|

|

|

|

|||||

|

|

|

Carnival posted another record quarter.

The company continues to see strong booking trends.

It has done a nice job of deleveraging, and the stock is reasonably priced.

Cruise ship operators were some of the worst-hit companies during the pandemic, being forced to shut down. But passengers have been coming back in droves in the years since cruises resumed. That was on display once again when Carnival Corp. (NYSE: CCL) (NYSE: CUK) reported its 10th straight quarter of record revenue.

Despite the strong results and guidance, the stock sank on the report, but it is still up about 15% on the year, as of this writing.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Let's dive into Carnival's most recent results to see whether now is a good time to buy the dip.

Image source: Getty Images

Carnival posted strong fiscal third-quarter results, reporting record revenue and profits. In addition, the company said booking volumes continue to strengthen, with half of 2026 already booked at historically high prices and 2027 already off to a strong start.

For the quarter, Carnival's revenue rose 3% to a record $8.15 billion. Ticket revenue climbed 4% to $5.43 billion, while onboard revenue edged up 2%.

Available lower berth days (ALBDs), a measure of capacity based on cabins holding two passengers, fell 2% to 24.6 million. Occupancy, meanwhile, remained at 112%. Occupancy is based on two passengers per cabin, so it can exceed 100%. The company had less available capacity than a year ago and fewer passengers, but strong pricing powered revenue growth.

Net yields, which measure revenue minus variable costs (such as commissions, transportation, etc.) per ALBD, jumped 5% to $249.11. Its gross margin per ALBD rose to $124.20. These metrics show that the company is seeing better margins and profitability per cabin.

Additionally, these metrics helped the company produce record net income and adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) in the quarter. Adjusted net income climbed 10% to $2 billion, while adjusted EBITDA jumped 7% to $3 billion. Adjusted earnings per share (EPS) climbed 13% to $1.43.

Carnival has generated about $4.7 billion in operating cash flow so far this year, and $2.6 billion is free cash flow. The latter is a big improvement compared to a year ago, when it was spending more on capital expenditures (capex) to build new ships. It had one new ship delivered this year and has none set for next year. The company expects to add one to two new ships a year going forward.

The combination of free cash flow and strong profitability helped the company reduce its leverage (net debt/adjusted EBITDA) to an expected 3.6 times by year-end 2025. That would be a huge improvement from the 6.7 times leverage it carried at the end of fiscal 2023.

Looking ahead, Carnival is projecting fiscal Q4 adjusted net income to surge 60% to $300 million. It expects net yields to rise by 6.4%, or 4.3% in constant currency.

The company once again raised its full-year guidance across the board, as seen in the table below.

| December Guidance | March Guidance | June Guidance | September Guidance | |

|---|---|---|---|---|

| Net yield growth | 4.2% | 4.7% | 5% | 5.3% |

| Adjusted EBIDTA | $6.6 billion | $6.7 billion | $6.9 billion | $7.1 billion |

| Adjusted EPS | $1.70 | $1.83 | $1.97 | $2.14 |

Source: Carnival. EBITDA = earnings before interest, taxes, depreciation, and amortization. EPS = earnings per share.

One of the biggest issues facing Carnival coming out of the pandemic lockdown was that it left the company burdened with debt and highly leveraged. Management has done a great job of not only growing revenue and profitability but also lowering leverage to a more reasonable amount.

Now, given that the cruising market could always turn if the economy weakens, I'd still like to see the company continue to lower its debt. But overall, it's taking a nice, disciplined approach to adding new ships while benefiting from strong occupancy and high prices. It's also been able to boost its credit rating and refinance to lower-cost debt, helping lower its interest expense.

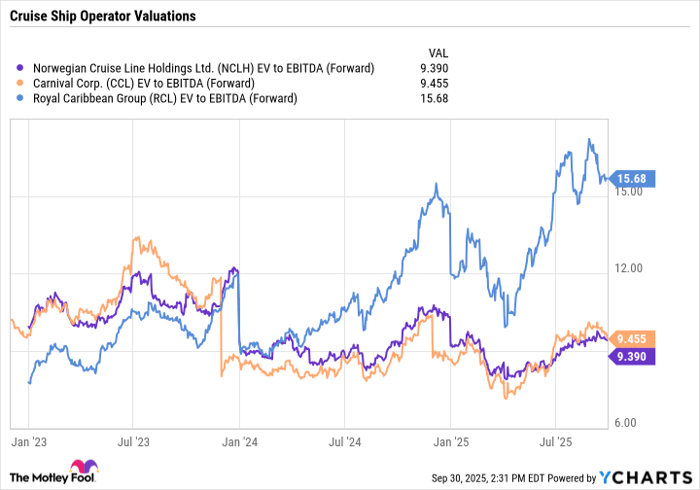

From a valuation perspective, the company trades at a forward enterprise value (EV)-to-EBITDA multiple of about 9.5. Given the debt and depreciation associated with the industry, I prefer using this valuation metric when looking at cruise ship stock, and its valuation is right in line with rival Norwegian Cruise Line and at a discount to Royal Caribbean.

NCLH EV to EBITDA (Forward) data by YCharts. EV = enterprise value. EBITDA = earnings before interest, taxes, depreciation, and amortization.

Overall, I think Carnival has solid upside potential from here, given the industry trends, its strong bookings, and its ability to continue deleveraging. Meanwhile, its valuation is reasonable and has the potential to possibly expand moderately. However, it's a cyclical stock that could come under pressure during a recession, so just be aware of economic trends.

Before you buy stock in Carnival Corp., consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Carnival Corp. wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $646,567!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,143,710!*

Now, it’s worth noting Stock Advisor’s total average return is 1,072% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool recommends Carnival Corp. The Motley Fool has a disclosure policy.

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite