|

|

|

|

|||||

|

|

|

UPS stock is hovering around multi-year lows.

A dividend cut would help UPS support its payout with free cash flow and improve its investment thesis.

Difficult end-market conditions have disrupted UPS' plans.

United Parcel Services (NYSE: UPS) has been getting a lot of attention as one of the three highest-yielding stocks in the S&P 500 (SNPINDEX: ^GSPC), along with chemical giant LyondellBasell Industries and consumer packaged food company Conagra Brands. But the yields of these companies have been going up because of falling stock prices.

UPS' dividend yield is hovering around an all-time high of 7.6%, as the stock price is down 31.3% year to date and 47.7% in three years.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

These two Fool.com contributors discuss the state of UPS' turnaround, what's going right and what's going wrong, and why some investors may want to buy the high-yield dividend stock, whereas others may prefer holding off.

Image source: Getty Images.

Daniel Foelber: One glance at UPS' stock price, and it's easy to lose hope that the company will turn around.

UPS overexpanded its network during the pandemic shutdowns, anticipating sustained growth in the package delivery market, particularly for business-to-consumer small packages. That didn't happen, as consumers shifted spending toward services. Then came inflation and cost-of-living challenges, which are straining consumer spending on discretionary goods.

The glass-half-full outlook on UPS centers around the belief that the company's focus on higher-margin deliveries will pay off over the long term. UPS is cutting its package delivery volumes with Amazon (NASDAQ: AMZN) -- its largest customer -- by 50% by June 2026. The move should result in lower revenue and higher margins, providing a better foundation for returning to growth. But in the near term, UPS' results continue to disappoint.

The good news is that declines seem to have stabilized. In its second-quarter 2025 earnings release, UPS did not provide revenue or operating profit guidance, but it did confirm $3.5 billion in expected expense reductions. These expenses, under its network reconfiguration and Efficiency Reimagined initiatives, are partially related to reducing Amazon delivery volumes. So investors shouldn't expect these cuts to boost earnings considerably, but rather to reposition its network to function without Amazon.

For full-year 2025, UPS is guiding for $1 billion in buybacks (already completed) and $5.5 billion in dividend payments. Having paid $2.7 billion in dividends in the first half of 2025, UPS is indicating that it doesn't plan to cut its payout.

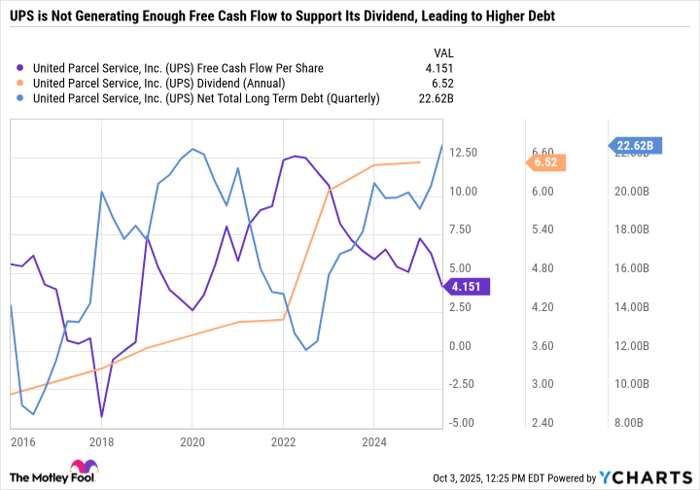

Although I'm optimistic about UPS' cost-cutting efforts and decision to reduce its dependence on Amazon to boost margins, I'm less confident about the sustainability of its dividend. UPS simply doesn't have $6.5 billion lying around to pass along to shareholders through buybacks and dividends. In its latest quarter, it only generated $742 million in free cash flow (FCF) -- which was about half of what was needed to cover its dividend.

UPS Free Cash Flow Per Share data by YCharts.

UPS has a high yield because it boosted its dividend considerably in 2022, when its FCF was much higher. The move was reasonable at the time, when UPS was raking in over $12 in FCF per share. However, FCF has nosedived and is insufficient to cover the dividend, which has taken a toll on UPS' balance sheet.

Investors buying UPS should do so as a turnaround play rather than an ultra-high-yield stock. If I had to guess, I would expect UPS to cut its dividend by 50%, or maybe by two-thirds, before the end of 2026. So, when considering UPS, I'm mentally penciling in a yield of more like 2.5% to 3.8%, rather than the 7.6% it currently yields. That way, the dividend is supported by FCF.

Lee Samaha: UPS management isn't responsible for external market conditions, but it is responsible for how it adjusts to them, and particularly so when its internal forecasting proves inaccurate. Barring a miracle, this will be the third consecutive year that UPS has missed management's guidance, given at the start of the year.

Again, this is not to be too critical of management. It wasn't easy to predict how the economy would react coming out of the lockdown periods (where demand for deliveries boomed). It's also not easy to forecast interest rates or the Trump administration's tariff actions -- both of which have negatively affected UPS in recent times.

However, what does deserve introspection is a failure to adjust. Spending $1 billion on share buybacks in the first half (all of which would have been made at a substantially higher price than the current price) is questionable, at the very least.

Moreover, continuing to commit to a dividend costing $5.5 billion, when Wall Street analysts are now forecasting free cash flow of just $4.6 billion in 2025, $5.4 billion in 2026, and $5.1 billion in 2027, implies that UPS will need to borrow money to pay the dividend. If that seems far-fetched, consider that UPS CEO Carol Tome told investors that she had conversations with CFO Brian Dykes regarding debt financing for the dividend, as the yield is higher than the "after-tax cost of the debt."

To be clear, UPS does have good long-term growth prospects. The reduction in low or negative-margin Amazon deliveries makes sense, as does focusing on healthcare and small and medium-sized businesses (SMBs), while investing in productivity-enhancing technology.

Still, with no revenue or operating profit guidance in place for 2025 (management declined to do so in the second-quarter presentation), it's clear that there needs to be a reset of expectations, including its capital allocation policy, before investors can feel completely comfortable buying in here.

Before you buy stock in United Parcel Service, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and United Parcel Service wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $657,979!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,122,746!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 187% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 7, 2025

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and United Parcel Service. The Motley Fool has a disclosure policy.

| 59 min | |

| 1 hour | |

| 2 hours |

AI Stocks Reset In 2026 Amid Software Reckoning, Hyperscaler Capex Boom

AMZN

Investor's Business Daily

|

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 8 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite