|

|

|

|

|||||

|

|

|

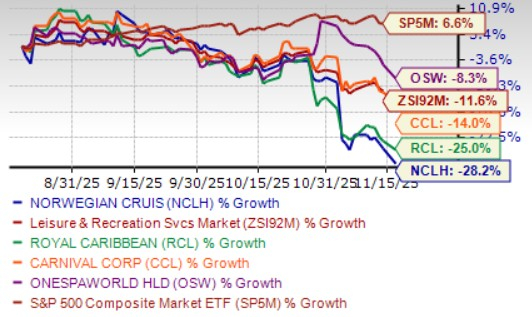

Shares of Norwegian Cruise Line Holdings Ltd. NCLH have declined 28.2% in the past three months compared with the Zacks Leisure and Recreation Services industry’s 11.6% fall. Over the same timeframe, the stock has underperformed industry peers, including Carnival Corporation & plc CCL, Royal Caribbean Cruises Ltd. RCL and OneSpaWorld Holdings Limited OSW, which have declined 14%, 25% and 8.3%, respectively. However, the S&P 500 has risen 6.6% during the same time.

This pullback reflects a combination of shifting market sentiment and company-specific dynamics. Although NCLH reported record EBITDA and strong booking momentum in the third quarter, the company’s elevated leverage profile continues to weigh on investor confidence. At the same time, its strategic pivot toward shorter Caribbean itineraries and a more family-oriented guest mix is diluting blended pricing, resulting in lowered yield guidance.

The heavier Caribbean exposure — an area prone to close-in booking swings and competitive intensity — has also amplified concerns around pricing stability. Coupled with near-term capital requirements tied to upcoming ship deliveries and an uneven macro backdrop, these factors have likely contributed to a more cautious investor stance toward the stock.

From a technical perspective, NCLH stock is currently trading below its 50-day moving average, signaling a bearish trend.

Given the significant pullback in Norwegian Cruise’s shares currently, investors might be tempted to snap up the stock. But is this the right time to buy NCLH? Let’s find out.

Despite a strong third-quarter print, Norwegian Cruise is facing several underlying pressures that may limit near-term upside. The company delivered record EBITDA, higher-than-expected load factors and disciplined cost control, yet management acknowledged that its strategic shift toward shorter Caribbean itineraries is creating measurable pricing dilution. As more families sail on the Norwegian brand, the increase in third- and fourth-quarter guests per cabin is lowering blended per diem rates, prompting the company to revise fourth-quarter yield expectations to increase approximately 2.4-2.5% compared with the prior expectation of 2.5%.

NCLH’s expanded Caribbean exposure is also contributing to investor caution. While these itineraries support stronger margins and operational efficiency versus longer international voyages, the region is inherently more susceptible to close-in booking trends and elevated competitive intensity. Management noted that promotional activity remains in line with historical norms, but the concentration of short Caribbean sailings — up more than 80% year over year in the fourth quarter — heightens sensitivity to demand fluctuations and pricing stability.

Financial leverage remains another point of scrutiny. Net leverage increased slightly to 5.4x in the third quarter due to the delivery of Oceania Allura and is expected to end the year around 5.3x. Although the company continues to prioritize deleveraging, upcoming vessel deliveries in 2026 will keep leverage higher than ideal for another year. Recent refinancing efforts, including the elimination of all secured notes, improve the capital structure but do not meaningfully change the near-term leverage profile.

Cost dynamics add to the mixed setup. Net cruise costs excluding fuel are expected to rise 50 basis points in the fourth quarter, reflecting the timing of certain expenses and an elevated marketing investment to support brand repositioning and the rollout of new amenities at Great Stirrup Cay. While these initiatives are designed to reinforce long-term pricing power and strengthen demand, they also introduce modest near-term pressure on operating margins.

Despite near-term volatility, Norwegian Cruise remains well-positioned to navigate current challenges and advance its longer-term strategic priorities. The company is sharpening its brand positioning through a focused commercial reset at the Norwegian brand, including a stronger emphasis on family travelers, upgraded leadership and a refreshed marketing campaign set to launch in early 2026.

This shift — supported by rising load factors and broader consumer engagement — is beginning to take hold as more guests respond to its short-Caribbean offerings and expanded appeal. At the same time, enhancements at Great Stirrup Cay, with new amenities coming online around the holidays and the Great Tides Water Park set to debut next summer, are expected to elevate the guest experience and serve as meaningful contributors to yield and margin performance as the destination scales throughout 2026.

Operational discipline remains a key pillar of NCLH’s strategy. Through its multiyear cost-efficiency program, the company continues to deliver sub-inflationary unit cost growth and sustained margin expansion, supported by improved itinerary mix, higher occupancy and ongoing efficiencies across the fleet. Management reiterated confidence in achieving further margin gains next year, underscoring the durability of these initiatives. Meanwhile, Oceania Cruises and Regent Seven Seas Cruises continue to benefit from consistent luxury demand and strengthened organizational alignment, providing stability and balanced growth within the broader portfolio.

Looking ahead, Norwegian Cruise’s repositioning efforts — combined with rising occupancy, a more efficient Caribbean footprint, strengthened luxury brands and upgraded private-island experiences — create a constructive backdrop for gradual recovery. While leverage and mix-related pricing dilution may keep the near-term setup uneven, the company’s strategic initiatives, operational rigor and expanding guest appeal position NCLH to manage current headwinds better and build momentum into 2026 and beyond.

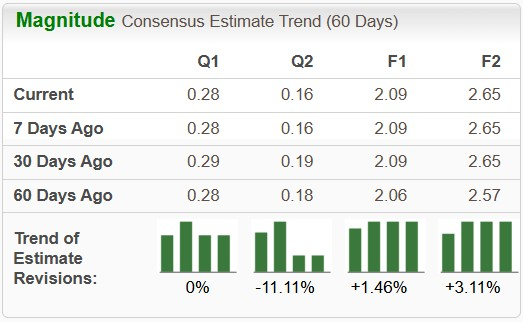

Over the past 60 days, the Zacks Consensus Estimate for NCLH’s 2026 earnings per share (EPS) has increased from $2.57 to $2.65. Over the same time frame, EPS estimates for industry players, including Carnival and OneSpaWorld, have increased 5.3% and 1.7%, respectively, while estimates for Royal Caribbean have declined 1.8%.

Norwegian Cruise stock is currently trading at a discount. NCLH is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 6.78X, below the industry average of 15.91X, reflecting an attractive investment opportunity. Other industry players, such as Carnival, Royal Caribbean and OneSpaWorld, have P/E ratios of 10.6X, 13.98X, and 17.32X, respectively.

Norwegian Cruise offers a constructive long-term setup supported by rising occupancy trends, strengthened brand positioning and meaningful enhancements across its fleet and private destinations. The company’s disciplined execution under its multiyear cost-efficiency framework, combined with a sharpened commercial strategy and the upcoming rollout of major upgrades at Great Stirrup Cay, reinforces its ability to drive margins and deepen guest engagement over time.

However, near-term risks tied to mix-driven pricing dilution, elevated leverage and greater exposure to the competitive Caribbean market continue to temper enthusiasm. Macroeconomic uncertainty, close-in booking sensitivity and execution considerations around its brand repositioning and new amenity launches may keep the stock under pressure in the intermediate term. While Norwegian Cruise’s broader trajectory remains favorable, the recent pullback reflects the persistent caution surrounding its balance sheet and evolving demand mix.

Given these dynamics, maintaining a position in this Zacks Rank #3 (Hold) stock appears sensible for existing shareholders. Prospective investors may benefit from waiting for additional clarity around pricing stabilization and deleveraging progress before initiating new positions.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Aug-10 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite