|

|

|

|

|||||

|

|

|

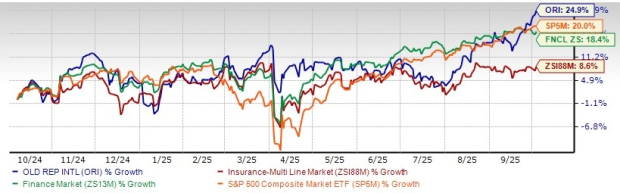

Shares of Old Republic International Corporation ORI have gained 24.9% in the past year, outperforming its industry, the Finance sector and the Zacks S&P 500 composite’s growth of 8.6%, 18.4% and 20%, respectively.

ORI has outperformed its peers, Assurant, Inc. AIZ, Radian Group Inc. RDN and EverQuote, Inc. EVER, which have risen 17.9%, 2.2% and 12.8%, respectively, in the past year.

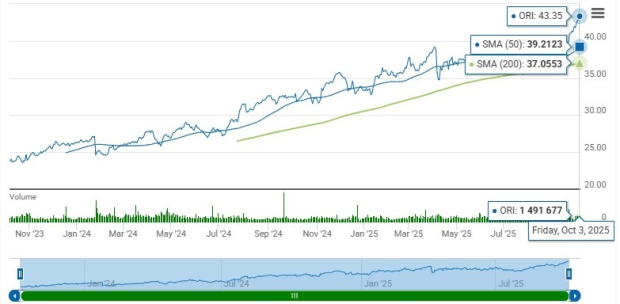

Shares of Old Republic International closed at $43.35 on Friday and hit a 52-week high of $43.56.

With a market capitalization of $10.77 billion, the average number of shares traded in the last three months was 1.4 million.

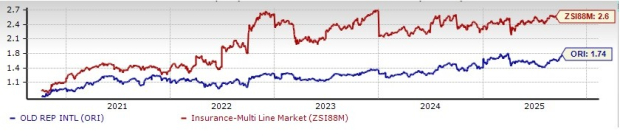

The stock is trading at a discount to the industry. Its price-to-book value of 1.74X is lower than the industry average of 2.6X, the Finance sector’s 4.34X, and the Zacks S&P 500 Composite’s 8.8X.

The company has a Value Score of B. This style score helps find the most attractive value stocks.

Shares of Old Republic International are trading above the 50-day and 200-day simple moving averages (SMA) of $39.37 and $37.65, respectively, indicating solid upward momentum. SMA is a widely used technical analysis tool to predict future price trends by analyzing historical price data.

The Zacks Consensus Estimate for Old Republic International’s 2025 earnings per share indicates a year-over-year increase of 7.2%. The consensus estimate for revenues is pegged at $8.86 billion, implying a year-over-year improvement of 8.5%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 4.6% and 6.1%, respectively, from the corresponding 2024 estimates.

The insurer has a solid track record of beating earnings estimates in each of the last four quarters, with an average of 34.73%.

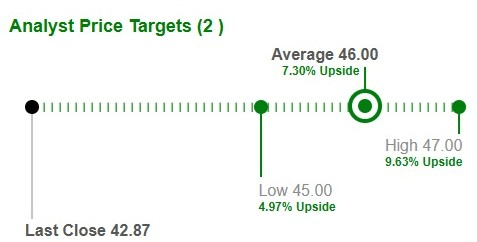

Based on short-term price targets offered by two analysts, the Zacks average price target is $46 per share. The average suggests a potential 7.3% upside from the last closing price.

Return on equity (ROE) for the trailing 12 months was 20.9%, which compared favorably with the industry’s 14.8%. This reflects its efficiency in utilizing shareholders’ funds. ORI’s ROE has been increasing over the last few quarters.

Also, return on invested capital (ROIC) has been increasing over the last few quarters as the company raised its capital investment over the same time frame. This reflects ORI’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 6.2%, better than the industry average of 1.9%.

ORI has a diverse and decentralized portfolio of specialty insurance products and services.

ORI’s General Insurance segment should continue to benefit from segmentation, better risk selection, meticulous pricing and increased use of analytics. This, in turn, has helped deliver a combined ratio below 96 for 14 years. The insurer aims for a combined ratio between 90 and 95.

The Title business, meanwhile, should continue to benefit from an expanding presence in the commercial real estate market.

For long-term growth, the insurer continues to invest in new general insurance specialty underwriting subsidiaries and technology for both general insurance and title insurance. The insurer writes less catastrophe-exposed business than most of its peers, safeguarding its combined ratio to some extent.

ORI’s dividend history is impressive. It has hiked dividends for the last 43 years. Its dividend yield of 3.1% appears attractive compared with the industry average of 2.5%, making it an attractive pick for yield-seeking investors. The insurer also engages in regular buybacks.

However, a high debt level, an increase in interest expense and a lower asset base in a low-interest rate environment keep us cautious about this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite