|

|

|

|

|||||

|

|

|

United Parcel Service UPS is scheduled to report its third-quarter 2025 results on Oct. 28, 2025.

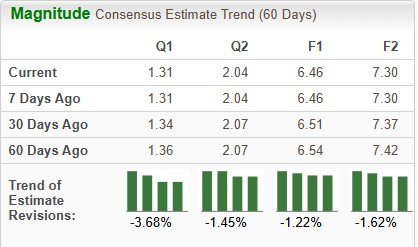

The Zacks Consensus Estimate for the September-quarter earnings is pegged at $1.31 per share, implying a 25.6% decrease from the year-ago quarter’s reported number. The estimate has been revised downward by 5 cents per share over the past 60 days.

The Zacks Consensus Estimate for revenues is pegged at $20.84 billion, indicating a decline of 6.3% from the year-ago quarter’s actuals.

UPS has an impressive earnings surprise history, as reflected in the chart below.

Given this backdrop, let us examine the factors likely to influence UPS’ third-quarter results.

Shipping volumes at UPS are likely to have been hurt by geopolitical uncertainties and high inflation. Uncertainty over tariffs, supply-chain instability and other broader macroeconomic headwinds are likely to hurt results. We believe that more than the financial numbers, it is the guidance that investors will more closely watch.

Labor costs are likely to have been high, hurting United Parcel Service’s bottom-line performance in the September quarter. Faced with these headwinds, the company has been focusing on cutting costs. As part of this exercise, UPS is offering buyouts to delivery drivers for the first time in its 117-year history. UPS’ full-time drivers are eligible for this offer. We expect an update on the same on the conference call.

Apart from the tariff-induced economic uncertainties, UPS’ decision to reduce business with its largest customer, Amazon AMZN, contributed to the decision to trim the workforce. UPS’ management has reached an agreement in principle with Amazon to lower the latter’s volume by more than 50% by June 2026. According to Carol Tome, UPS’ chief executive officer, Amazon was not its most profitable customer.

The De Minimis exemption had expired on Aug. 29. The trade exemption allowed packages containing goods valued at less than $800 to enter the United States without additional taxes. In July, President Trump signed the executive order to eliminate the exemption. Per a recent NBC News report, the accumulation of packages in UPS warehouses has compelled it to discard some shipments due to severe customs bottlenecks.

UPS has been facing customer backlash with allegations that it has been discarding certain international shipments before they reach their intended destinations. An update on that front is also expected on the third-quarter conference call.

Low fuel costs are expected to have aided UPS’ bottom-line performance in the September-end quarter. We expect expenses on fuel to decrease 7.6% from the third-quarter 2024 actuals. Tariff concerns, weakening consumer confidence and production increase by OPEC+ have all contributed to this downward pressure on crude oil.

Our proven model does not conclusively predict an earnings beat for UPS this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat, which is not the case here.

The company's Earnings ESP is -1.04%. This is because the Most Accurate Estimate is currently pegged at $1.29 per share, 2 cents below the Zacks Consensus Estimate.

UPS currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

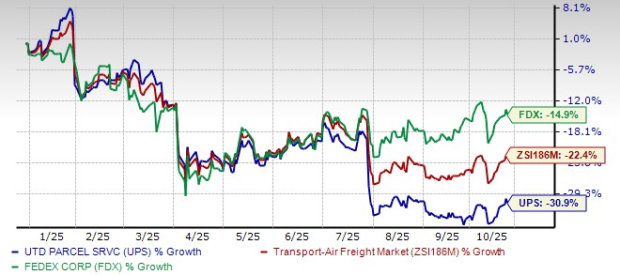

Shares of UPS have plunged in excess of 30% so far this year compared with the Zacks Transportation—Air Freight and Cargo industry’s 22.4% decline. Rival FedEx's FDX price performance is better than that of UPS.

On the basis of the forward 12-month Price/Sales (P/S), UPS’ shares are trading at a discount compared with the industry average. Rival FedEx is cheaper. FedEx currently has a Value Score of A, like UPS.

Due to the decline in shipping demand, volumes at UPS have suffered. A slowdown in online sales in the United States, apart from a softness in global manufacturing activity, has been hurting the demand scenario.

Moreover, the recent failure of the Estafeta deal represents a setback to UPS’ expansion efforts. UPS cited the inability to satisfy all closing conditions as the reason for the cancellation. The deal was announced in 2024, as a part of UPS’ “Better and Bolder” strategy to become the world's premium international small package and logistics provider.

Concerns over the sustainability of UPS’ dividends in this era of demand weakness represent a further challenge for this parcel delivery company. However, UPS’ expansion efforts look good.

It is worth noting that the company has the brand and the network to continue generating steady cash flows in the long run. This makes UPS a compelling long-term player in the transportation space. However, the near-term headwinds, including the tariff-induced uncertainties, are hard to ignore. The combination of its weak current performance and an uncertain future casts a shadow over UPS’ prospects.

Though the company has a solid track record of beating earnings estimates, it will be prudent for investors to stay away from investing in the stock for now and wait for the upcoming quarterly results to get more clarity on near-term prospects.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 min |

FedEx says it will return to customers any refunds it gets back from Trump's illegal tariffs

FDX

Associated Press Finance

|

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite