|

|

|

|

|||||

|

|

|

Disney’s DIS Direct-to-Consumer (DTC) momentum is emerging as a real turning point for entertainment growth. After years of heavy investment in streaming, the company reported its third consecutive profitable quarter. In the third quarter of fiscal 2025, the DTC segment posted operating income of $346 million, a sharp reversal from a $19-million loss a year ago, driven by price increases, subscriber growth and rising ad revenues.

While the overall Entertainment operating income declined 15% year over year due to weakness in Content Sales/Licensing and Linear Networks, DTC was the bright spot. Disney’s optimism is supported by its outlook. The company projects $1.3 billion in DTC operating income for fiscal 2025, indicating a more than 800% year-over-year upsurge.

The driving force behind this momentum is clear. The price increases have led to a revenue rise, improved ad-supported tiers and steady subscriber growth, with Disney+ and Hulu now reaching 183 million subscribers. Backed by marquee sports rights, including the NFL and WWE, initiatives like merging Hulu with Disney+ and launching a standalone ESPN streaming service in the fall of 2025 are designed to drive ARPU and long-term retention.

According to Zacks models, this momentum can lead to a 14.3% return on entertainment operating income in fiscal 2025, and management is forecasting 10 million new subscriptions for the fourth quarter. These factors indicate that Disney's DTC momentum is becoming a decisive driver of revitalized and sustainable entertainment margins.

Netflix Inc. NFLX leads streaming with more than 300 million subscribers and plans to spend $18 billion in 2025 on shows, movies and live sports. The company is boosting revenues through ads, price increases and growing margins. Popular hits like Squid Game and the upcoming Stranger Things 5 keep viewers engaged. Netflix also uses AI recommendations and ad-tech to stay ahead, while expanding into gaming and live events to grow beyond scripted content.

Warner Bros. Discovery’s WBD streaming segment, anchored by Max, added 3.4 million global subscribers at the end of the second quarter of 2025, reaching 125.7 million and lifting streaming revenues 9% to $2.8 billion. WBD turned streaming profitable with $293 million in EBITDA, while studios rallied 55% on major releases. With HBO originals, Warner Bros. films and Discovery content, WBD leverages ad-supported tiers and bundling. Strong cost control and rising profitability underscore the company’s growing competitive strength in the direct-to-consumer streaming battle against rivals like Disney.

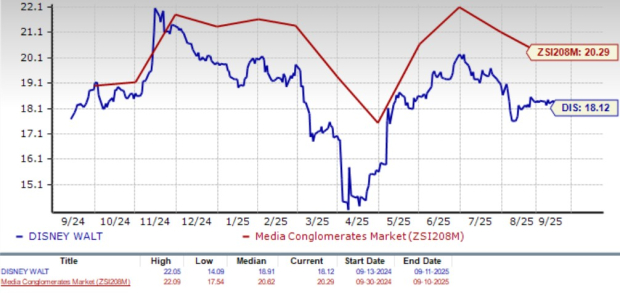

Disney shares have gained 5.2% in the year-to-date period, underperforming both the Zacks Consumer Discretionary sector’s rise of 10.9% and the Zacks Media Conglomerates industry’s growth of 10.1%.

From a valuation standpoint, the DIS stock is currently trading at a forward 12-month price/earnings ratio of 18.12X compared with the industry’s 20.29X. DIS has a Value Score of B.

The Zacks Consensus Estimate pegs Disney’s fiscal 2025 and 2026 earnings at $5.86 and $6.49 per share, witnessing upward revisions over the past 30 days. These figures suggest year-over-year growth of 17.91% in 2025 and 10.69% in 2026.

DIS currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-27 | |

| Feb-27 |

Six Months, 9 Offers and $81 Billion. How Hollywood's Nasty Takeover Was Won.

NFLX +13.77% WBD

The Wall Street Journal

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Paramount Stock Up 20% On Warner Deal; Democrats Warn Of 'Vigorous' Investigation

NFLX +13.77%

Investor's Business Daily

|

| Feb-27 | |

| Feb-27 |

Paramount Stock Up 20% On Warner Deal; Democrats Warn Of 'Vigorous' Investigation

WBD

Investor's Business Daily

|

| Feb-27 |

Paramount must convince regulators its deal with Warner will not hurt customers

NFLX +13.77%

Associated Press Finance

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite