|

|

|

|

|||||

|

|

|

Cruise operators are riding on a powerful wave of leisure demand, with occupancy, onboard spend and advance bookings all accelerating as consumers continue to prioritize experiential travel. Within this strengthening backdrop, Carnival Corporation & plc CCL and Norwegian Cruise Line Holdings Ltd. NCLH have emerged as standout performers, each posting record financial results, yet doing so through markedly different strategic playbooks. Carnival is leaning on scale-driven efficiencies and disciplined yield management, while Norwegian Cruise is pushing brand segmentation, premium pricing and targeted cost transformation. These contrasting approaches are creating a widening gap in operating leverage, margin visibility and financial flexibility.

For investors seeking exposure to the sector’s cyclical tailwinds and expanding cash-generation potential, the decision between these two industry leaders carries real portfolio implications. The key question becomes: Which cruise stock currently offers the more compelling risk-reward profile? A closer examination of their fundamentals, growth trajectories and capital frameworks helps illuminate where the more attractive opportunity lies.

Carnival is steadily strengthening its commercial position as demand for cruising remains firm across its major brands and regions. Management continues to emphasize disciplined pricing, improved brand segmentation and better itinerary planning — all contributing to stronger booking trends and healthier revenue mix. The company’s focus on expanding its destination portfolio, including the rollout of Celebration Key, is expected to support continued pricing gains while giving Carnival more control over onboard revenue opportunities.

Operational improvements are playing an important role in the company’s progress. Carnival has been tightening cost structures through fleet efficiencies, procurement initiatives and more effective use of shared systems across its brands. Recent investments in ship upgrades and digital tools are helping improve guest satisfaction and streamline onboard processes, contributing to more consistent execution. These steps are designed to reinforce Carnival’s operating base and support more predictable long-term performance.

The company is also making visible headway on the balance-sheet side. Management remains focused on lowering leverage through stronger cash generation and a measured approach to new capacity. By limiting near-term ship deliveries and prioritizing debt reduction, Carnival is gradually rebuilding financial flexibility. This gives the company more room to absorb external pressures and positions it better for future decisions around capital allocation.

However, Carnival still faces several challenges. The company continues to carry a substantial debt balance, and interest costs remain significantly higher than pre-pandemic levels, creating a drag on earnings. Management also noted several expected 2026 pressures, including costs tied to a new loyalty program, higher destination-related operating expenses and increased dry dock activity — all of which may weigh on its near-term margins.

Norwegian Cruise is sharpening its commercial strategy as demand remains strong across its three-brand portfolio. The company is leaning into a more focused mix shift at the Norwegian brand — expanding short Caribbean sailings, elevating family appeal and rolling out new private-island amenities — to lift occupancy and strengthen yield performance. Its luxury brands, Oceania and Regent, continue to benefit from consistent demand and targeted product enhancements, supported by refreshed marketing and upgraded fleet investments.

Operational discipline remains a core pillar. NCLH is delivering meaningful margin expansion through tighter cost control, scale efficiencies and record pre-cruise sales, while recent digital and loyalty upgrades are improving conversion and deepening guest engagement.

The company also enhanced its balance-sheet profile by refinancing upcoming maturities and reducing fully diluted share count while maintaining its commitment to sub-inflationary unit cost growth.

That said, several pressures persist. Higher family mix brings modest per-diem dilution, and 2026 is likely to carry incremental costs tied to destination development, dry docks and brand investment. Also, leverage remains elevated, keeping financial flexibility constrained in the near term.

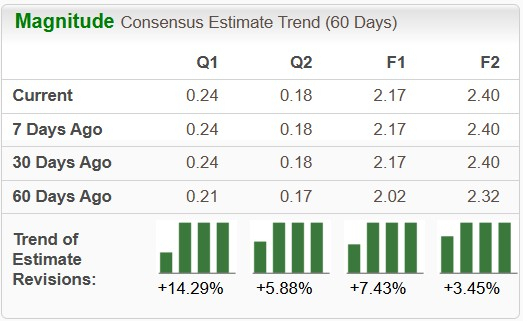

The Zacks Consensus Estimate for Carnival’s fiscal 2026 sales and EPS suggests year-over-year increases of 4.3% and 10.8%, respectively. In the past 60 days, earnings estimates for fiscal 2026 have risen 3.5%.

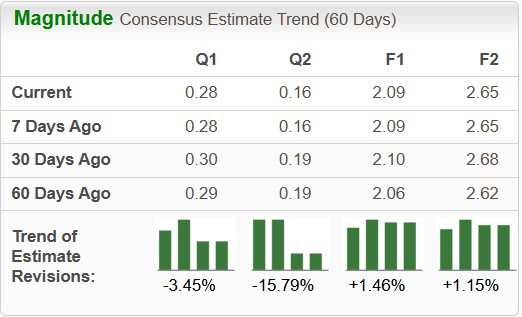

The Zacks Consensus Estimate for Norwegian Cruise’s 2026 sales and EPS suggests year-over-year increases of 10.2% and 27.2%, respectively. In the past 60 days, earnings estimates for 2025 have jumped 1.2%.

Carnival stock has gained 2.3% in the past year against the industry’s fall of 8.9%, while the S&P 500 witnessed growth of 14.8%. Meanwhile, Norwegian Cruise shares have declined 31.8% in the same time.

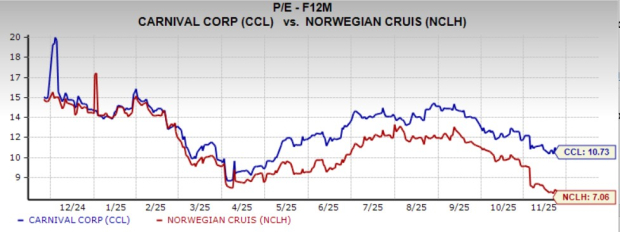

Carnival is trading at a forward 12-month price-to-earnings (P/E) ratio of 10.73, below the industry average of 15.64 over the last year. NCLH’s forward 12-month P/E multiple sits at 7.06 over the same time frame.

At this stage, Carnival appears better positioned to deliver more balanced follow-through, supported by steadier cost execution, improving fleet efficiencies and clearer traction on deleveraging. The Zacks Consensus Estimate trajectory likewise leans modestly in Carnival’s favor, reflecting firmer forward expectations relative to Norwegian Cruise, whose outlook carries more variability due to mix-driven pricing dilution, higher incremental costs and elevated leverage. The combination of improving operational visibility and a more stable financial glide path gives Carnival a relative advantage as the cruise industry works through its next phase of normalization.

Norwegian Cruise, while benefiting from strong demand and meaningful brand initiatives, faces a more complex near-term setup marked by higher family-mix pressure, sizable destination and dry-dock investments, and a slower path to balance sheet improvement. These factors contribute to softer sentiment around earnings durability and a more uneven margin trajectory. As a result, Carnival holds the edge in the current environment.

Both stocks presently carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Aug-06 | |

| Aug-06 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite