|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

The sky-high addressable opportunity presented by artificial intelligence (AI) has sent shares of Palantir Technologies and Nvidia soaring by 2,870% and 1,260%, respectively, since 2023 began.

Despite handily surpassing Wall Street's consensus third-quarter sales forecast, Palantir stock tumbled by 8% -- and there's a good reason why.

The world's largest publicly traded company will have a difficult time justifying its valuation when it lifts the hood on its fiscal third-quarter results in less than two weeks.

Over the last three years, nothing has captivated the attention and pocketbooks of investors quite like the evolution of artificial intelligence (AI). The capacity for software and systems to make split-second decisions without human intervention, and to potentially grow more efficient at their assigned tasks over time, is a game-change for most industries.

The pie-in-the-sky addressable market for AI -- $15.7 trillion by 2030, according to a report from PwC -- has sent shares of AI data-mining specialist Palantir Technologies (NASDAQ: PLTR) and graphics processing unit (GPU) kingpin Nvidia (NASDAQ: NVDA) soaring. Since the end of 2022, Palantir shares have skyrocketed 2,870%, while Nvidia stock has rallied 1,260% and crested the $5 trillion market cap plateau.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

While it's plainly evident that professional and everyday investors are excited about the growth potential and real-world utility of AI, Palantir's latest operating results revealed an undeniable weakness for Wall Street's AI darlings that should become apparent when Nvidia unveils its quarterly operating results on Nov. 19.

Make no mistake about it, Palantir's stock has gone parabolic for a reason. It's a company with well-defined competitive advantages that's made a recent habit of leaping over the consensus revenue and profit expectations of Wall Street analysts.

The true beauty of Palantir's operating model is that no large-scale competitors for its two core operating systems (Gotham and Foundry) exist.

Gotham is the company's breadwinner, at the moment. It's a cloud-based, AI-driven, software-as-a-service platform that helps the U.S. military and its allies plan and oversee missions, as well as collect and analyze data. Palantir typically secures four- or five-year contracts from federal governments, which have sustained double-digit sales growth, pushed the company into recurring profitability, and has made forecasting its operating cash flow highly predictable.

The other core segment is Foundry, which is a subscription service that helps businesses make sense of their data. It can streamline their operations by improving manufacturing efficiency, tightening up supply chains, and automating certain tasks.

The lack of large-scale competition was evident for Palantir during the September-ended quarter. Its $1.18 billion in quarterly sales topped expectations by a cool $90 million. The company also guided for $1.33 billion in fourth-quarter revenue, which was $140 million above the consensus.

But on Nov. 4, the day after Palantir unveiled its operating results following the closing bell, shares of the company tumbled more than $16, or close to 8%. In terms of market cap, we're talking about a loss of $39 billion.

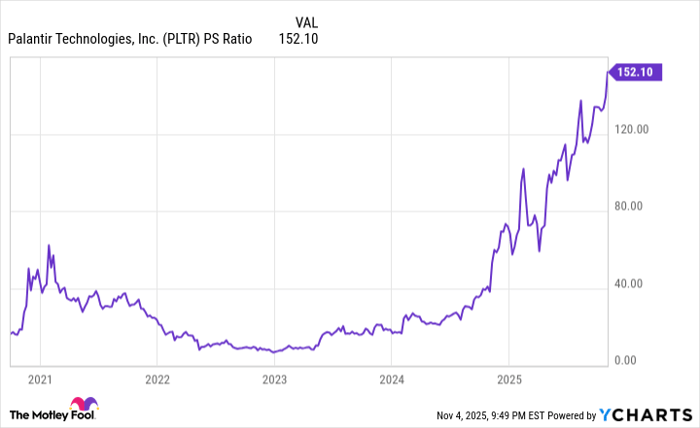

PLTR PS Ratio data by YCharts. PS Ratio = price-to-sales ratio.

What this sizable move lower in Palantir stock showed was that no earnings or revenue beat would have been sufficient to justify its premium valuation.

As of the closing bell on Nov. 3 (i.e., in the minutes leading up to Palantir's earnings release), shares of the company were valued at a price-to-sales (P/S) ratio of 152! To put this figure into perspective, the internet companies leading the charge prior to the dot-com bubble bursting in early 2000 peaked at P/S ratios ranging from 31 to 43. Consistently, this range has served as a ceiling for hyped megacap stocks on the cutting edge of a next-big-thing trend. Palantir entered its earnings report at four to five times this historical ceiling.

Whereas Wall Street analysts are known for setting the bar conservatively when establishing sales and profit expectations, there was simply no beat that would have justified Palantir's P/S ratio.

Image source: Nvidia.

However, an outlandish valuation isn't an issue exclusive to Palantir. It's a problem that's somewhat pervasive among AI stocks, including the stock market's largest publicly traded company, Nvidia.

Similar to Palantir, Nvidia's well-defined competitive advantages have lifted its valuation to new heights. Though estimates are all over the board, some analysts view Nvidia's share of GPUs deployed in AI-accelerated data centers at 90% or above. Demand for Nvidia's three generations of AI chips (Hopper, Blackwell, and Blackwell Ultra) have been backlogged.

Nvidia CEO Jensen Huang is ensuring that his company won't cede its spot at the head of the AI hardware table anytime soon. He's overseeing the development and launch of a new advanced GPU on an annual basis. Following the ramp up of Blackwell Ultra is Vera Rubin and Vera Rubin Ultra, which should make their commercial debuts in the latter-halves of 2026 and 2027. None of Nvidia's external competitors have been particularly close to matching the compute capabilities of Hopper, Blackwell, or Blackwell Ultra.

The other core advantage of Nvidia is its CUDA software platform, which is the toolkit developers use to maximize the compute capabilities of their AI-GPUs, as well as to build and train large language models. CUDA is sort of an unsung hero for Nvidia in that it keeps customers loyal to the company's ecosystem of products and services.

When Nvidia reports is fiscal third-quarter operating results after the closing bell on Nov. 19, there's a very good probability it's going to handily surpass Wall Street's expectations. But similar to Palantir, I wouldn't expect this beat to be anywhere near enough to justify its current valuation.

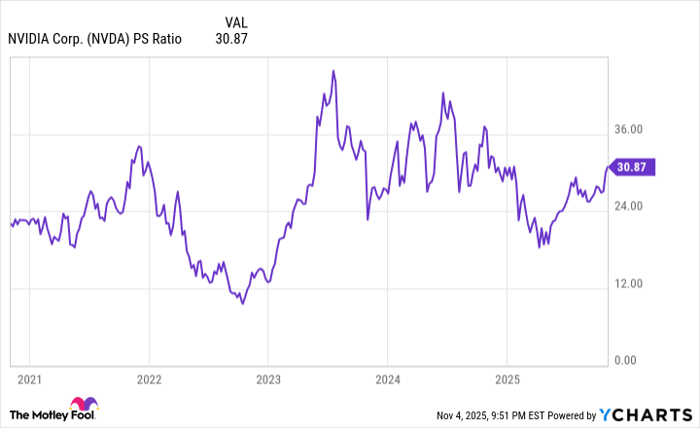

Although Nvidia has pulled back from a peak P/S ratio of a little over 42, which was reached during the summer of 2023, it did end the Nov. 3 trading session at a P/S ratio of 31. It's right back in the range that history tells us isn't sustainable and is typically a marker for bubbles.

NVDA PS Ratio data by YCharts.

Speaking of bubbles, did you know that we haven't had a game-changing investment trend in over 30 years avoid an early stage bubble-bursting event? Starting with and including the internet, we've watched bubbles form and burst with genome decoding, nanotechnology, China stocks, 3D printing, blockchain technology, cannabis, and the metaverse. Nothing suggests artificial intelligence will be the exception to this unwritten rule.

If investors have, once again, overshot with their expectations for early stage AI adoption and utility, Nvidia would be among the hardest-hit companies. It's trending toward generating 90% of its revenue from its data center segment.

Furthermore, Nvidia isn't shielded from competitive pressures. Though it's run circles around external GPU developers, many of its largest customers by net sales have been internally developing AI-GPUs for their data centers. These internally developed chips are much cheaper and more readily accessible than Nvidia's hardware. Despite not matching Nvidia's chips on a compute basis, these GPUs can reduce the AI-GPU scarcity that's fueled Nvidia's pricing power and gross margin.

Palantir exposed Nvidia's biggest weakness -- its historically unsustainable valuation premium -- and it'll be on full display come Nov. 19.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $589,424!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,217,942!*

Now, it’s worth noting Stock Advisor’s total average return is 1,054% — a market-crushing outperformance compared to 193% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 3, 2025

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. The Motley Fool has a disclosure policy.

| 1 hour | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 9 hours | |

| 12 hours | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite