|

|

|

|

|||||

|

|

|

Costco Wholesale Corporation’s COST October sales update offers a fresh perspective on the retail giant’s momentum. As a dominant force in the warehouse club segment with a consistent history of growth, Costco has remained a longtime investor favorite. Yet, the latest sales figures raise an important question: Is now the right time to buy, hold or book profits on Costco stock?

Costco’s membership-driven model remains a core strength, with high renewal rates ensuring a dependable revenue stream. Its efficient supply chain and bulk purchasing power enable competitive pricing, reinforcing its strong market position. This combination of customer loyalty and operational efficiency continues to give Costco an advantage in a competitive retail landscape.

For the four weeks ended Nov. 2, 2025, Costco reported a 6.6% year-over-year increase in total company comparable sales. Regionally, comparable sales rose 6.6% in the United States, 6.3% in Canada and 7.2% in Other International markets. Digitally-enabled comparable sales surged 16.6%. (Read: Costco Sales Climb Again in October as Shoppers Keep Spending)

As a result, Costco's net sales for October increased 8.6% to $21.75 billion, up from $20.03 billion in the same period last year. This follows sales improvements of 8% and 8.7% reported in September and August, respectively, reflecting a strong and consistent sales performance over the past few months.

Costco’s main strength is its resilient membership-based business model, which acts as a powerful growth engine. This setup provides a steady and predictable revenue stream from annual fees, setting Costco apart from traditional retailers. Importantly, the model creates a strong value proposition, leading to consistently high membership renewal rates. The annual membership structure also fosters a sense of exclusivity and trust among shoppers. This approach supports Costco’s competitive advantage, enabling it to operate on slim margins while achieving high sales volumes.

The company’s operational discipline is clear in its meticulous approach to supply chain management and procurement. By leveraging scale and efficiency, Costco routinely secures favorable terms with suppliers and passes savings on to customers without sacrificing quality. This disciplined cost management improves margins and shields the company from inflationary pressures. Coupled with limited-markup policies, Costco proves that profitability and affordability can coexist in a competitive retail landscape.

Costco’s capacity to adapt to changing consumer preferences has also been key to its growth. The company modifies its product mix to include both everyday essentials and unique, high-demand items — a strategy that broadens its appeal across diverse customer groups. Using data-driven market analysis and flexible merchandising, Costco has gradually expanded its presence both domestically and internationally.

Costco’s strategic investments in technology and logistics are strengthening its multi-channel ecosystem. The company’s digital initiatives have improved member engagement and operational efficiency, combining online convenience with the effectiveness of its warehouse model. By boosting e-commerce capabilities and expanding logistics infrastructure, Costco not only taps into new growth opportunities but also ensures stable demand from a wide member base that values reliability and convenience equally.

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 7.7% and 11%, respectively.

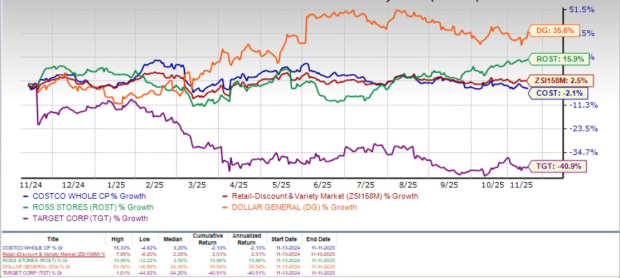

Costco has declined 2.1% over the past year against the industry's growth of 2.5%. When compared with its peers, Costco has underperformed Ross Stores, Inc. ROST and Dollar General Corporation DG but fared better than Target Corporation TGT. While shares of Dollar General and Ross Stores have rallied 35.6% and 15.9%, respectively, Target has declined 40.9%.

Despite muted stock performance over the past year, Costco is still trading at a premium to its industry peers. The company's forward 12-month price-to-earnings ratio stands at 44.96, higher than the industry’s ratio of 29.78 and the S&P 500's ratio of 23.66. However, the stock is trading below its median P/E level of 50.35, observed over the past year.

Costco is trading at a premium to Target (with a forward 12-month P/E ratio of 11.52), Dollar General (15.92) and Ross Stores (24.25).

Now, the question arises whether Costco’s current price is warranted or overvalued in today’s market.

The company’s high valuation shows that investors have strong faith in the company’s steady growth, loyal customer base and solid business model. This premium may be deserved, given Costco’s consistent performance, but it also means the stock has less room for error. At this level, some of the future growth may already be priced in, making it harder to justify further upside.

Costco's October sales results reaffirm its position as a dependable stock in the retail sector, backed by strong membership growth, consistent comparable sales improvement and solid financial fundamentals. While the stock trades at a premium valuation, this appears justified, given its operational resilience, expanding global footprint and loyal customer base. For long-term investors willing to pay up for quality and stability, Costco remains a compelling choice. However, for value-conscious buyers, the elevated valuation may warrant patience for a more attractive entry point. Costco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-18 |

Costco Gas Pumps Are So Popular the Retailer Is Building Stand-Alone Stations

COST

The Wall Street Journal

|

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite