|

|

|

|

|||||

|

|

|

GE Aerospace is what remains of General Electric after a series of spin offs.

The company makes and services jet engines.

GE Aerospace had a strong second quarter, increased its guidance, and has a huge backlog.

General Electric is a storied name on Wall Street and in the world more generally. But the company got caught up in the mortgage mess during the Great Recession, and getting back on track meant a massive corporate makeover. The GE ticker is now attached to a company called GE Aerospace (NYSE: GE). It is a very, very exciting business.

Here are three reasons to like the stock and one thing you'll need to be careful about.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

On the surface, what GE Aerospace does is build and sell jet engines. That is, of course, a very important part of its business. But it isn't actually the most important part. Indeed, every jet engine the aerospace company sells has to be maintained. And that maintenance generates service revenue for as long as the engine is still being used.

Image source: Getty Images.

Some numbers will help here. On the commercial side of the business, which sells to airlines, services account for nearly three-quarters of GE Aerospace's revenue. On the military side, services make up just over half of the company's revenue. All in, services are roughly 70% of overall revenue.

That is a recurring income stream that provides huge support to the company's earnings. And every new engine it builds and sells just increases the service revenue it reports on its income statement.

In the second quarter of 2025, GE Aerospace reported that adjusted revenue rose 23%. Adjusted earnings rose 38%. And free cash flow rose a massive 92%. It was a very good quarter.

But management has high hopes for the future, too. It increased its full-year guidance for 2025 when it released second-quarter earnings. That makes sense given the recent performance, but there was another twist here. The company also upped its outlook through 2028.

The details of the long-term guidance change are probably less important than the direction of the change. It is hard to predict what the next quarter will bring, let alone a quarter three years away. This long-term guidance improvement, however, suggests that GE Aerospace isn't just expecting a good year in 2025, but that the business is actually fundamentally stronger than management had earlier thought.

The third reason to be excited about GE Aerospace today is that it has a $175 billion backlog. This is work that the company has contracted for, but that it has yet to complete. It is, in effect, future revenue. The backlog is a mix of business, including both jet engine sales and services for existing engines. But those engine sales, as noted above, just increase the customer base for services in what is something of a positive feedback loop.

The backlog also provides a lens through which investors can view the company's long-term guidance. The 2028 outlook is at least partly built on the huge $175 billion backlog. To give some insight here, GE Aerospace generated roughly $35 billion in revenue in 2024, meaning that $175 billion represents around five years' worth of income.

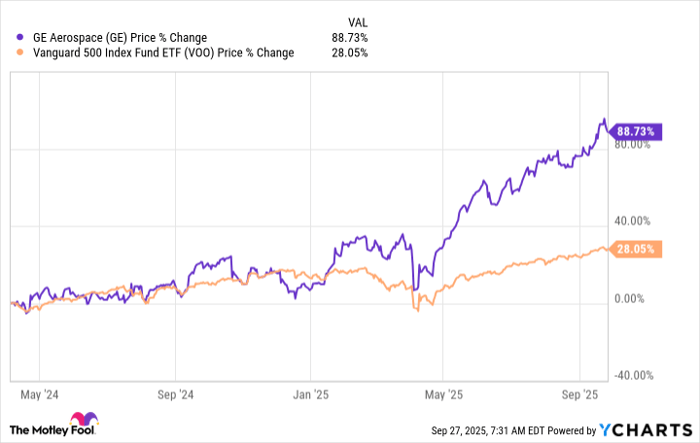

Data by YCharts.

When discussing GE Aerospace's earnings, the term adjusted was used. That's because the company, as it stands today, was created following a series of large spin-offs, the last of which took place on April 4, 2024. In other words, GE Aerospace has only existed in its current form for a relatively short period of time. That makes it kind of hard to value the company.

This is relevant because the stock price has taken off, particularly in recent months. But without a clean history on the revenue and earnings side of things, it is hard to say what traditional valuation metrics like price-to-sales and price-to-earnings should be. The current price rally could just be the market placing a more appropriate valuation on the shares after GE Aerospace became its own company.

And yet it is hard to ignore the market-beating price advance, which could also be a sign that investors have gotten a little overly excited by the company's strong financial performance. There are very, very good reasons to be excited by GE Aerospace's business and, at the same time, it may still only deserve a spot on your wishlist as Wall Street tries to figure out the right price to place on the shares.

Before you buy stock in GE Aerospace, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and GE Aerospace wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $650,607!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,114,716!*

Now, it’s worth noting Stock Advisor’s total average return is 1,068% — a market-crushing outperformance compared to 190% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends GE Aerospace. The Motley Fool has a disclosure policy.

| 22 min | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 |

Dow Jones AI Giant Nvidia Eyes Buy Point With Earnings Set To Surge 72%

GE

Investor's Business Daily

|

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite