|

|

|

|

|||||

|

|

|

Netflix NFLX is slated to report third-quarter 2025 results on Oct. 21.

For the third quarter, Netflix projects revenues of $11.526 billion, suggesting year-over-year growth of approximately 17% on both a reported and foreign exchange neutral basis. This revenue growth is expected to be driven by continued expansion in members, pricing adjustments, and increasing advertising revenues.

The Zacks Consensus Estimate for third-quarter revenues is pegged at $11.52 billion, indicating growth of 17.3% year over year.

The company provided specific earnings guidance, projecting diluted earnings per share of $6.87 for third-quarter 2025, with expected operating income of $3.625 billion and net income of $2.979 billion for the quarter.

The consensus mark for earnings is pegged at $6.89 per share, currently above the company’s expectations. The estimate has remained unchanged over the past 30 days.

In the last reported quarter, the company delivered an earnings surprise of 1.7%. The company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 6.41%.

Netflix, Inc. price-eps-surprise | Netflix, Inc. Quote

Our proven model does not predict an earnings beat for Netflix this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

NFLX has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The company forecasted an operating margin of 31% for the third quarter, which would represent a 2 percentage point improvement compared to third-quarter 2024. Netflix noted that, similar to past years, the operating margin in the second half of 2025 would be lower than in the first half due to higher content amortization and increased sales and marketing costs associated with their larger second-half programming slate. This structural pressure on profitability, despite revenue growth, raises questions about sustainable margin expansion.

The content slate delivered significant engagement drivers during the quarter. Squid Game Season 3, which premiered on June 27, generated a record-breaking 60.1 million views in its first three days and maintained its position as a cultural phenomenon throughout the period. KPop Demon Hunters emerged as an unexpected breakout success, becoming Netflix's most-watched animated original film and subsequently the platform's most popular film of all time with more than 236 million views by late August. Wednesday Season 2 launched in a strategic two-part release, with Part 1 debuting on Aug. 6 and Part 2 concluding on Sept. 3, featuring a high-profile guest appearance by Lady Gaga that generated significant social media buzz and viewership. This staggered release strategy kept the series in the cultural conversation throughout the quarter and extended its impact on subscriber metrics.

The company also highlighted its continued expansion of live programming with two marquee boxing matches in the third quarter, including the Taylor vs. Serrano rematch and the Canelo vs. Crawford fight.

Regarding the advertising business, Netflix indicated that its U.S. upfront negotiations were nearly complete, with the vast majority of deals closed with major agencies. They are expected to have been consistent with the company's goal to roughly double advertising revenues in 2025. The company completed the rollout of the Netflix Ads Suite, its proprietary first-party ad tech platform, across all advertising markets, with early results likely to be in line with expectations.

Given these dynamics, existing shareholders appear well-positioned to maintain holdings given Netflix's expanding monetization capabilities and durable competitive advantages against other streaming giants, including Apple AAPL, Amazon AMZN and Disney DIS. However, prospective investors face a more challenging risk-reward proposition. The combination of premium valuations, near-term margin pressure, and execution risks associated with the advertising buildout suggested waiting for a more attractive entry point represented the prudent course. A pullback following earnings or broader market volatility could provide better opportunities to establish positions in this streaming leader.

The consensus mark for third-quarter 2025 Asia-Pacific revenues is pegged at $1.39 billion, indicating 23.9% growth from the figure reported in the year-ago quarter.

The Zacks Consensus Estimate for Latin America revenues is pegged at $1.45 billion, suggesting a rise of 17.3% from the figure reported in the previous quarter.

Moreover, the consensus mark for EMEA revenues is pegged at $3.68 billion, suggesting an increase of 17.5% from the figure reported in the year-ago quarter.

The Zacks Consensus Estimate for the United States and Canada revenues is pegged at $4.99 billion, indicating a 15.5% rise from the figure reported in the year-ago quarter.

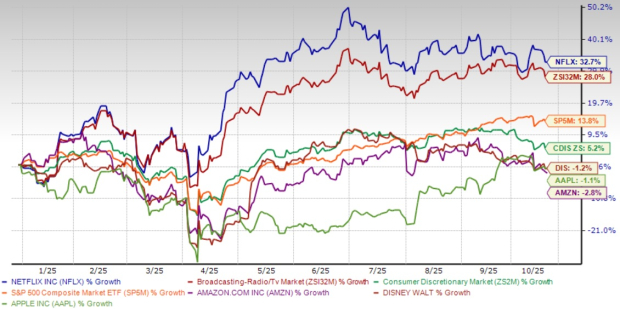

Shares of Netflix have gained 32.7% in the year-to-date period compared with the Zacks Consumer Discretionary sector’s growth of 28%. Amazon, Apple and Disney’s shares have plunged 2.8%, 1.1% and 1.2%, respectively in the same time frame.

Now, let’s look at the value Netflix offers investors at current levels. Currently, NFLX is trading at 38.18X forward 12-month earnings, above its five-year median of 33.8X. Meanwhile, the Zacks Broadcast Radio and Television industry’s forward earnings multiple sits at 29.92X. The company’s valuation looks somewhat stretched compared with its range and the industry average.

Netflix's third-quarter 2025 guidance projects solid fundamentals with 17% revenue growth to $11.5 billion and improved 31% operating margins, supported by membership expansion and doubling advertising revenues. However, the premium valuation and intensifying streaming competition warrant caution. While management has raised full-year targets to $44.8-$45.2 billion in revenues and 29.5% margins demonstrate operational strength, much of the upside reflects favorable foreign exchange movements rather than organic momentum. The second-half content slate appears robust, yet execution risks remain amid increasing content costs. Patience may reward investors seeking better risk-reward dynamics.

Netflix demonstrates strong operational execution with robust third-quarter guidance and improving margins, yet the premium valuation and competitive streaming landscape suggest limited near-term upside. Existing shareholders should maintain positions given solid fundamentals, but prospective investors would benefit from waiting for a more favorable entry point or stronger confirmation of sustained growth momentum beyond third-quarter results.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour |

Iran Says Khamenei Killed As U.S.-Israeli Attacks Continue; Dow Jones Futures Loom

AAPL

Investor's Business Daily

|

| 2 hours | |

| 3 hours |

Trump Says Khamenei Killed In U.S.-Israeli Attacks. How Will Dow Jones Futures React?

AAPL

Investor's Business Daily

|

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours |

Trump Says Khamenei Likely Killed In U.S.-Israeli Attacks On Iran. How Will Dow Jones Futures React?

AAPL

Investor's Business Daily

|

| 7 hours | |

| 8 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 13 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite