|

|

|

|

|||||

|

|

|

As Target Corporation TGT is slated to report third-quarter fiscal 2025 earnings on Nov. 19 before market open, investors face an important decision on whether they should buy the stock now or hold their current positions.

With earnings expectations and market conditions in mind, it is crucial to evaluate key factors influencing Target’s performance and whether the stock offers an attractive entry point ahead of its earnings report.

Although TGT has built a strong position in retail through its diversified business model and omnichannel strategy, the company is facing weakening consumer demand, traffic softness and margin compression.

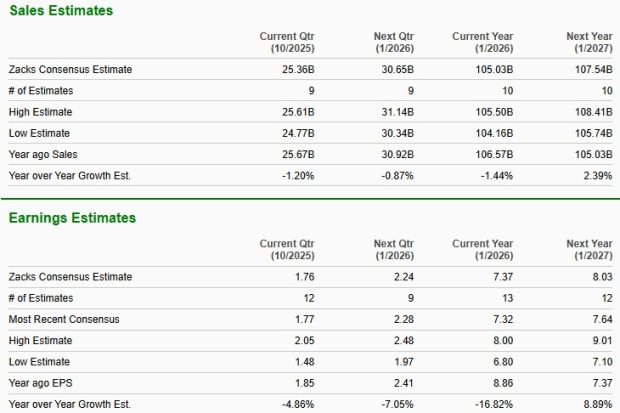

The Zacks Consensus Estimate for fiscal third-quarter revenues is pegged at $25.36 billion, indicating a 1.2% decline from the year-ago reported level. Also, the consensus mark for quarterly earnings has moved down 2 cents in the past seven days to $1.76 per share, indicating a 4.9% decline from the year-ago quarter’s reported figure.

Target has a trailing four-quarter average negative earnings surprise of 8.4%. In the last reported quarter, the company’s bottom line missed the Zacks Consensus Estimate by a margin of 1.9%.

As investors prepare for TGT’s third-quarter announcement, the question of earnings beat or miss looms. Our proven model does not conclusively predict an earnings beat for Target this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. However, that is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Target has an Earnings ESP of -3.07% and a Zacks Rank #3 at present. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Target Corporation price-consensus-eps-surprise-chart | Target Corporation Quote

Target’s integrated strategy appears to have provided support to its third-quarter performance, despite a tough retail backdrop. We believe TGT’s strong brand equity, growing owned-brand portfolio and continued investment in digital capabilities helped maintain relevance with value-conscious shoppers.

Efforts to strengthen Target Plus and expand third-party assortment are likely to have broadened the merchandise mix and improved marketplace flexibility, while the Enterprise Acceleration Office’s work to streamline processes and modernize technology helped the company operate with greater speed and agility. The deployment of enhanced AI tools is from this perspective. Cumulatively, these initiatives positioned Target to better leverage its scale, reduce friction across operations and respond more effectively to shifting customer preferences.

Digital transformation remained a key contributor to momentum, particularly as shoppers continued to favor convenience-led options. Drive Up, Order Pickup and same-day delivery reinforced Target’s omnichannel ecosystem and are likely to have supported steadier engagement amid softer store traffic.

However, Target might have continued to face soft sore traffic. Lower spending per visit, challenged transaction volumes and ongoing margin headwinds — from promotional activity to the elevated cost of digital fulfillment — are likely to have weighed on profitability. We expect the number of transactions to decline 1% and the average transaction amount to dip 0.4% for the fiscal third quarter. As a result, we anticipate comparable sales to decline 1.4%.

Lingering tariff exposure and any markdowns might have further pressured performance, creating a drag that offset some of the benefits from strategic and operational improvements. For the fiscal third quarter, we foresee an operating margin contraction of 20 basis points.

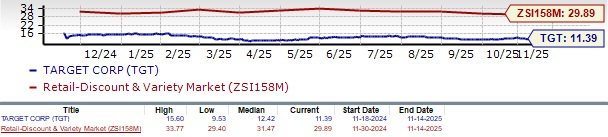

From a valuation standpoint, Target stock is currently trading at a discount compared with the Zacks Retail - Discount Stores industry. With a forward 12-month price-to-earnings (P/E) ratio of 11.39, Target stands far below the industry average of 29.89, suggesting that the stock may be relatively cheap at current levels.

When compared with other retail giants, including The Kroger Co. KR, Walmart Inc. WMT and Ross Stores, Inc. ROST, the company’s valuation looks even more discounted. Kroger trades at a forward P/E of 12.92, Walmart at 35.87 and Ross Stores at 23.89 — all higher than Target’s valuation multiple. Currently, Target has a Value Score of A.

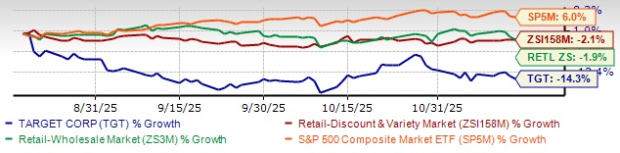

Over the past three months, Target stock has lost 14.3% compared with the industry’s decline of 2.1%. In the same period, the Retail-Wholesale sector and the S&P 500 have declined 1.9% and increased 6%, respectively.

The company underperformed some key peers, including Walmart, which has gained 1.8%. Ross Stores stock has rallied 9.9%, while Kroger stock has declined 4.3% over the same period.

Target heads into its third-quarter report with a mix of strategic momentum and uncertainty, leaving investors in a wait-and-watch position. The company’s operational upgrades, digital expansion and disciplined execution offer encouraging long-term signals, but softer store traffic, pressured comparable sales and limited earnings-beat potential temper expectations.

Given the stock’s attractive valuation but lack of a clear setup for an upside surprise, prospective investors may find it more prudent to stay on the sidelines until the results clarify the trajectory, while existing shareholders may choose to hold through the print if they have a longer-term view anchored in Target’s improving structural initiatives.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite