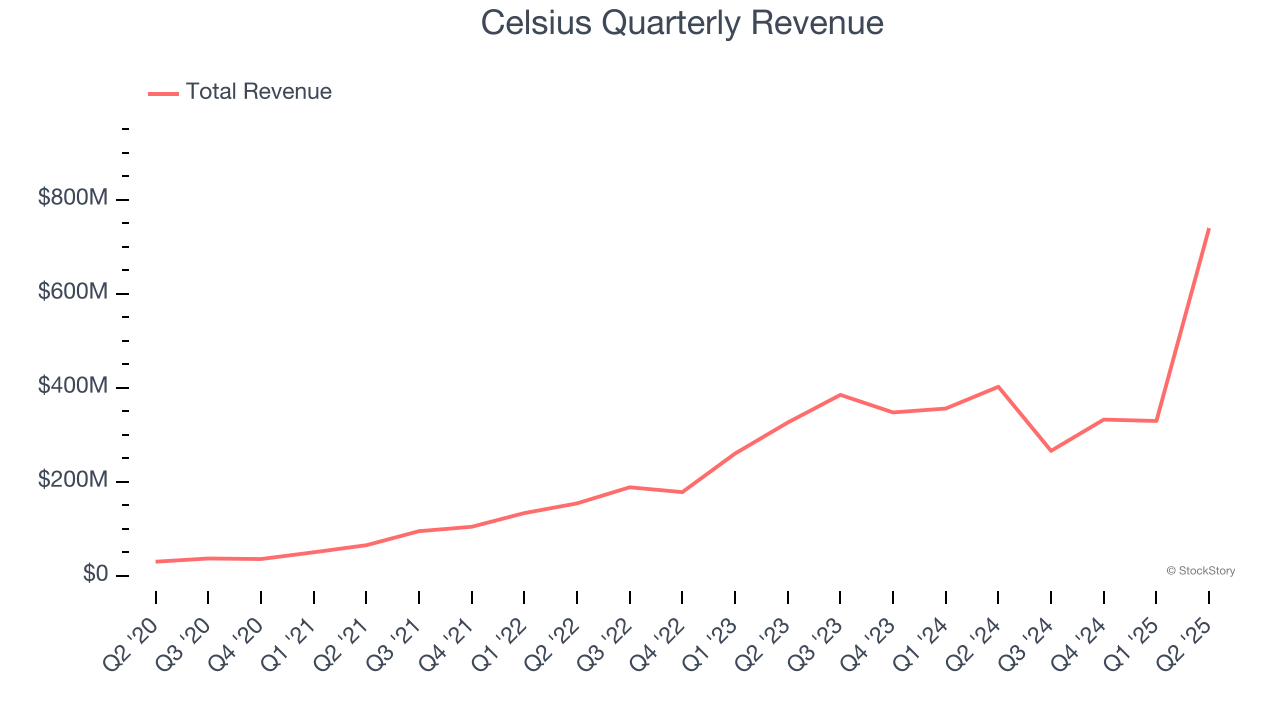

With $1.67 billion in revenue over the past 12 months, Celsius is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Celsius’s sales grew at an incredible 50.7% compounded annual growth rate over the last three years. This is a great starting point for our analysis because it shows Celsius’s demand was higher than many consumer staples companies.

This quarter, Celsius reported magnificent year-on-year revenue growth of 83.9%, and its $739.3 million of revenue beat Wall Street’s estimates by 14%.

Looking ahead, sell-side analysts expect revenue to grow 56.4% over the next 12 months, an acceleration versus the last three years. This projection is eye-popping and implies its newer products will catalyze better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

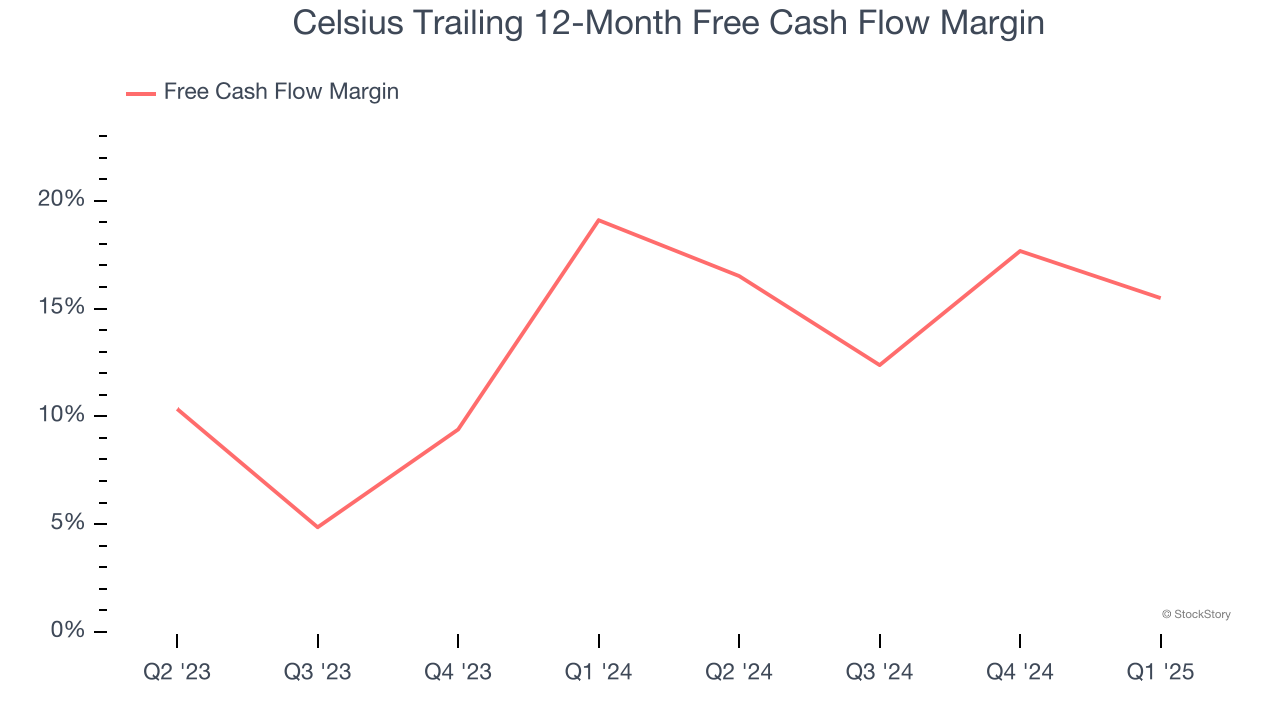

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Celsius has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 17.4% over the last two years.

We were impressed by how significantly Celsius blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. Zooming out, we think this quarter featured some important positives. The stock traded up 16.7% to $50.02 immediately following the results.

Sure, Celsius had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| 9 hours | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-08 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite