|

|

|

|

|||||

|

|

|

Costco Wholesale Corporation COST released its fourth-quarter fiscal 2025 results on Sept. 25, after the closing bell, drawing fresh attention from investors tracking the retail sector’s performance. Given its stable growth and loyal membership base, Costco has historically weathered economic hiccups better than many competitors. Now that its latest earnings are out, investors are contemplating whether to increase their stake, hold tight to their current investments or sell off shares in response to new data and market trends.

Shares of Costco have fallen 3.4% since the release of its fourth-quarter fiscal 2025 earnings, reflecting investor caution over the top-line miss. Nonetheless, both revenues and earnings improved year over year, driven by robust membership growth, resilient traffic, double-digit e-commerce gains and margin expansion. (Read: Costco Q4 Earnings Top Estimates, Comparable Sales Rise 5.7%)

The company's ability to generate strong comparable sales across regions highlights its effective pricing strategy and member loyalty. Comparable sales, excluding gasoline prices and foreign exchange impacts, rose 6.4%. In the United States, comparable sales increased 6%, while Canada and Other International markets saw gains of 8.3% and 7.2%, respectively.

Costco ended the quarter with 81 million paid members, up 6.3% from the prior year. Executive memberships, a more profitable category for Costco, grew 9.3% year over year to reach 38.7 million, now accounting for 47.7% of all paid members and driving 74.2% of worldwide sales. The company's commitment to value and quality has fostered strong loyalty among members.

Over the past 30 days, the Zacks Consensus Estimate for the current fiscal year has moved up by 16 cents to $20.01, while the estimate for the next fiscal year has declined by 3 cents to $21.86. These estimates indicate expected year-over-year growth rates of 11.2% and 9.3%, respectively.

Costco’s resilient business model, centered around a membership-based structure, continues to be a major growth driver. The company’s high membership renewal rates, coupled with its efficient supply chain management and bulk purchasing power, ensure competitive pricing. The renewal rate remained healthy at 92.3% in the United States and Canada and 89.8% worldwide.

Members pay an annual fee for access to Costco's warehouses, where they can purchase goods at significant discounts. This model not only ensures a steady inflow of revenues but also creates a sense of exclusivity and value among its members. Membership fee income rose 14% year over year to $1,724 million in the fourth quarter of fiscal 2025. About less than half of the quarterly growth in membership fee income came from the fee increases introduced last September in the United States and Canada.

Costco’s ability to evolve with changing consumer preferences has also played a vital role in its expansion. The company adjusts its product mix to include both everyday essentials and unique, high-demand items — a strategy that strengthens its appeal across diverse customer segments. Through data-driven market analysis and an adaptable merchandising approach, Costco has steadily expanded its presence in both domestic and international markets.

Digital acceleration and logistics investments are monetizing Costco’s assortment and big-ticket capability. E-commerce performance was strong, with comparable sales rising 13.6% year over year, or 13.5%, after excluding the impact of gasoline prices and currency fluctuations. E-commerce site traffic was up 27%, and Costco Logistics deliveries rose 13% in the quarter. Management also highlighted that “digitally enabled” sales (a broader measure that will be reported going forward) totaled more than $27 billion in fiscal 2025.

This robust operational performance translated into strong financial results. Costco generated $13,335 million of operating cash flow in fiscal 2025 and concluded the year with $14,161 million in cash and equivalents. Management invested nearly $5,498 million in capital expenditures during the fiscal year and signaled that fiscal 2026 capex would grow modestly above last year to support 35 planned openings.

Costco's impressive sales figures are part of a larger retail picture where competition is intensifying. Rivals like Ross Stores, Inc. ROST, Dollar General Corporation DG and Target Corporation TGT are investing in expanding their capabilities and enhancing customer experience.

Moreover, margins remain a critical area to monitor, with potential concerns stemming from any deleverage in the selling, general and administrative rate. Additionally, foreign exchange volatility and potential tariffs on key imports create uncertainty.

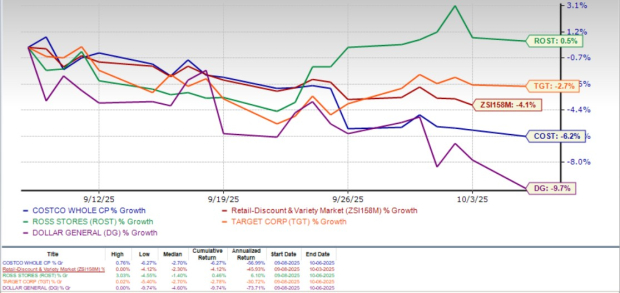

Costco stock has fallen 6.2% over the past month, underperforming the industry’s decline of 4.1%. A sneak peek into key retail peers' performance reveals that shares of Ross Stores have risen marginally by 0.5% during the said time frame, while Target and Dollar General have declined 2.7% and 9.7%, respectively.

However, the stock is trading at a significant premium to its peers. Costco's forward 12-month price-to-earnings ratio stands at 45.11, higher than the industry’s ratio of 29.45 and the S&P 500's 23.65. Costco is trading at a premium to Target (with a forward 12-month P/E ratio of 11.24), Ross Stores (22.90) and Dollar General (15.13).

While Costco continues to trade at a notable premium to its peers, reflecting investor confidence in its strong brand image, loyal membership base and long-term growth potential, the stock’s recent underperformance relative to the industry highlights some caution. With such a high valuation, even minor setbacks could trigger a pullback in the stock.

Costco remains one of the most dependable names, supported by its steady membership growth, operational efficiency and disciplined expansion. However, with the stock already priced quite high, there may not be much room for short-term gains unless growth stays strong. For existing investors, holding the stock makes sense, given its long-term strength and resilience, while potential investors may want to wait for a more attractive entry point before buying in. Costco currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 6 hours | |

| 6 hours | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite