|

|

|

|

|||||

|

|

|

Chevron Corporation (CVX) just delivered another quarterly beat, marking its third straight outperformance — a streak that reflects impressive operational execution amid a choppy oil market.

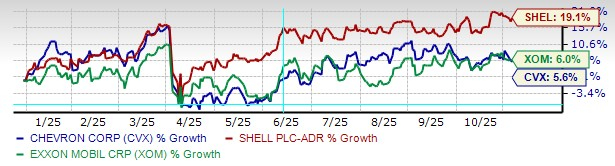

Last Friday’s Q3 report showed record production, strong downstream margins, and resilient free cash flow, all of which reinforce the company’s standing as one of the strongest names in Big Oil. Yet with shares lagging both ExxonMobil (XOM) and Shell (SHEL), and valuation sitting at a premium, the bigger question is whether this momentum can translate into meaningful upside for investors.

Chevron’s Q3 results told a story of operational strength and disciplined execution. Record output of 4,086 thousand oil-equivalent barrels per day, driven by the Hess acquisition and ramp-ups in the Permian Basin and Kazakhstan’s Tengiz field, powered results above expectations. The integration of Hess is already adding scale and higher-margin barrels, while U.S. production surged more than 27% year over year — a testament to Chevron’s upstream depth and capital efficiency.

Operating cash flow (excluding working capital) jumped nearly 20% year over year to $9.9 billion, easily funding the $3.4 billion in dividends and $2.6 billion in buybacks. These robust numbers underscore Chevron’s ability to convert production growth into shareholder returns, even as commodity prices moderate.

Although falling oil realizations hurt upstream profits, Chevron’s downstream business was exceptionally strong, delivering a 91% surge in earnings to $1.1 billion. Expanding refining margins across its core operating regions provided a critical financial cushion, effectively offsetting the impact of softer crude prices. This robust, integrated structure — where the refining arm successfully mitigates upstream volatility — mirrors the fundamental strength observed at peers like ExxonMobil and Shell, all of whom strategically leverage their diversified operations to stabilize earnings across commodity cycles.

For Chevron, that balance reinforces its position as a cash-flow powerhouse. Management’s commitment to maintaining a $20 billion annual repurchase program and a quarterly dividend of $1.71 per share signals confidence in the company’s underlying cash generation, even with capital spending inching higher due to the Hess integration.

Yet not everything in Q3 was smooth sailing. Upstream earnings plunged 28% year over year, primarily penalized by softer oil prices and the transaction costs related to the Hess acquisition. Crucially, the deal also introduced immediate integration expenses and temporary operational friction, creating an undeniable drag on near-term profitability. While management forecasts significant synergies to finally appear in 2026, the current pressure on margins has noticeably cooled enthusiasm for Chevron’s immediate earnings trajectory.

In sharp contrast, Shell's naturally leaner cost structure and rapidly expanding LNG segment have bolstered its earnings resilience. Similarly, ExxonMobil’s sustained, record-breaking output from the Permian Basin continues to successfully mitigate falling crude prices. Chevron’s modest share price appreciation year to date — especially when measured against Shell’s double-digit gains — is a direct reflection of this current transitional phase as it works to fully absorb and optimize its new operational assets.

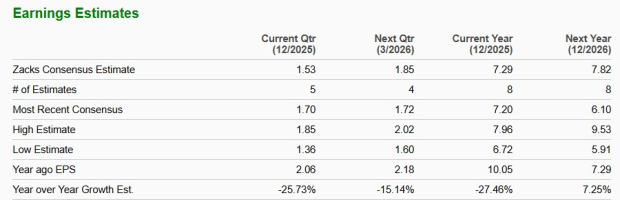

Chevron’s premium valuation also leaves less room for error. The stock trades at roughly 19.5X forward price-to-earnings multiple, notably higher than Shell’s 11X and ExxonMobil’s 15X. This high price is especially striking because the Zacks Consensus Estimate predicts Chevron's actual profits will drop significantly — by 27.5% — in 2025.

This gap highlights a key issue: even though Chevron has great assets, its positive future is already accounted for in today’s stock price. The stock's premium price tag means that unless the company reports surprisingly better results or analysts drastically increase their future forecasts, it’s unlikely to deliver the biggest returns compared to its cheaper rivals in the short term.

Chevron’s third straight quarterly earnings beat highlights its strong execution — marked by record production, tight capital discipline, and consistent shareholder returns. However, softening EPS trends, elevated valuation, and near-term uncertainty from ongoing integration expenses make the risk-reward profile less compelling at this stage.

While Chevron’s long-term fundamentals remain sound and its operational stability unmatched in the energy sector, the stock currently holds a Zacks Rank #4 (Sell), suggesting limited short-term upside. For now, investors may want to scale back exposure until clearer growth catalysts emerge.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| 6 hours |

Exxon Mobil on Pace For Largest One-Day Market Cap Loss Since 2008

XOM -5.23%

The Wall Street Journal

|

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 12 hours | |

| 12 hours | |

| 12 hours | |

| 13 hours | |

| 13 hours | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite