|

|

|

|

|||||

|

|

|

SoundHound AI is a leading developer of conversational artificial intelligence (AI) software.

Some of the world's top brands are using its technology, including Krispy Kreme, Chipotle, and Hyundai.

Its business is growing quickly, but its financial results are lumpy, and its stock certainly isn't cheap.

SoundHound AI (NASDAQ: SOUN) develops conversational artificial intelligence (AI) software that is used by some of the world's top brands. It's designed to understand voice prompts and respond in kind, making it highly practical in fast-paced business settings like restaurants and customer service call centers.

SoundHound is still in the early stages of commercializing its technology, so its financial results can be unpredictable, but its revenue continues to grow briskly. However, its stock is down 36% over the past month alone as investor sentiment cools on the AI industry overall, and it's now down by around 50% from last year's record high.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Should investors steer clear of this up-and-coming AI stock, or could the recent dip be the ultimate buying opportunity heading into 2026?

Image source: Getty Images.

The company's software is in high demand from businesses in a number of industries, including hospitality, automotive, healthcare, and financial services, among others.

Allina Health, a nonprofit healthcare system in the U.S., used SoundHound's Amelia platform to create an AI-powered agent named Alli. The healthcare provider says it has contributed to a 23% improvement in call center service, with 80% of calls answered in under 45 seconds. Another healthcare company, which provides vision care, uses Amelia-powered agents to handle over 25,500 phone calls every single day.

Quick-service restaurant chains like Krispy Kreme doughnuts and Chipotle Mexican Grill use SoundHound's technology to take drive-thru orders, as well as over the phone and in-store. Many restaurants also use the company's Employee Assist software, which workers can use via vocal commands any time they need help with store policies, menu items, and more.

SoundHound believes it has a $1 billion revenue opportunity in the U.S. restaurant industry alone, as more chains turn to technology to boost their efficiency.

The company generated $42 million in revenue during the third quarter (ended Sept. 30), a decline from $42.7 million in the second quarter three months earlier. It was a healthy 68% increase from the year-ago period, but a sharp deceleration from the 217% growth in the second quarter.

It's common for companies in the early stages of commercialization to deliver lumpy financial results because they don't always have the infrastructure in place to keep up with demand. Still, SoundHound increased its revenue guidance for 2025 along with its third-quarter results -- a sign that it expects momentum to continue through year-end. The company now forecasts sales somewhere between $165 million and $180 million, up from its previous prediction of $160 million to $178 million.

The strong top-line results are a product of heavy investments in acquisitions and growth-focused operating costs; however, as a result, the company is losing money at the bottom line, including $109.2 million on the basis of generally accepted accounting principles (GAAP) during the third quarter alone.

The third-quarter loss was a more palatable $13 million after excluding one-off and noncash expenses like those related to acquisitions and stock-based compensation. But with just $269 million in cash on hand, management needs to be cautious about the pace of its spending. If it can't achieve profitability soon, it will have to raise more money in the next couple of years, which could dilute existing shareholders and hurt their returns.

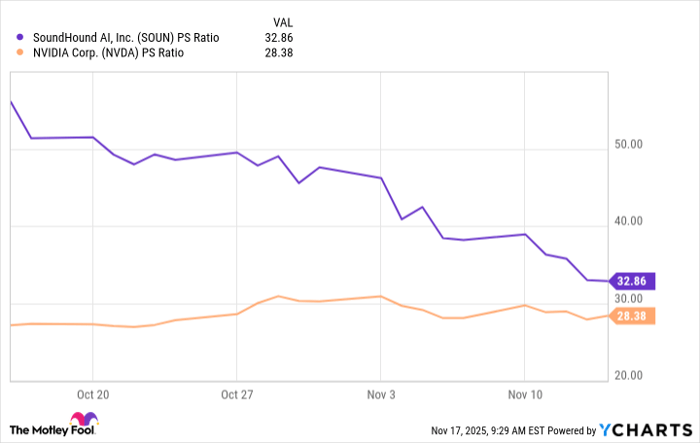

Despite SoundHound's growing business, its valuation might be a reason to avoid its stock for now. Even with its 36% slump over the past month, it still trades at a price-to-sales ratio (P/S) of 32.8, making it even more expensive than Nvidia (NASDAQ: NVDA).

SOUN PS Ratio data by YCharts.

Nvidia, the leading supplier of data center chips and networking equipment for AI, is the world's largest company. Its success spans decades, with hundreds of billions of dollars in annual revenue, soaring profits, and a rock-solid balance sheet. So I don't think a company like SoundHound deserves a premium valuation to Nvidia.

Despite its early success, the combination of its lumpy revenue growth, substantial losses, and lean balance sheet is a recipe for uncertainty, which could translate into further downside in its stock price.

As a result, although SoundHound AI might have a bright future, it's difficult to justify buying shares right now based on its valuation. If the AI boom loses any steam in 2026, investors who buy its stock today could be stuck with steep losses.

Before you buy stock in SoundHound AI, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoundHound AI wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $615,279!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,111,712!*

Now, it’s worth noting Stock Advisor’s total average return is 1,022% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 17, 2025

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill and Nvidia. The Motley Fool recommends the following options: short December 2025 $45 calls on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

| 30 min | |

| 53 min | |

| 1 hour | |

| 2 hours | |

| 4 hours | |

| 6 hours | |

| 9 hours | |

| 9 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Specialty Chip Stock Teams Up With Nvidia. Its Chart Shows Bullish Traits.

NVDA

Investor's Business Daily

|

| Apr-01 | |

| Apr-01 |

Nvidia Stock: Pay Less For Ownership, Aim For Unlimited Upside With This Strategy

NVDA

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite