|

|

|

|

|||||

|

|

|

Shares of Honeywell International Inc. HON have been showing some decent gains of late, rising 10% in the past year. The industrial conglomerate has outperformed the industry’s growth of 2.5%. In contrast, the company’s peers, Carlisle Companies Incorporated CSL, Zebra Technologies Corporation ZBRA and MSA Safety Incorporated MSA have lost 4.5%, 0.8% and 1.5%, respectively, over the same time frame. However, it has lagged behind the S&P 500 composite’s increase of 20.5%.

Closing at $216.37 on Friday, the stock is trading below its 52-week high of $242.77 but much higher than its 52-week low of $179.36.

Honeywell is experiencing persistent strength in its commercial aviation aftermarket business, driven by solid demand in the air transport market and supply-chain improvements. In the second quarter of 2025, sales from its commercial aviation aftermarket business increased 7% year over year. Strength in its defense and space business, owing to stable U.S. and international defense spending volumes and sustained demand from the current geopolitical climate, is also proving beneficial. In the second quarter, sales from the defense and space business surged 13% year over year.

In the quarters ahead, HON expects the Aerospace Technologies segment to benefit from strong demand in commercial aviation, growth in air transport flight hours, higher shipset deliveries and strong defense spend volumes.

Solid demand for its products and solutions, led by increasing building projects, particularly in North America, Middle East and India, is expected to drive the Building Automation segment. Increasing order rates in data centers, airports and hospitality projects bode well for it.

Solid momentum in the Universal Oil Products business, driven by higher refining and petrochemicals projects, remains favorable for the Energy and Sustainability Solutions segment. Exiting the second quarter, the company’s overall backlog grew 10% year over year to $36.6 billion. For 2025, it expects overall revenues to be in the $40.8-$41.3 billion range, with organic revenues expected to be up 4-5% on a year-over-year basis.

Honeywell’s commitment to rewarding its shareholders through dividends and share buybacks is also encouraging. It paid out dividends worth $1.48 billion and repurchased shares worth $3.6 billion in the first six months of 2025. Also, in September 2024, HON hiked its quarterly dividend by approximately 5% to $1.13 per share.

The company’s ability to generate strong free cash flow supports its shareholder-friendly activities. HON expects free cash flow to be in the range of $5.4-$5.8 billion for 2025.

Softness in the productivity solutions and services business, owing to project slowdown, remains a concern for the Industrial Automation segment. In second-quarter 2025, the segment’s sales declined 5% on a year-over-year basis. For 2025, it anticipates that the Industrial Automation segment’s organic sales will decline in the low to mid-single digit range.

High long-term debt remains a major concern for Honeywell. Its long-term debt in the last five years (2020-2024) increased 9.3% (CAGR). Exiting second-quarter 2025, HON’s long-term debt was $30.2 billion, higher than $25.5 billion at 2024-end. The increase in its debt level was primarily attributable to the funds raised for acquisitions. Considering its high debt level, its cash and cash equivalents of $10.3 billion do not look impressive.

Also, interest expenses and other financial charges in second-quarter 2025 remained high at $330 million, reflecting an increase of 32% year over year. High debt levels can increase its financial obligations and prove detrimental to profitability moving ahead.

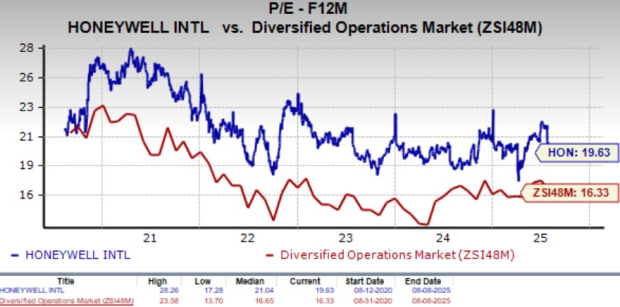

Honeywell is currently trading at a forward 12-month P/E of 19.63X, at a premium compared with the industry’s 16.33X. While its peer, Carlisle, is trading cheaper compared with HON, Zebra Technologies and MSA Safety are trading at a premium. Notably, Carlisle, Zebra Technologies and MSA Safety are currently trading at 15.69X, 19.89X and 20.65X, respectively.

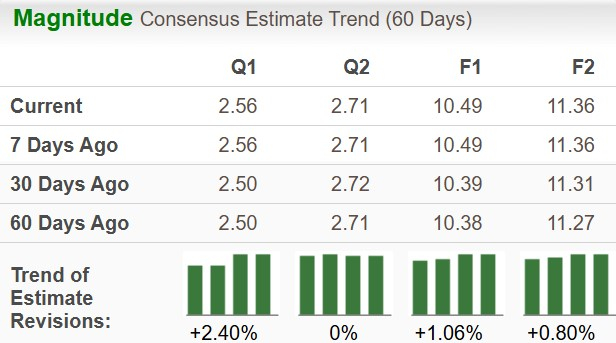

The Zacks Consensus Estimate for Honeywell’s 2025 earnings has increased 1.1% to $10.49 per share over the past 60 days, indicating year-over-year growth of 6.1%. The consensus mark for 2026 earnings increased 0.8% to $11.36 per share, indicating a year-over-year increase of 8.2%.

Despite its several upsides and impressive dividend payout trend, the near-term challenges, such as persistent weakness in the Industrial Automation unit and high debt level, are limiting this Zacks Rank #3 (Hold) company’s near-term prospects. While current shareholders should hold their positions, new investors should wait for the stock to retract some of its recent gains and provide a better entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite