|

|

|

|

|||||

|

|

|

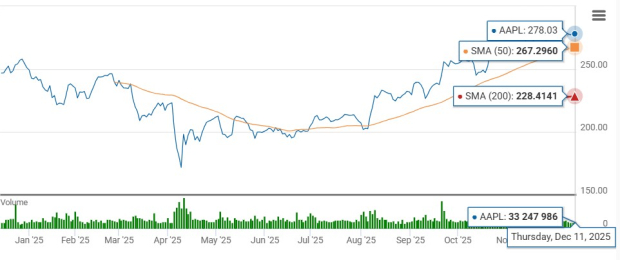

Apple AAPL shares have appreciated 41.5% over the trailing six-month period, outperforming the Zacks Computer and Technology sector’s return of 28.4%. The outperformance can be attributed to consistent results driven by strong Services business, robust adoption of iPhone 17, as well as portfolio overhaul for Mac and iPad despite headwinds related to Apple Intelligence, stiff competition in China and uncertainty over tariffs.

AAPL shares are now trading above the 50-day and 200-day moving averages, indicating a bullish trend.

So, can the rally in Apple shares continue in calendar 2026? Let’s find out.

Apple’s prospects in 2026 are expected to benefit from continued iPhone 16 series sales and strong iPhone 17 series adoption. Per Counterpoint Research’s latest data, the iPhone 16 was the best-selling smartphone globally in the third quarter of 2025. The iPhone 17 Pro Max is gaining traction, driven by strong replacement demand. Per 9TO5 Mac, Apple is rumored to launch four new iPhones, including iPhone 17e, iPhone 18 Pro and Pro Max and iPhone Fold/iPhone Ultra. Apple now expects the December quarter’s (first-quarter fiscal 2026) iPhone sales to grow in double digits year over year.

Services, which comprises Apple’s advertising business, AppleCare, Cloud Services, Digital content (Arcade, Music, Fitness+, TV, News+) and Payment services (Apple Card & Apple Pay), is riding on an expanding base of installed devices. Apple’s Services segment benefits from an expanding games portfolio and the growing popularity of Apple TV+. Apple’s strategy of adding new games on a continuous basis is driving its user base. Apple TV+ is benefiting from an expanding content portfolio.

Apple updated its Mac portfolio with the launch of the M5 chip-powered 14-inch MacBook Pro. The new MacBook Pro delivers up to 3.5 times faster AI performance than the previous generation, and is up to six times faster compared to the 13-inch MacBook Pro with M1. Apple has been winning market share thanks to strong demand for Mac.

Apple has a strong balance sheet and generates significant cash flow. As of Sept. 27, 2025, cash & marketable securities were $132.42 billion compared with term debt of $90.68 billion. Apple had cash & marketable securities worth $132.99 billion compared with term debt of $91.78 billion as of June 28, 2025. Including commercial paper of $7.98 billion, total debt was $98.66 billion as of Sept. 27, 2025.

Apple returned nearly $24 billion in the reported quarter through dividend payouts ($3.9 billion) and share repurchases ($20 billion). These shareholder-friendly initiatives make Apple attractive to investors.

The Zacks Consensus Estimate for Apple’s first-quarter fiscal 2026 earnings has increased by three cents to $2.65 per share over the past 30 days, indicating 10.42% growth from the figure reported in the year-ago quarter.

Apple Inc. price-consensus-chart | Apple Inc. Quote

The Zacks Consensus Estimate for Apple’s first-quarter fiscal 2026 revenues is pegged at $137.46 billion, indicating 10.59% growth over the figure reported in the year-ago quarter.

Apple is playing catch-up to its AI competitors, including Alphabet GOOGL, Amazon AMZN and Microsoft MSFT. While AAPL has underperformed Alphabet shares over the past six months, its shares have outperformed Amazon and Microsoft. Alphabet shares have appreciated 31.4%, while Microsoft and Amazon shares dropped 3% and 3.4%, respectively.

Limited launch and features of Apple Intelligence are negatively impacting Apple’s AI expansion opportunities. In comparison, Alphabet has been actively embedding AI, especially within Search, to enhance user experience, provide better AI-focused features and consequently improve ad performance. Microsoft is benefiting from strong Copilot adoption. The expanded OpenAI partnership, securing $250 billion in additional Azure commitments, reinforces long-term AI leadership for Microsoft. Amazon’s AI initiatives, like Trainium 2, show promise. AWS provides cutting-edge AI and machine learning services to enterprise customers, positioning Amazon as a leader in the rapidly expanding generative AI market.

Apple faces stiff competition in the smartphone market from Chinese handset makers, Samsung’s Galaxy and Alphabet’s Pixel devices. In the PC market, Apple faces tough competition from HP, Dell Technologies, Lenovo and others who are investing heavily to develop AI-powered PCs.

Apple’s stock is not so cheap, as the Value Score of F suggests a stretched valuation at this moment.

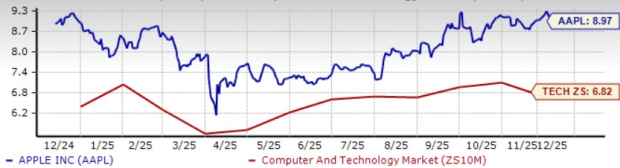

AAPL is trading at a forward 12-month price/sales (P/S) of 8.97X compared with the sector’s 6.82X, and Amazon’s 3.12X.

Apple’s iPhone sales are expected to benefit from strong adoption of the iPhone 16 and iPhone 17. However, stretched valuation and stiff competition in the smartphone, PC and AI domains are concerning for prospective investors.

AAPL currently has a Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point in the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 11 min | |

| 23 min | |

| 43 min | |

| 1 hour | |

| 5 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Could Apple's next 50 years of success lie in AI, foldable phones?

GOOGL AAPL MSFT

Yahoo Finance Video

|

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Apple turns 50: A look at the iPhone maker's history of innovation

GOOGL AAPL MSFT

Yahoo Finance Video

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite